Rebate Clawbacks and Scheme Cancellations in India

When a rebate must be recovered or a scheme withdrawn — clawback clauses, recovery routes, accrual reversals and the tax questions they raise.

Money already paid to the channel sometimes has to come back. A target is missed after an advance payout; goods are returned after a rebate is settled; a duplicate is caught after the cheque clears; a scheme is withdrawn mid-period. Each of these is a clawback — and each is a commercial problem, an accounting problem and a tax problem at the same time. The order in which you handle those three decides whether the recovery actually works or just creates a fresh dispute.

Why do clawbacks happen?

Clawbacks are not random. They cluster around six causes, and almost every one was avoidable at the design stage — which is the first reason they are worth understanding before they happen rather than after.

A target missed after a provisional or advance payout. You paid a distributor against a projection, and the projection did not land. This is the single most common clawback, and the most self-inflicted: it exists only because someone chose to pay on expectation rather than achievement. It is the recovery you should never have to make.

Returns or cancellations after settlement. A volume rebate was settled on a quantity that later shrank because the customer returned goods or cancelled an order. The rebate was correct on the day it was paid and wrong a month later. This is inherent to the timing of returns, but tighter claim windows shrink the exposure.

A duplicate or erroneous claim paid. The same claim came in twice, or an arithmetic error slipped through, and the payment went out before anyone caught it. Fully avoidable with validation before settlement — this is revenue leakage that a control would have stopped.

Scheme terms misapplied. The circular said one thing and the claim was settled on another reading — wrong slab, wrong period, wrong SKU. Avoidable, but only if the scheme terms are precise enough to apply the same way twice.

An agreement breach. Channel-hopping, unauthorised discounting, cross-territory selling — the partner earned the incentive and then broke the terms it was conditional on. Recovery here is less an accounting correction than a contractual remedy.

An audit finding. A later review — internal or statutory — concludes that an amount should not have been paid. This one is rarely avoidable in advance; it is the reason the audit trail behind every settlement has to survive scrutiny long after the money moves. For a CFO, the claims and deductions picture is exactly where these findings surface.

The pattern across all six is the same. A clawback is almost never a surprise about what a rebate is — it is a gap between when money moved and when the fact that justified it was confirmed. Close that gap at design time and most of this list never triggers.

The clawback clause: what the agreement should say

Recovery is far easier when the agreement anticipated it. A supplier rebate agreement that stays silent on clawbacks forces you to argue the right to recover after the fact; one that spells it out turns recovery into a mechanical step. These are commercial points to raise with your legal advisor — not a template to copy, and not legal advice — but a well-drafted clause tends to cover nine things:

- Trigger events — precisely which situations create a right to recover (missed target, return, duplicate, breach, audit finding).

- Notice period — how much warning the partner gets before a recovery is actioned.

- Recovery method — whether recovery is by netting against future claims, a debit note, or recovery of the payout itself, and who chooses.

- Time limit — how long after the original payment a clawback can still be raised.

- Evidence standard — what the brand must show to justify the recovery, so it is not a bare assertion.

- Dispute route — how a contested clawback is escalated and resolved.

- Effect of partial achievement — whether a partner who fell just short of target keeps a proportionate benefit or loses the lot.

- Interaction with future claims — whether a recovery blocks, reduces or runs alongside the partner's next claims.

- Effect on termination — what happens to outstanding recoveries if the relationship ends mid-scheme.

The link between a clean clause and a clean number runs straight through to how the accruals were calculated in the first place — a clause you cannot compute against is a clause you cannot enforce.

