Returns, Reversals and Cancellations in Channel Claims

How to reverse a settled claim, cancel a claim, handle returns and correct mistakes — the document, the entry and the audit trail for each.

Channel claims change after settlement more often than anyone plans for. Goods come back, a scheme is withdrawn, a duplicate is caught, an amount was wrong. None of that is unusual — it is the normal life of a claim. What matters is choosing the right correction route and leaving an audit trail behind it. Pick the wrong route — delete instead of reverse, net without a record, fix it in a spreadsheet — and the problem does not go away. It resurfaces months later as a tax mismatch or a reconciliation gap nobody can explain. This is the operations guide to getting each correction right.

The mechanics below assume you already know how a claim gets raised, approved and settled in the first place; if not, start with how the claim process works and come back.

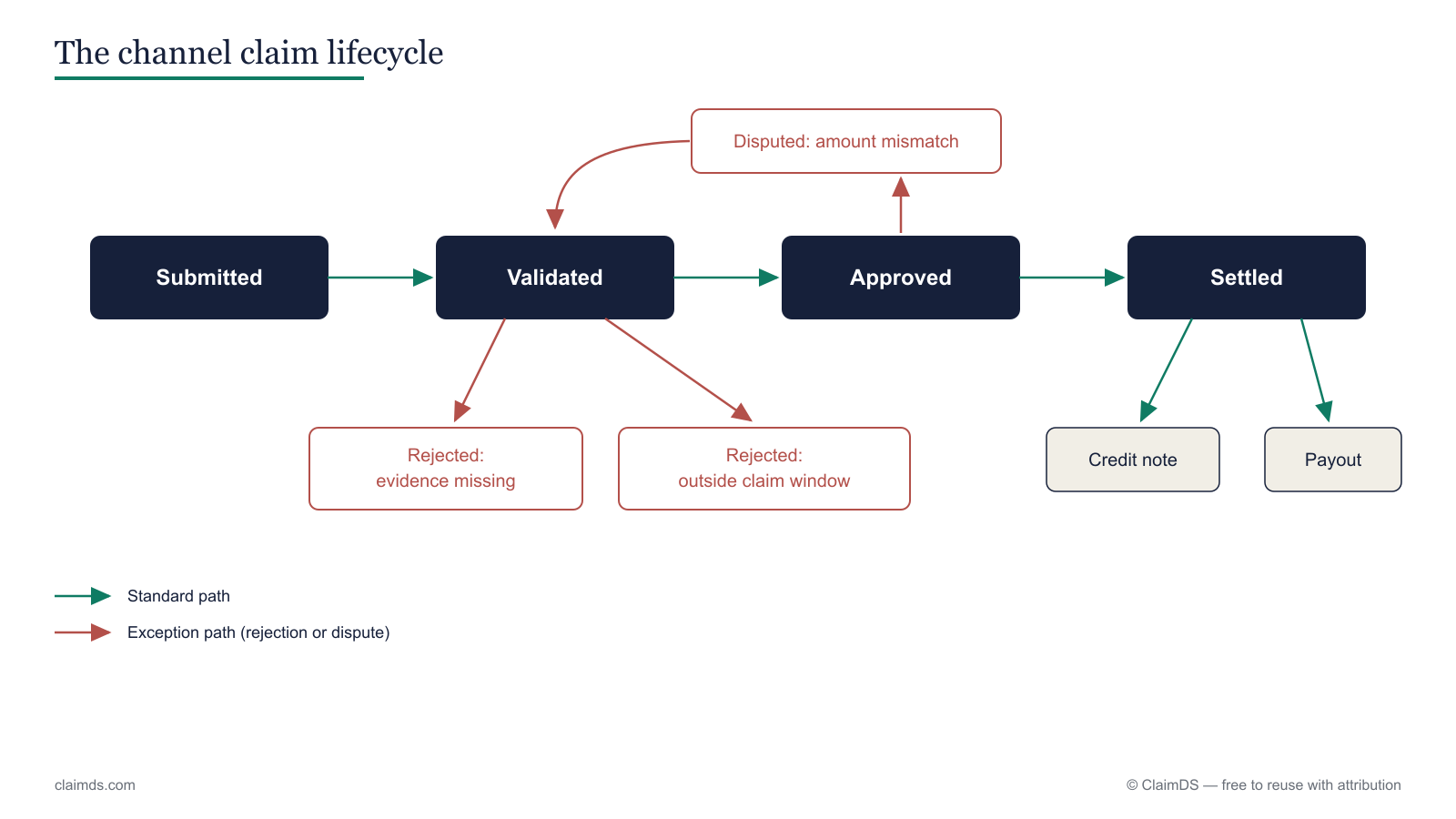

The claim status model: cancelled vs reversed vs reopened vs amended

The single rule that governs everything here: a settled claim is never deleted — it is reversed with a linked correcting record. Deletion destroys the trail; reversal preserves it. Everything else is about choosing the right status transition for where the claim currently sits.

A reversal never deletes the settled claim — it records a linked correcting entry against it.

Four words get used loosely on the shop floor. They are not interchangeable, and the difference decides which document you issue.

Cancelled. The claim is voided before it settles. No money and no credit note have moved, so there is nothing to unwind — you simply stop it, record a reason, and it never reaches settlement. Cancellation is only available pre-settlement. The product-side rules for this are in cancel a claim.

Reversed. The claim has already settled and now has to be undone or corrected. You cannot cancel it — the value is gone — so you raise a linked correcting entry (credit note, debit note or recovery) that reverses the financial effect while the original claim stays on file, fully visible. See reversals explained for the record structure.

Reopened. A settled or rejected claim is brought back into an active state so it can be re-worked — typically after a dispute or new evidence. Reopening changes the claim's status but does not, by itself, move any money; a reversal or a fresh settlement follows.

