How to Settle Pharma Stockist Claims

The end-to-end process to settle pharma stockist claims — expiry and breakage evidence, batch validation, approval and settlement by credit note.

Settling a pharma stockist claim runs through six stages: the return policy is communicated, the stockist accrues and files the claim with batch-level evidence, the field or area manager verifies it, finance validates it against the policy and batch data, an approver signs off per the delegation-of-authority matrix, and the claim is settled — usually by credit note — and reconciled. Two stages cause most of the delay: gathering complete batch and expiry evidence, and validating each line against the return policy and the GST route. The rest moves fast once those two are clean.

All ₹ figures below are illustrative, not benchmarks. Your return policy and agreement always govern. This guide owns the end-to-end process; for the wider channel picture, see the pillar on pharma channel claims and rebates in India, and for the physical-stock side, the sibling on pharma expiry, breakage and returns.

The six-stage pharma claim settlement process

Every stockist claim, whatever its type, moves through the same six stages. Getting the sequence right — and knowing which two stages absorb most of the time — is what turns an expiry backlog into a predictable pipeline. The generic version of this lifecycle is set out in the claim process explained; below is the pharma-specific shape, where batch and expiry data sit at the centre of every check.

Stage 1 — Scheme / return policy communicated

Everything downstream traces back to the return policy: the document that fixes which packs qualify for return, the expiry window (how many months before or after expiry a pack is eligible), the treatment of saleable versus non-saleable stock, any caps by value or batch, and the claim window itself. If the policy is ambiguous — an unstated expiry window, no line on who bears breakage — every claim under it inherits that ambiguity and disputes multiply at validation. A clean policy names the eligible window from the expiry date, states whether goods must be physically returned or destroyed, and fixes the evidence a claim must carry. It also has to actually reach the field and the stockist, not sit in an inbox. The way expiry and breakage returns are treated end to end is mapped in pharma expiry, breakage and returns, and the credit-note side in credit notes for expired and damaged goods returns. This stage costs little time but sets the ceiling on how cleanly the other five run.

Stage 2 — Stockist accrues and files the claim with batch-level evidence

The stockist computes the claim against the policy and files it with supporting evidence — the batch number and expiry date for each pack, the original supply reference, destruction or physical-return proof for non-saleable stock, and the return-policy reference it is claimed under. This is the first of the two slow stages: batch and expiry evidence is where claims sit for days, because the stockist is assembling records against physical stock after the fact. Filing inside the claim window matters as much as the amount — a correct expiry claim filed late is still rejected. The physical-stock distinctions that shape what evidence is needed are in pharma expiry, breakage and returns, and the stockist's place in the tier in distributor vs dealer vs super-stockist. A claim filed complete on the first pass is the single biggest lever on total settlement time. In ClaimDS, stockists and internal teams file claims against the specific return policy and attach batch, expiry and destruction proof in one place. <!-- TODO: confirm capability wording with founder --> The step-by-step is documented in submit a sales claim.

Stage 3 — Field / area-manager verification

Before finance sees the claim, the field — the area manager or medical representative closest to the market — verifies the claims that need eyes on the ground: that the expired stock physically exists, the breakage was genuine, the batch tallies with what that stockist was actually supplied. This is the human check that batch data alone cannot give, and it is where scheme leakage is caught early rather than clawed back later. The trade-off is speed: routing every claim through field verification slows the pipeline, so most companies verify by exception — value threshold, non-saleable stock, or a risk flag — rather than universally. Expiry, breakage and destruction claims almost always need it, because they hinge on physical stock that will be written off; the credit-note treatment of those is in credit notes for expired and damaged goods returns and the reversal mechanics in returns, reversals and cancellations in channel claims. Clear ownership at this stage keeps it from becoming a bottleneck.