Four recovery routes

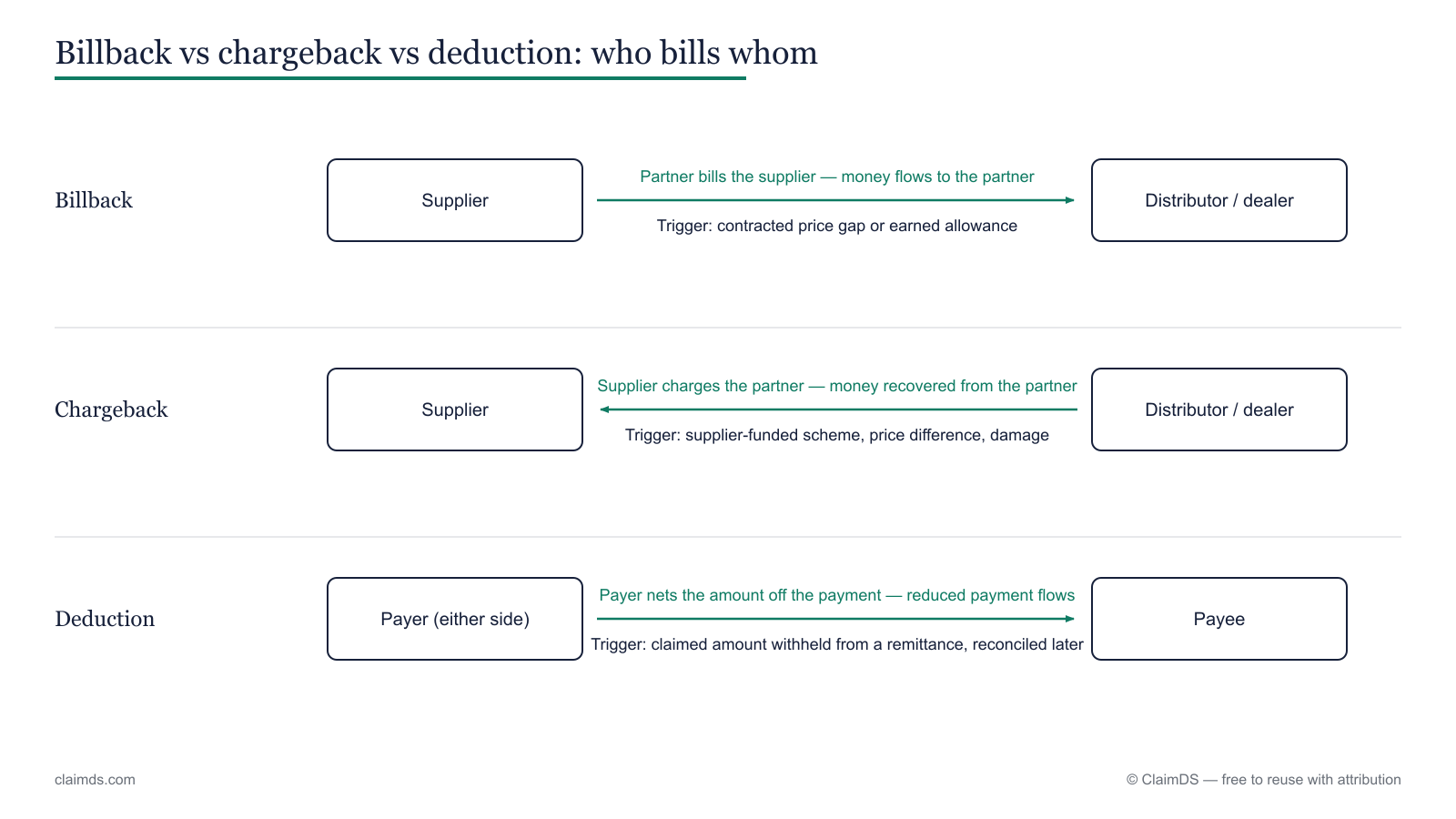

Once the right to recover exists, there are four ways to actually get the money back. They differ in speed, formality and relationship cost, and each lands differently in the two sets of books.