Amended. A claim that has not yet settled is edited — quantity, rate, evidence — and then continues through approval on its corrected figures. Amendment changes the claim in place; once settled, you can no longer amend, only reverse. The distinction between editing before settlement and correcting after it is covered in changing a claim after submission.

The practical test is always the same: has value moved yet? If no — cancel or amend. If yes — reverse, with a linked record. Keeping these four apart is what keeps the audit trail honest.

Eight reversal scenarios and what each one requires

Every correction below follows one shape: a trigger, a person who initiates, a decision, a document route, an effect on the claim record, and an audit-trail requirement. The two-column table under each scenario shows the paperwork at pointer level — the exact GST treatment routes to GST adjustments on channel settlements, which is the tax companion to this operations guide.

(a) Duplicate claim found after settlement

Trigger: the same underlying event — one invoice, one scheme period, one return — has been claimed and settled twice. Often caught in reconciliation when two claim references point at the same document. Who initiates: the finance or claims team that spots the overlap. Decision: confirm which claim is the valid one and which is the duplicate; the duplicate is reversed in full, not the original. Document route: a debit note to the distributor for the duplicated value, or netting against the next payout if the relationship is ongoing. Claim-record effect: the duplicate claim moves to reversed, linked to the surviving claim reference so the pair is legible. Audit-trail requirement: reason code "duplicate", the surviving claim reference, and the recovery document number. Tight deduction-management practice is what surfaces duplicates before they settle twice.

| In the manufacturer / brand books | In the distributor / dealer / retailer books |

|---|---|

| Issues a debit note for the duplicated amount (or nets the next payout) | Receives the debit note; accepts the recovery against its account |

| Duplicate claim record set to reversed, linked to the valid claim | Reverses the duplicated credit it had taken |

| Accounting effect: reduces the over-credited expense, restores the receivable | Accounting effect: reduces the income/credit it had booked twice |