Stage 4 — Finance validation against policy, batch data, expiry window and caps

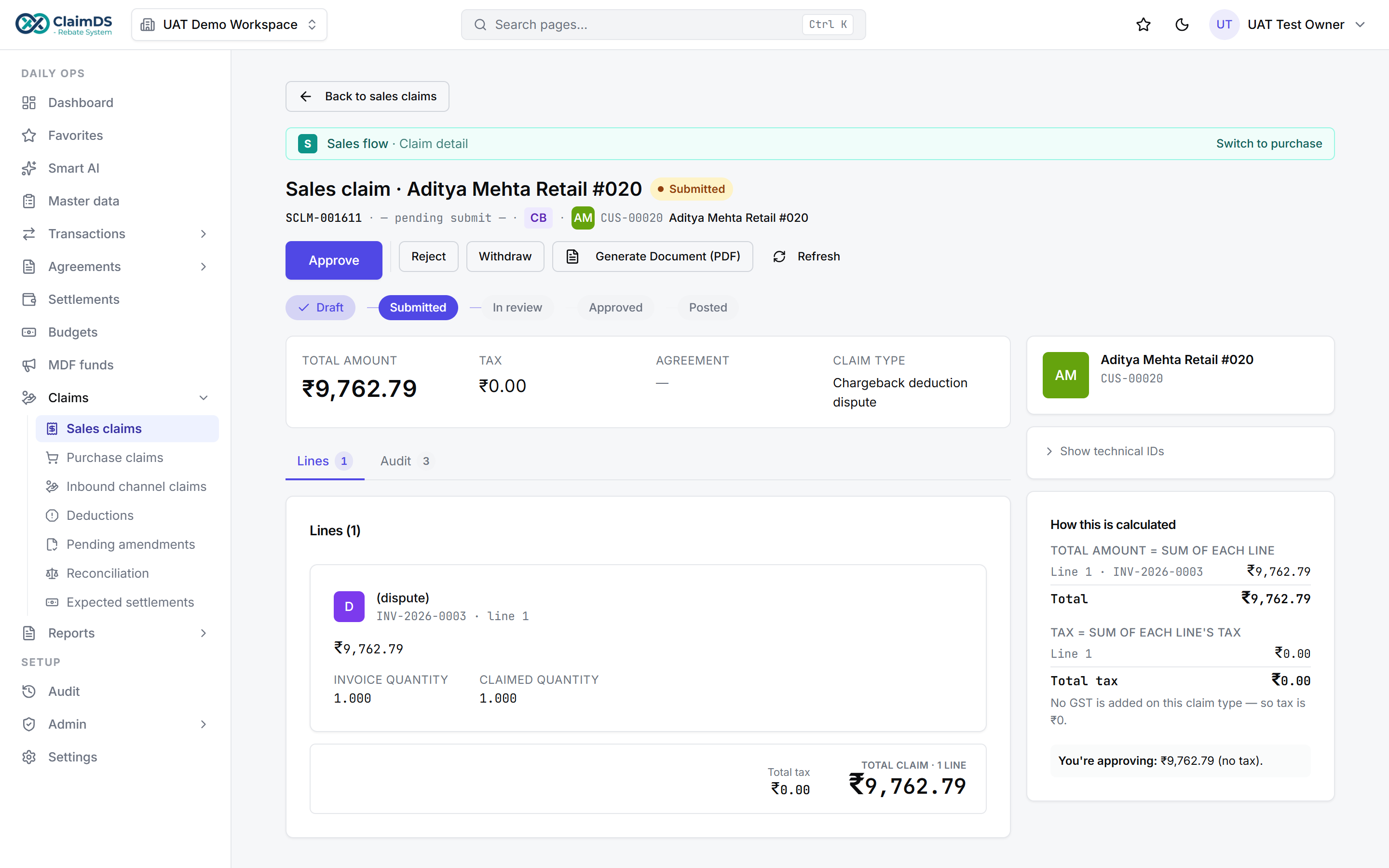

This is the second slow stage, and the one that most determines whether settlement is defensible. Finance recomputes the claim from the batch data rather than trusting the filed figure: does each batch match a genuine supply, does the expiry date place the pack inside the return window, is the amount within any per-batch or value cap, is it a duplicate of a claim already settled? It is exacting precisely because a wrong approval here becomes a real over-payment on stock that will be destroyed. ClaimDS validates each claim against its own return policy and batch data, and flags batch mismatches, out-of-window expiry, breached caps and likely duplicates for a reviewer rather than passing them silently. <!-- TODO: confirm capability wording with founder -->

Validation: a claim checked against its return policy and batch data.

Validation: a claim checked against its return policy and batch data.

The over-claims caught here otherwise become deductions and disputes downstream — the mechanism behind revenue leakage in rebate programs and the discipline in deduction management best practices. The pharma-specific version of this leakage is set out in chargebacks in pharma distribution.

Ready to see validation run on your own return policy and batch data? Book a demo and we will walk a live expiry claim through the six stages on your data.