Netting against future claims or payments

The fastest route: reduce the partner's next claim or payment by the amount owed. It works only where the partner agrees, or the agreement clearly permits it — netting an amount the partner disputes simply converts one argument into two.

| In the brand books | In the distributor / dealer books |

|---|---|

| Next payable reduced by the recovery amount; original over-payment cleared against it | Next receivable reduced by the same amount; nets down the balance due |

Debit note on the distributor

The formal route: the brand raises a debit note on the distributor for the amount to be recovered. It creates a clean, dated document trail, which is why it is the default when the amount is material or contested. The tax treatment of that debit note is not a bookkeeping afterthought — route it through GST adjustments on channel settlements before you raise it.

| In the brand books | In the distributor / dealer books |

|---|---|

| Debit note raised on the distributor; recovery recognised as due | Debit note received and recorded as a payable to the brand |

Reversal of the original credit note

Where the rebate was originally settled by credit note, the cleanest correction is to unwind that credit note rather than raise a fresh document alongside it. This only applies when a credit note was the settlement instrument, and the mechanics — which document changes, and how the tax follows — must be documented carefully; the same GST adjustments on channel settlements walkthrough covers it.

| In the brand books | In the distributor / dealer books |

|---|---|

| Original credit note reversed or corrected; liability and any tax adjustment unwound | Credit note reversal recorded; the earlier reduction to the payable is undone |

Direct recovery / payout return

The rarest route: asking the partner to actually return money already banked. It carries the highest relationship cost and is usually a last resort, reserved for breach or fraud where netting and debit notes are not available or not appropriate.

| In the brand books | In the distributor / dealer books |

|---|---|

| Cash refund expected from the partner; recovery booked as receivable until settled | Cash repayment made to the brand; payable cleared on remittance |

A clawback recovers money down the same channels a claim paid it out — by netting, a debit note, or reversing the credit note.

Scheme cancellation and mid-period changes

Recovering a single over-payment is one thing. Pulling a whole scheme is another, and it is where commercial, legal and accounting pressures collide hardest.

Cancelling before the scheme ends. You can stop offering a scheme at any point — but stopping it prospectively and clawing back what has already accrued are different acts. Cancel cleanly and you halt future accrual with notice; try to reach backwards and you are into contested territory.

Withdrawing after claims are filed. This is the hard case. Partners have submitted claims, earned under the terms you published, and now you want to withdraw. Claims validly earned before the withdrawal are, commercially, a commitment rather than a courtesy. Refuse them and you save cash once; you pay for it at every negotiation that follows, because the channel now prices in the risk that your schemes are not dependable. Related mechanics — how filed claims unwind when the underlying sale reverses — sit alongside this in returns, reversals and cancellations on channel claims.

Retrospective term changes. Changing the rate, slab or eligibility after the period has run is the most fraught of all. Whether a scheme can be withdrawn or amended retrospectively depends on the scheme circular's own terms and your dealer agreement — take legal advice before you act; this is a pointer, not a position.

The commercial reality is blunt: notice matters, honouring earned claims matters, and the trust cost of getting it wrong outlasts the saving. A scheme pulled without warning does not just cost the disputed claims — it teaches every partner to discount your next offer, which raises the price of every scheme that follows. The design lesson is just as blunt. Schemes that state their own amendment and withdrawal terms up front — how much notice, what happens to in-flight claims, whether changes can reach backwards, and who bears the cost of stock already bought against the scheme — avoid nearly all of this. The wider menu of scheme structures, each with its own cancellation profile, is set out in types of trade schemes in India, and the settlement discipline that makes withdrawal cleaner is covered in secondary scheme settlement.

Accrual reversals and write-backs

Behind every scheme sits an accrual — the liability you booked for rebates expected to be claimed. When a scheme is cancelled, or when claims simply never arrive, that accrual has to be dealt with, and how you deal with it shows up directly in the P&L.

If a scheme is cancelled before any payout, the accrual is reversed and the liability comes off the books. If claims lapse — the window closes with money unclaimed — you face the unclaimed-liability question: how long do you carry a liability for a claim that may never come, and when do you write it back? That decision turns on your claim-window policy, your write-back policy, and the P&L optics of a large write-back landing in one period. A big write-back flatters the numbers in the period it hits, which is exactly why the policy should be fixed in advance rather than decided when the amount is staring at you. Year-end timing sharpens all of this: a write-back taken in March reads very differently from the same amount taken in April, and a reviewer will ask why the timing fell where it did.