(b) Overpaid or excess amount settled

Trigger: the claim was valid but settled for more than it should have been — a rate applied too high, a quantity overstated, a slab misread. Who initiates: whoever finds the gap, usually finance during payout reconciliation. Decision: quantify the excess only; the correct portion of the claim stands, so you never reverse the whole claim. Document route: a debit note for the excess, netting against the next approved payout, or a direct refund if the distributor pays it back. Claim-record effect: a partial reversal entry for the excess amount, linked to the original claim, which itself stays settled for the correct value. Audit-trail requirement: reason code "overpayment", the recomputed correct value, and the recovery document. Recovering an excess is a routine cousin of a billback recovery — same discipline, opposite direction.

| In the manufacturer / brand books | In the distributor / dealer / retailer books |

|---|---|

| Raises a debit note for the excess only, or nets it forward | Receives the debit note for the over-settled portion |

| Original claim stays settled at corrected value; excess sits as a linked reversal | Reduces the credit taken down to the correct amount |

| Accounting effect: recovers the over-paid expense | Accounting effect: reverses the excess income booked |

(c) Claim rejected, corrected and re-submitted

Trigger: a claim was rejected for a fixable defect — wrong proof, missing invoice, a computation slip — and the distributor wants to try again. Who initiates: the distributor, after the rejection reason is communicated. Decision: this is not a reversal at all — nothing settled — so the rejected claim is closed and a fresh, corrected claim is raised. Document route: none on the rejected claim; the new claim runs the normal settlement route if approved. Claim-record effect: the rejected claim stays rejected (never deleted); the resubmission is a new record that should reference the rejected one. Audit-trail requirement: rejection reason code on the original, and a link from the new claim to the one it replaces, so the history is traceable through the claim approval workflow.

| In the manufacturer / brand books | In the distributor / dealer / retailer books |

|---|---|

| No document on the rejected claim; processes the fresh claim normally | Raises a corrected claim referencing the rejected one |

| Rejected record retained; new claim linked to it | Retains the rejection notice; tracks the resubmission separately |

| Accounting effect: none until the new claim settles | Accounting effect: none until the new claim is credited |

(d) Partial approval — approved for less than claimed

Trigger: the reviewer accepts part of a claim and disallows the rest — a quantity trimmed, an ineligible SKU removed, a rate capped. Who initiates: the approver during review. Decision: settle the approved portion; record the disallowed portion with a reason rather than silently dropping it. Document route: a credit note for the approved value only; the shortfall is not paid. Claim-record effect: the claim settles at the approved amount, with the disallowed delta captured against the same record so the distributor can see what was cut and why. Audit-trail requirement: the claimed-vs-approved figures, the disallowance reason, and the approver. Getting the claimed figure right in the first place is a matter of how FMCG distributor claims are calculated; partial approvals fall when the two sides compute differently.

| In the manufacturer / brand books | In the distributor / dealer / retailer books |

|---|---|

| Issues a credit note for the approved portion only | Receives credit for the approved value; sees the disallowed delta |

| Claim settled at approved amount; disallowed delta recorded with reason | Books the credit actually received, not the amount claimed |

| Accounting effect: expense recognised at approved value | Accounting effect: income booked at credited value; writes off or disputes the rest |

(e) Calculation error found after settlement

Trigger: a genuine arithmetic or rate-table error is discovered after the claim settled — the direction can be either way, over or under. Who initiates: finance or audit, on review. Decision: recompute correctly, then move only the difference; if the distributor was underpaid you owe them, if overpaid you recover. Document route: a credit note for a top-up, a debit note for a recovery — never a re-settlement of the whole claim. Claim-record effect: a linked correcting entry for the delta, with the corrected computation attached; the original claim stays settled. Audit-trail requirement: reason code "calculation correction", the before and after figures, and the approver — reversals that move money in either direction need the same rigour. An illustrative case: a claim settled at ₹48,000 against a correct ₹42,000 leaves a ₹6,000 recovery (figure illustrative only).