Stage 5 — Approval per the delegation-of-authority matrix

A validated claim still needs sign-off, and the delegation-of-authority matrix decides who signs. Approval routes by value: an area or finance manager clears smaller expiry claims, while larger ones escalate to a controller or CFO. The matrix exists to keep small claims fast without letting a large one settle on one person's say-so — and to leave an audit trail of who approved what. Well-designed approval routing is the difference between a queue that clears daily and one that waits on a single overloaded approver; the patterns are in claim and rebate approval workflows and the finance-owner view in claims and deductions management for the CFO. ClaimDS routes each claim to the right approver by value and records every approval and rejection with a reason. <!-- TODO: confirm capability wording with founder --> The workflow is documented in the claim approval workflow.

Stage 6 — Settlement by credit note or replacement, and reconciliation

Once approved, the claim is settled — in the Indian pharma channel, usually by credit note against the stockist's account rather than cash, because it offsets what the stockist owes and keeps the GST trail clean. Some breakage and near-expiry cases settle by physical replacement instead, where the policy specifies it. A credit note must carry the right GST treatment; whether it is a financial or tax credit note changes the reporting, as set out in financial vs tax credit notes under GST, the pharma-specific version in GST treatment of pharma claims and returns, and the rule basis in GST credit notes for rebates under Rule 53(1A). Because expired stock is written off, the input-tax side matters too — see ITC reversal on post-sale discounts and credit notes. Settlement is not the end: the credit note has to be reconciled against the accrual and, on the GST side, against the returns — the discipline in reconciling scheme credit notes to GSTR-2B/3B, within the GST credit note time limits. ClaimDS settles approved claims by credit note and reconciles each one against its accrual and the stockist account. <!-- TODO: confirm capability wording with founder --> The how-to is in reconcile a claim to a credit note, and cancellations in rebate clawbacks and scheme cancellations.

The evidence standard

Most pharma disputes are not disagreements about the policy — they are disagreements about evidence. A claim that arrives with everything below can be validated on the first pass; a claim missing any row goes into the slow lane. The full documentation discipline is in the scheme settlement GST documentation playbook; this is the working checklist.

| Evidence element | What a valid claim carries | Why it matters |

|---|---|---|

| Batch number | The batch/lot number for every claimed pack | Ties the claim to a genuine manufactured lot; the anchor for every other check |

| Expiry date | The printed expiry date per batch | The return window runs from expiry; without it, eligibility cannot be judged |

| Physical / destruction proof | Return note or destruction certificate for non-saleable stock | The only evidence that written-off stock existed and was not resold |

| Return-policy reference | The specific policy and window the claim is filed under | Fixes the eligible window, saleable/non-saleable treatment and caps |

| Original supply reference | The invoice or supply record the batch traces back to | Confirms the stockist was actually supplied that batch |

| Claim-window compliance | Proof the claim was filed inside the policy's window | A correct claim filed after the window is still ineligible |

The batch and expiry data carry the most weight. Because validation recomputes eligibility from the batch — running the return window from the expiry date and applying caps per batch — rather than trusting the filed figure, an unstated or unmatched batch is the single deepest cause of pharma disputes. The physical-stock context behind each of these elements is in pharma expiry, breakage and returns.

Why claims get rejected

Rejections cluster around eight recurring causes. Each is concrete, and each has a fix — which is why a rejected claim is usually recoverable rather than lost. This is also the highest-leverage list to fix upstream, because every avoided rejection is a claim that settles on the first pass.

| # | Rejection reason | The fix |

|---|---|---|

| 1 | Batch does not match what was supplied | Reconcile the claimed batch to the original supply reference before re-filing |

| 2 | Pack outside the expiry return window | Check the expiry date against the policy window; re-file only eligible batches |

| 3 | Non-saleable stock claimed as saleable | Claim non-saleable stock under the correct policy line with destruction proof |

| 4 | Destruction / return proof missing | Attach the destruction certificate or return note before, not after, filing |

| 5 | Duplicate of a claim already settled | Check the claim register before filing; settle once per batch line |

| 6 | Amount exceeds the policy cap | Recompute at the policy rate and per-batch cap; re-file the eligible amount |

| 7 | Filed after the claim window closed | File inside the window; where a genuine delay exists, seek an agreed extension |

| 8 | GST treatment on the credit note is wrong | Apply the correct financial vs tax credit-note treatment and reverse ITC where due |

Reasons 1 and 2 — batch mismatches and out-of-window expiry — are the most frequent, and both trace back to how the batch data was assembled at filing. The returns and reversal question specifically is handled in returns, reversals and cancellations in channel claims, the GST treatment in reason 8 in GST adjustments in channel settlements, and the ITC reversal it triggers in ITC reversal on post-sale discounts and credit notes. Fixing rejections at the source is what turns a re-work queue into a clean pipeline — the argument in challenges of manual rebate processing.