There is a discipline point underneath the optics. If you release liabilities early to hit a number, you will eventually meet the partner whose late-but-valid claim you have already written back — and now you are paying it out of the current period against no accrual. Carrying the liability to the honest end of the window, then writing back what genuinely lapsed, is both cleaner accounting and cheaper in disputes.

Consider an illustrative example. A scheme carries a ₹40,00,000 accrual. By the time the claim window closes, ₹31,00,000 has been validly claimed and settled, leaving ₹9,00,000 unclaimed. Under a documented write-back policy, that ₹9,00,000 no longer represents a real obligation once the window has shut, so it is written back to the P&L — a one-time credit to the current period. The decision is not whether the ₹9,00,000 is "owed" (it is not, once the window closes) but when and how visibly it lands, and whether the window truly closed for every partner or only most. (Figures illustrative.)

The mechanics of unwinding an accrual or a settlement — the actual sequence of steps — are covered in the product docs: reverse an accrual or settlement and the broader reversals explained, with the timing discipline in month-end close. The depth on carrying and releasing these liabilities lives in rebate accrual management. The specific journal entries for a reversal or write-back are their own topic — the debits and credits that record it — and deserve a dedicated treatment. <!-- TODO: link journal-entries article when it exists -->

<!-- TODO CA REVIEW: prior-period adjustment vs current-period correction (Ind AS 8) treatment — reviewer to confirm position -->Where a write-back or reversal relates to an earlier period rather than the current one, whether it is treated as a prior-period adjustment or a current-period correction is a matter for your accounting policy and standards such as Ind AS 8. This article names the standard only and takes no position on which treatment applies — that is a call for your finance team and reviewer.

Revenue-recognition standards such as Ind AS 115 also bear on how the original incentive and its later reversal interact with reported revenue; that interaction is a topic in its own right and is named here only, not developed. <!-- TODO: link Ind AS 115 revenue-recognition article when it exists -->

The tax questions clawbacks raise

Recovery is where the tax exposure concentrates, and it is where a confident-sounding answer is most dangerous. The conservative posture below names the instruments and stops there.

GST. If the rebate was originally settled by a credit note that reduced taxable value, then recovering that amount means the underlying document has to be corrected — you cannot claw back the money and leave the tax document describing the old, larger benefit. The credit and debit notes that carry this correction are the Section 34 documents, and doing it properly has an input-tax-credit consequence for the recipient at the other end of the channel. The full mechanics — which document, in which direction, and the ITC follow-through — belong in GST adjustments on channel settlements; do not improvise them from this page.

TDS and Section 194R. Where a benefit or incentive was subjected to tax deduction under Section 194R and is later clawed back, the treatment of the tax already deducted is not settled. The position here depends on facts and timing, and practice varies — take this to your tax advisor before you structure the recovery. This article asserts nothing about whether the deducted tax can be adjusted, credited or recovered.

<!-- TODO CA REVIEW MANDATORY: TDS treatment on clawed-back 194R benefits — reviewer to confirm current position and add citations; publish this section only after review -->For where these tax questions fit within the wider landscape of channel incentives and their treatment, the overview in tax on rebates, chargebacks, billbacks and buybacks in India and the Section 194R explainer give the surrounding context — but neither replaces advice on your specific recovery.

Designing schemes that don't need clawbacks

The best clawback is the one you never have to make. Five design choices remove most of the exposure before a scheme even launches:

- Pay on achievement, not projection. Settle when the target is actually hit, not when you hope it will be. This alone eliminates the most common clawback.

- Use provisional accruals, not advance payouts. Carry the expected cost as a liability and release it on achievement, rather than paying cash up front and hoping to recover it.

- Set claim windows. A defined window closes the door on late claims and gives write-backs a clean trigger.

- Validate before settling. Catch duplicates, arithmetic errors and misapplied terms while the money is still in your hands — the point of a real claim and rebate approval workflow.

- Keep the audit trail. Every settlement should carry its own evidence, so that if a recovery is ever needed the basis is already documented rather than reconstructed.

Run this way — provisional rebate accruals released on achievement, inside defined windows, behind real validation — and clawbacks shrink from a routine headache to a rare exception.