| In the manufacturer / brand books | In the distributor / dealer / retailer books |

|---|---|

| Top-up: credit note for the shortfall. Recovery: debit note for the excess | Receives the matching credit or debit note |

| Original claim stays settled; delta booked as a linked correction | Adjusts its recorded credit up or down by the delta |

| Accounting effect: corrects the expense by the difference only | Accounting effect: corrects the income by the difference only |

(f) Goods returned after the claim was settled

Trigger: stock tied to an already-settled claim comes back from the channel — the scheme benefit was earned on goods that no longer sit with the buyer. Who initiates: the distributor or retailer raising the return; finance links it to the prior claim. Decision: decide whether the earlier claim benefit must be unwound for the returned quantity, and whether the return is replaced or credited. Document route: a return document for the goods, plus a credit note (or replacement) for the return itself — and a linked reversal on the claim if the benefit no longer holds. Claim-record effect: a partial reversal proportional to the returned quantity, linked to both the original claim and the return document. Audit-trail requirement: the return reference, the quantity, and the claim-linkage. The returns mechanics and their evidence sit in credit notes for expired and damaged goods returns.

| In the manufacturer / brand books | In the distributor / dealer / retailer books |

|---|---|

| Receives goods on a return document; issues credit note or replacement | Sends goods back on a return document; receives credit or replacement |

| Claim partially reversed for the returned quantity, linked to the return | Reverses the scheme benefit on the returned units |

| Accounting effect: reduces sale and reverses the related scheme cost | Accounting effect: reverses purchase and the credit taken on those units |

(g) Scheme cancelled or amended after claims filed

Trigger: a scheme is withdrawn, capped or retrospectively changed after distributors have already filed claims against it. Who initiates: the brand's trade-marketing or finance team announces the change; claims already in flight are re-assessed. Decision: at the operations level, decide which filed claims are still valid, which are void, and which need re-computation on the new terms. Document route: cancellation for unsettled claims that are now void; reversal with a recovery document for settled claims that must be clawed back. Claim-record effect: affected claims move to cancelled or reversed against the scheme-change reference. Audit-trail requirement: the scheme-amendment reference and a reason code linking every affected claim to it. The deeper clawback mechanics — how far back you can reach, and on what basis — belong in rebate clawbacks on scheme cancellations; the scheme structures themselves are in types of trade schemes in India.

| In the manufacturer / brand books | In the distributor / dealer / retailer books |

|---|---|

| Unsettled claims cancelled; settled claims reversed via debit note / netting | Void claims dropped; clawed-back credits repaid or netted |

| Each affected claim linked to the scheme-amendment reference | Adjusts booked incentives to the revised scheme terms |

| Accounting effect: reverses accrued or paid scheme cost | Accounting effect: reverses the incentive income recognised |

(h) Deduction reversed — short-payment withdrawn or invalid deduction recovered

Trigger: a customer withdraws a short-payment they had taken, or an invalid deduction is challenged and recovered. Who initiates: the deductions or receivables team working the open item. Decision: confirm the deduction was invalid or withdrawn, then restore the receivable. Document route: reverse the deduction — a debit note back to the customer, or a netting entry that restores the amount — and close the deduction as recovered. Claim-record effect: the deduction record moves to reversed/recovered, linked to the originating invoice and any related claim. Audit-trail requirement: reason code, the original deduction reference, and the recovery document. Working invalid deductions to closure is the heart of deduction-management best practice.

| In the manufacturer / brand books | In the distributor / dealer / retailer books |

|---|---|

| Reverses the deduction; issues debit note or restores the receivable | Withdraws the short-payment or repays the invalid deduction |

| Deduction record set to recovered, linked to the invoice | Clears the disputed open item on its side |

| Accounting effect: restores the receivable written down earlier | Accounting effect: reverses the deduction it had taken |

The returns taxonomy

Not every return is the same event, and the evidence each one needs differs. Classifying the return correctly is the first decision, because it drives whether stock re-enters inventory, gets destroyed, or goes back up the chain — and which document follows.