Spreadsheets vs a claims system

Most pharma teams start in spreadsheets, and for a handful of expiry claims a month that is genuinely fine. The problem is not the spreadsheet — it is what happens to it at scale, across many stockists, thousands of batches and rolling expiry windows. The honest comparison is operational, not a promised return: below is what actually breaks.

| Operational reality | In spreadsheets | In a claims system |

|---|---|---|

| Batch tracking | Batch and expiry keyed by hand, error-prone across thousands of lots | Each claim line held against its batch and expiry |

| Version control | Copies diverge across people and months; no single truth | One record per claim, one current state |

| Duplicate detection | Eye-balled; the same batch settles twice unnoticed | Flagged against the claim register at validation |

| Audit trail | Manual, reconstructable at best | Every action and approval recorded against the claim |

| Ageing visibility | Rebuilt by hand each time someone asks | Ageing and status visible across the channel at once |

| Reconciliation | Hand-matched credit note to accrual | Each settlement reconciled to its accrual |

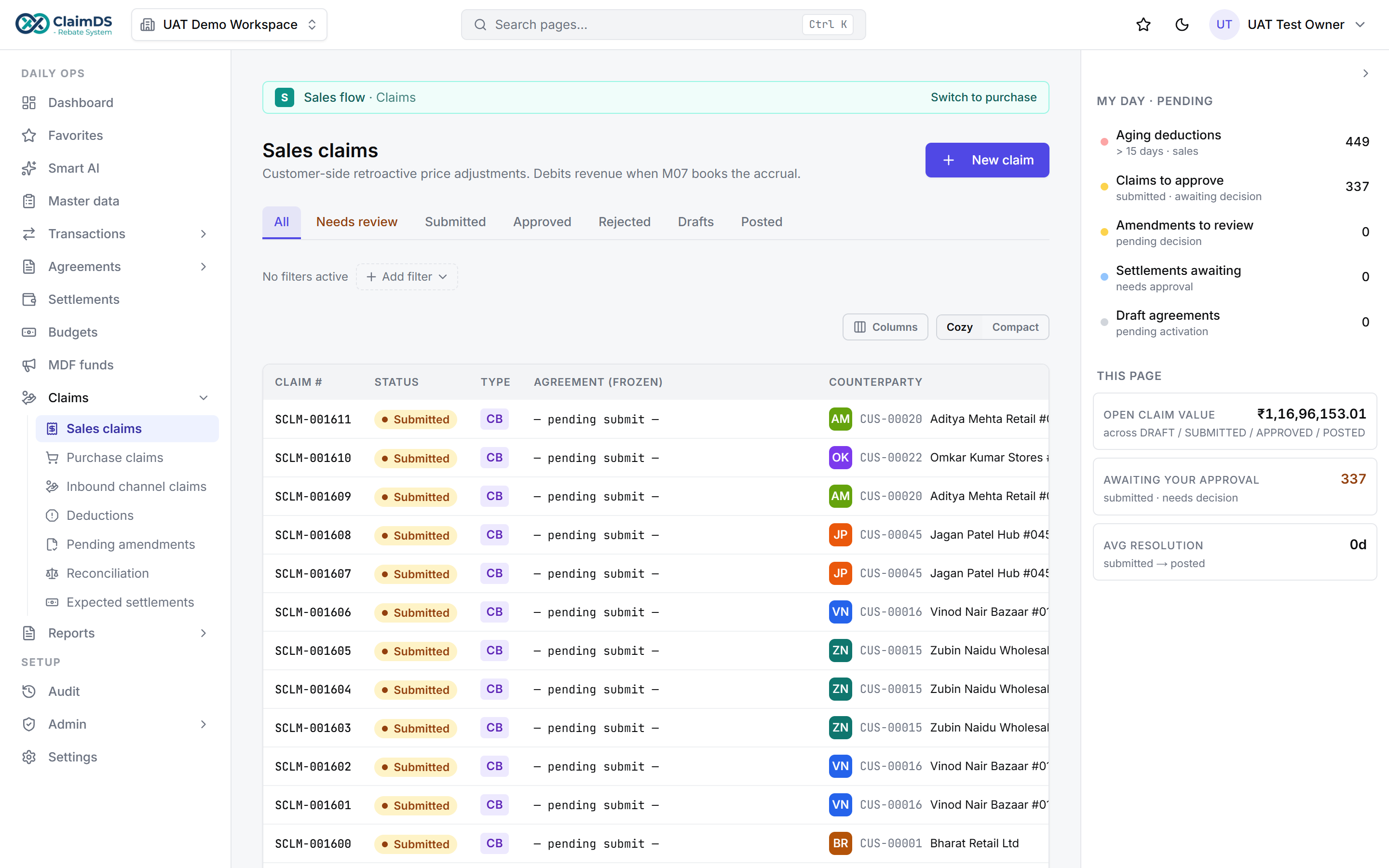

Note what is not claimed here: no percentage saved, no ROI figure. The case for a system is that the failure modes above are structural to spreadsheets — batch tracking by hand, version drift, no real audit trail, no duplicate detection, no live ageing, hand reconciliation — and they get worse, not better, as batch and claim volume grow. ClaimDS holds one record per claim with its full history, shows claim ageing and status across the channel in one view, and reconciles each settlement to its accrual. <!-- TODO: confirm capability wording with founder -->

Claim ageing and status across the channel, in one view.

Claim ageing and status across the channel, in one view.

Whether that trade-off is worth it depends on your claim volume and how much the current expiry backlog costs you — the buyer's-eye view is in distributor claims software: a buyer's guide, the settlement-specific angle in distributor claim settlement software, and the ERP connection in ERP integration for claims, rebate and TPM software. For the accounting behind the accruals a system reconciles against, see rebate accrual management, and the operational discipline in distributor claims management. Where a stockist exits the market, the buyback route is in pharma buyback, the map of who files what across tiers in India's multi-tier channel claim map, and the base-data distinction in primary, secondary and tertiary sales. The wider channel picture stays with the pillar on pharma channel claims and rebates in India.