This article is general information, not tax, legal or accounting advice. GST, TDS and accounting treatment depend on the specific facts, the instruments used and the timing, and the position can change. The TDS-on-clawback question in particular is unsettled — confirm every tax and accounting position with a qualified CA or CMA before acting on it.

<!-- TODO: CA/CMA reviewer name and credential before publish — MANDATORY; the TDS-clawback section must not publish unreviewed -->Handled well, a clawback is a controlled unwind — a documented recovery down the same channel the money went out on, not a fight. ClaimDS is built to make that control the default: provisional accruals, defined claim windows, validation before settlement, and an audit trail that survives the recovery. <!-- TODO: confirm capability wording with founder -->

Frequently asked questions

What is a rebate clawback?

A rebate clawback is the recovery of an incentive already paid to a channel partner, when the basis for that payment no longer holds — a target missed after an advance payout, goods returned after settlement, a duplicate claim, or a scheme withdrawn mid-period. It is a commercial, accounting and tax event at once, best handled in that order.

Can a company recover a rebate already paid?

Usually yes, if the agreement provides for it. The cleanest recovery routes are netting against future claims, raising a debit note, or reversing the original credit note. Recovery without a clause is harder and can sour the relationship. What the recovery applies to, and how, should be set out before the scheme runs, not argued afterwards.

What happens if a distributor does not achieve the target after an advance payout?

If you paid on projection and the distributor falls short, the difference becomes recoverable. This is the most common clawback and the most avoidable — paying against a provisional accrual instead of an advance payout removes it entirely. Where an advance was paid, recovery is usually by netting against the next claim or a debit note for the shortfall.

Can a scheme be cancelled mid-period?

Commercially you can stop a scheme at any time, but stopping it and escaping the claims already earned are different things. Whether a scheme can be withdrawn retrospectively depends on the scheme circular's own terms and your dealer agreement — take legal advice. Claims a partner has already earned under the stated terms are usually honoured; future accrual can be halted with notice.

What happens to claims already filed when a scheme is withdrawn?

Claims filed and validly earned before withdrawal are generally a commitment, not a courtesy — refusing them costs trust you will pay for at the next negotiation. Claims not yet earned, or filed outside the window, can usually be declined. The dividing line should be the scheme's own terms, which is why those terms must be written down first.

How is a rebate reversal recorded?

A reversal unwinds the original entry. If the rebate was accrued but not yet paid, you reverse the accrual and the liability drops. If it was settled by credit note, the document itself must be corrected, not just the ledger. The accounting and the tax document have to move together — correcting one and not the other creates a mismatch.

What is a write-back of an unclaimed scheme?

A write-back reverses an accrual that will never be claimed. When a scheme's claim window closes with money still unclaimed, the leftover liability no longer represents a real obligation, so it is written back to the P&L. A large write-back flatters the current period's numbers, which is exactly why the policy for it should be set in advance, not case by case.

What is the GST effect of a clawback?

It depends on how the rebate was originally settled. If it went out on a tax credit note that reduced taxable value, recovering it means that document has to be corrected, which has an input-tax-credit consequence for the recipient. If it was a financial credit note with no tax adjustment, the GST position is different. Confirm the treatment with a tax advisor.

What happens to TDS already deducted on a clawed-back incentive?

There is no simple answer. Where a benefit was subjected to tax deduction under Section 194R and is later recovered, the treatment of the tax already deducted depends on the facts and the timing, and practice varies. This is unsettled ground. Do not assume it can be adjusted or refunded — take the specific facts to your tax advisor before you structure the recovery.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Deduction Management: Challenges, Best Practices and the AR Deductions Process

The AR deductions process — 6-stage lifecycle, the 7 biggest deduction management challenges, invalid-deduction recovery and a best-practice checklist.

What is a Billback? Meaning, Process and How It Differs from a Chargeback

Billback meaning in plain English — how billbacks work, billback pricing, a worked example, and billback vs chargeback in Indian channels.

CPQ Software vs. Rebate and Claims Management: Which Do You Actually Need?

CPQ meaning, in one line: Configure-Price-Quote software for pre-sale quoting. Here is how it differs from post-sale rebate and claims management.