Saleable return. Stock still fit for resale — in date, undamaged, in original packaging. It re-enters inventory. Evidence: a return note listing SKUs and batches, and a condition check confirming saleable status.

Non-saleable return. Stock that cannot be resold — opened, defaced, part-used, or failing a quality check. It is written off or sent for destruction. Evidence: a condition/quality report and a disposal or destruction record.

Expiry return. Goods returned because they have passed, or are near, their expiry date. Evidence: batch and expiry data on the return note, and a destruction certificate if destroyed rather than resold; the GST routing for these is in credit notes for expired and damaged goods returns.

Damage return. Stock damaged in handling or storage. Evidence: photographs, a damage report, and batch references.

Breakage. A sub-type of damage for fragile lines broken in transit or handling — often destroyed in the field rather than moved. Evidence: a breakage note and a field-destruction record.

Transit shortage. Quantity received is short of quantity dispatched. Evidence: the gate/receipt note against the dispatch document, and the transporter's acknowledgement of the short-delivery.

Destroy-in-field. Goods never come back; they are destroyed at the channel location against a certificate, and the supplier compensates by credit. Evidence: a dated, signed destruction certificate with batch detail.

Return to vendor (RTV). In modern trade, a retailer sends stock back to the supplier under a contractual return clause — delisting, non-performance or an agreed buyback. Evidence: the RTV document referencing the contract term, plus the credit note.

Near-expiry return. Stock returned before expiry under a shelf-life policy, to swap for fresh stock. Evidence: the shelf-life policy reference and current batch/expiry data.

| Return type | Fit for resale? | Typical evidence | Usual settlement |

|---|---|---|---|

| Saleable | Yes | Return note, condition check | Re-enter stock; credit or replace |

| Non-saleable | No | Quality report, disposal record | Write-off; credit note |

| Expiry | Sometimes destroyed | Batch/expiry data, destruction certificate | Credit note or replacement |

| Damage / breakage | No | Photos, damage/breakage report | Credit note; field destruction |

| Transit shortage | N/A | Gate note vs dispatch, transporter ack | Credit for short quantity |

| Destroy-in-field | No (never moves) | Signed destruction certificate | Compensating credit note |

| RTV (modern trade) | Varies | RTV doc, contract clause | Credit note; buyback |

| Near-expiry | Yes, if swapped | Shelf-life policy, batch data | Replacement stock |

Replacement or credit note?

When goods come back, you settle the return one of two ways — send fresh stock (replacement) or adjust value (credit note) — and the choice changes the claim record, the stock ledgers and the tax document.

A replacement keeps the original sale intact. Fresh stock goes out against the return; the claim value is settled in goods, not money. Stock records move on both sides — the returned units leave the buyer, the replacement units arrive — and the original invoice stands. Replacements suit saleable swaps, near-expiry shelf-life exchanges, and cases where the buyer still wants the product. The claim record shows the return matched to an outbound replacement, with no ledger credit.

A credit note settles in value. No goods go back out; instead the account is reduced. Here the fork that matters most is whether it is a financial (commercial) credit note that touches only the ledgers, or a tax credit note that adjusts GST — a distinction with real consequences, laid out in financial vs tax credit notes under GST. A credit note reduces the original sale; a replacement does not. That single difference is why the tax document diverges, and the exact GST treatment for each is in GST adjustments on channel settlements.

Use a replacement when the buyer wants product and stock is available; use a credit note when they want value back, when no equivalent stock exists, or when the relationship is being wound down. Record which one you chose on the claim — an auditor should never have to guess whether a return was replaced or credited.