Settling pharma stockist claims well is not clever math — it is a clean return policy, complete batch and expiry evidence, honest validation against the policy, clear approval authority, and a credit note that reconciles and reverses ITC where due. Get the two slow stages right and the rest follows. To see the six-stage process running on your own return policy and batch data, book a demo.

Frequently asked questions

How long does a pharma claim take to settle?

There is no fixed number — it depends on how complete the batch and expiry evidence is and how cleanly validation runs. A claim filed with batch numbers, expiry dates, destruction proof and a return-policy reference can move through verification, approval and credit note quickly. Missing evidence or a batch that does not match is what stretches settlement from days into weeks.

What documents are needed for a stockist expiry claim?

A valid expiry claim carries the batch number and expiry date for each pack, the return-policy reference it is claimed under, physical or destruction proof for goods that cannot be resold, the original purchase reference, and proof it was filed inside the claim window. Missing any of these is the most common reason an expiry claim stalls at validation.

Why was my claim rejected?

The usual reasons are concrete: the batch does not match what was supplied, the pack fell outside the return window, non-saleable stock was claimed as saleable, destruction proof was missing, the claim duplicated one already settled, or the amount exceeded the policy cap. Each has a fix — correct the batch, attach the proof, or re-file the eligible portion within the window.

Is a claim settled by credit note or replacement?

In the Indian pharma channel most stockist claims settle by credit note against the stockist's account, because it offsets what the stockist owes and keeps the GST trail clean. Some breakage and near-expiry cases settle by physical replacement instead. The return policy and the agreement decide which route applies, and the credit note carries the GST treatment.

What is batch-level evidence in a pharma claim?

Batch-level evidence is the record that ties each claimed pack to a specific manufactured lot: the batch number, its expiry date, and the original supply reference. Validation recomputes eligibility from this batch data — the return window runs from the expiry date, and caps apply per batch — so a claim without batch detail can be trusted but not validated.

Who approves a pharma stockist claim?

Approval follows a delegation-of-authority matrix: finance validates every claim, then sign-off routes by value — an area or finance manager clears smaller claims, while larger ones escalate to a controller or CFO. The matrix keeps small expiry claims moving while putting senior eyes on the ones that carry real money, with each approval recorded for audit.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.