Buyback vs return vs exchange

In this article "buyback" means a manufacturer taking back its own channel stock — slow-moving, delisted or end-of-scheme goods bought back from a distributor or retailer. It is not a share buyback, where a company repurchases its own equity from shareholders; that is a corporate-finance transaction with no connection to channel claims, and nothing here applies to it. With that cleared up, the three channel events below are easy to confuse but settle differently. The mechanics of the channel version are in the buyback process and supplier buybacks.

| Dimension | Buyback | Return | Exchange |

|---|---|---|---|

| What happens | Manufacturer purchases back channel stock | Buyer sends stock back for credit or replacement | Stock swapped for equivalent fresh stock |

| Why | Delisting, slow-movers, end-of-scheme cleanup | Expiry, damage, shortage, non-performance | Near-expiry or shelf-life refresh |

| Initiated by | Manufacturer (often pre-agreed) | Buyer | Either, under a swap policy |

| Money moves? | Yes — buyback price paid | Usually — credit note | Usually not — value-neutral swap |

| Claim record | Buyback claim, priced | Return linked to prior claim | Return matched to replacement |

Evidence and audit trail for reversals

A reversal is only as good as the record behind it — capture the full chain or the correction will not survive an audit. Every reversal, whatever the scenario above, should carry the same fields:

- Original claim reference — the claim being corrected, so the pair is legible.

- Reason code — duplicate, overpayment, calculation correction, return, scheme change, deduction recovery. Free-text reasons are not enough; codes let you report on why reversals happen.

- Approver — the name and role of who authorised it, distinct from who raised it.

- Linked document number — the credit note, debit note or netting entry that carries the financial effect.

- Date — when the reversal was authorised and when it settled.

- Evidence files — return notes, destruction certificates, recomputations, correspondence.

Every reversal links back to the original claim record — its reference, reason code and approver.

Reversals need a higher approval level than the original claim, for a simple reason: they move money that has already left the books, and they are a favourite route for both honest error and deliberate abuse. The approval design for this — who signs off at what threshold, and why reversals escalate — is in claim and rebate approval workflows. Whoever approves a reversal should be independent of whoever raised or settled the original claim. <!-- TODO: confirm capability wording with founder -->

Where reversals go wrong

Five failure modes account for most of the reconciliation pain teams feel months later. Each has a direct fix.

- Deleting instead of reversing. The claim vanishes and the trail with it, so nothing ties back to the money that moved. Fix: never delete a settled claim — reverse it with a linked record, always.

- Reversing the claim but not the credit note (or vice versa). The claim record and the tax/financial document drift apart, and GST returns stop matching the ledger. Fix: treat the claim reversal and its document as one atomic action — neither is done until both are.

- Netting without a linked record. An excess is quietly netted against the next payout with no reference to the claim it corrects, and no one can later reconstruct why the payout was short. Fix: every netting entry carries the original claim reference and a reason code.

- No reason codes. Reversals are logged with free-text or nothing, so you cannot see whether you have a duplicates problem, a calculation problem or a scheme-design problem. Fix: enforce a fixed reason-code list on every reversal.

- Reversals done in spreadsheets outside the system. The correction lives in someone's file, invisible to the claim record and to audit. Fix: every reversal happens against the claim in the system of record, never in a side spreadsheet. Sound deduction-management practice and disciplined reconciliation against GSTR-2B and 3B both depend on this.

Tax follows the document

The GST consequence of any reversal depends entirely on which document you issue — a credit note, a debit note, or a value-neutral replacement each land differently. This article stays at the operations level and names the documents; it does not work the tax. For the actual treatment — output-tax adjustment windows, ITC reversal, and how each document flows into the returns — go to GST adjustments on channel settlements, which is written as the tax companion to this guide. The broader tax picture across rebates, chargebacks, billbacks and buybacks is in tax on rebates, chargebacks, billbacks and buybacks in India, and the post-sale ITC-reversal angle in ITC reversal on post-sale discounts and credit notes.

This is general information, not tax advice — confirm the current position with a qualified professional before you act on it.

Getting returns, reversals and cancellations right is not about heroics at month-end; it is about routing each correction the right way the first time and leaving the record behind it. A system that forces a reason code, links every reversal to its claim and its document, and escalates approvals is what keeps the physical, financial and tax trails aligned. See how ClaimDS structures the claim record, reversal linkage and approval chain end to end.

Frequently asked questions

How do you reverse a settled claim?

You never delete it. Raise a linked correcting entry against the original claim that carries a reason code, an approver and a settlement document — a credit note, a debit note or a recovery from the next payout. The original claim stays visible in full; the reversal record sits beside it so the physical, financial and tax trails stay reconcilable months later.

Can a claim be cancelled after approval?

Before any money or credit note moves, yes — cancellation is the right route, and it simply voids the claim with a reason so it never settles. Once value has changed hands, cancellation is the wrong route: the claim is already settled, so you reverse it with a linked correcting document instead. The dividing line is whether settlement has happened, not whether approval has.

What is the difference between cancelling and reversing a claim?

Cancelling stops a claim that has not yet settled — it voids the record before value moves, leaving nothing to unwind. Reversing corrects a claim that has already settled — it issues a linked document that undoes the financial effect while the original claim stays on file. Cancel is pre-settlement and clean; reverse is post-settlement and always leaves a paired record.

How do you recover an overpaid claim from a distributor?

Three routes. Issue a debit note to the distributor for the excess, net the excess against the next approved payout, or take a direct recovery if they refund it. Whichever you pick, link it to the original claim with a reason code and keep the document number. Netting without a linked record is the classic mistake that breaks reconciliation later.

What happens when goods are returned after a claim is settled?

The return and the earlier claim are separate events that must be reconciled. The goods come back on a return document, and the settled claim may need a reversal if the scheme benefit was tied to stock that no longer sits with the buyer. Whether you replace the stock or issue a credit note decides which tax document follows — so record both the return and the claim effect.

What is the difference between a replacement and a credit note?

A replacement sends fresh stock in place of what came back — the claim value is settled in goods, and stock records move on both sides. A credit note settles in money or ledger value — no goods move, and a tax or financial document adjusts the account. Replacement keeps the sale intact; a credit note reduces it. The choice drives the GST document you must issue.

What is a saleable return?

A saleable return is stock the channel sends back that is still fit for resale — undamaged, in date and in original packaging — so it can re-enter inventory rather than be destroyed. It is treated differently from expiry, damage or breakage returns because no write-off is involved; the goods simply move back up the chain and the claim or credit adjusts the original sale value.

What is RTV (return to vendor)?

RTV, return to vendor, is when a retailer or modern-trade buyer sends stock back to the supplier — for non-performance, a delisting, expiry, or an agreed buyback of slow-moving lines. It is common in organised retail, where contracts set the return terms up front. RTV drives a return document and often a credit note; the linked claim record must reference both so nothing settles twice.

Who should approve a claim reversal?

A reversal should sit at a higher approval level than the original claim, because it moves money that has already left the books and it is a favourite route for error and fraud. The approver should be independent of whoever raised or settled the original claim, and the approval — name, date and reason code — must be captured on the reversal record itself.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

How to Calculate FMCG Distributor Claims (With Worked Examples)

How to calculate FMCG distributor claims — scheme slabs, secondary schemes, damage, price drops and display claims, with worked examples in ₹.

Designing Claim and Rebate Approval Workflows That Don’t Bottleneck Settlement

How to design claim and rebate approval workflows — role-based routing, authority thresholds, SLAs and escalation that keep settlement moving.

Distributor Claims Software: Buyer's Guide for Indian Businesses

A vendor-neutral buyer's guide to distributor claims software for India — top features, benefits, FMCG fit and an evaluation scorecard.