Tax on Rebates, Chargebacks, Billbacks and Buybacks in India

How each channel settlement is taxed in India — rebates, chargebacks, billbacks, buybacks and MDF — GST and TDS for both payer and receiver.

Channel settlements are taxed by instrument and document, not by what your teams call them. The same ₹1,00,000 of channel support can settle four ways — a GST (tax) credit note, a financial credit note, a payout that attracts TDS, or a service invoice — and each carries a different tax outcome. A rebate, a chargeback and a billback can all end up as the same credit note, or as three different instruments. This guide maps every channel settlement instrument to its GST and TDS treatment in India, from both sides of the ledger — the manufacturer or supplier who pays, and the distributor, dealer or retailer who receives.

GST note: This is general information, not tax or legal advice. Every position below must be re-verified at publish time with a qualified professional. Where the Finance Act 2026 is relevant it is noted only as enacted but awaiting commencement notification — not yet in force.

The master matrix — how is each channel settlement taxed?

Each instrument below maps to a settlement document, and the document decides both the GST and the TDS. Read this table as a pointer, then jump to the section that matches your instrument for the worked detail.

| Instrument | Typical settlement document | GST treatment (pointer) | TDS (194R) relevance | Receiver-side effect |

|---|---|---|---|---|

| Rebate / post-sale discount | Tax or financial credit note | Section 15(3)(b) conditions decide if value can be reduced | Cash rebate usually outside 194R; benefit-in-kind may attract it | ITC reversal only on a tax credit note — see ITC reversal on post-sale discounts |

| Chargeback / deduction | Distributor debit note; manufacturer credit note | Follows the credit note actually issued, not the memo | Not a benefit; generally no 194R | ITC effect follows the note — see deduction management best practices |

| Billback / rate difference | Credit note raised against the claim | Financial vs tax credit note choice | Usually none | ITC reversal only if a tax credit note — see what is a billback |

| Buyback / return | Section 34 credit note; delivery challan / e-way bill for movement | Genuine return reverses the original GST | None on the return itself | ITC reversal if goods are destroyed — see credit notes for expired and damaged goods |

| Price protection | Credit note for the rate drop | See price-protection rate-difference credit notes | Usually none | Mirrors the credit-note type issued |

| MDF / marketing support | Credit note, or dealer service invoice | Characterisation-dependent — see MDF and co-op claims | Benefit-in-kind may attract 194R | ITC to manufacturer only on a valid service invoice |

| Incentive in kind (goods / trips / gifts) | Payout memo or free-goods note | Free goods raise separate valuation questions | Section 194R likely applies | Recipient taxed on the benefit value |

The rest of this guide takes each row in turn. For the underlying scheme mechanics, see types of trade schemes in India and secondary scheme settlement; for the plain-language definitions, see what is a rebate and the chargeback process.

How is GST applied on rebates and post-sale discounts?

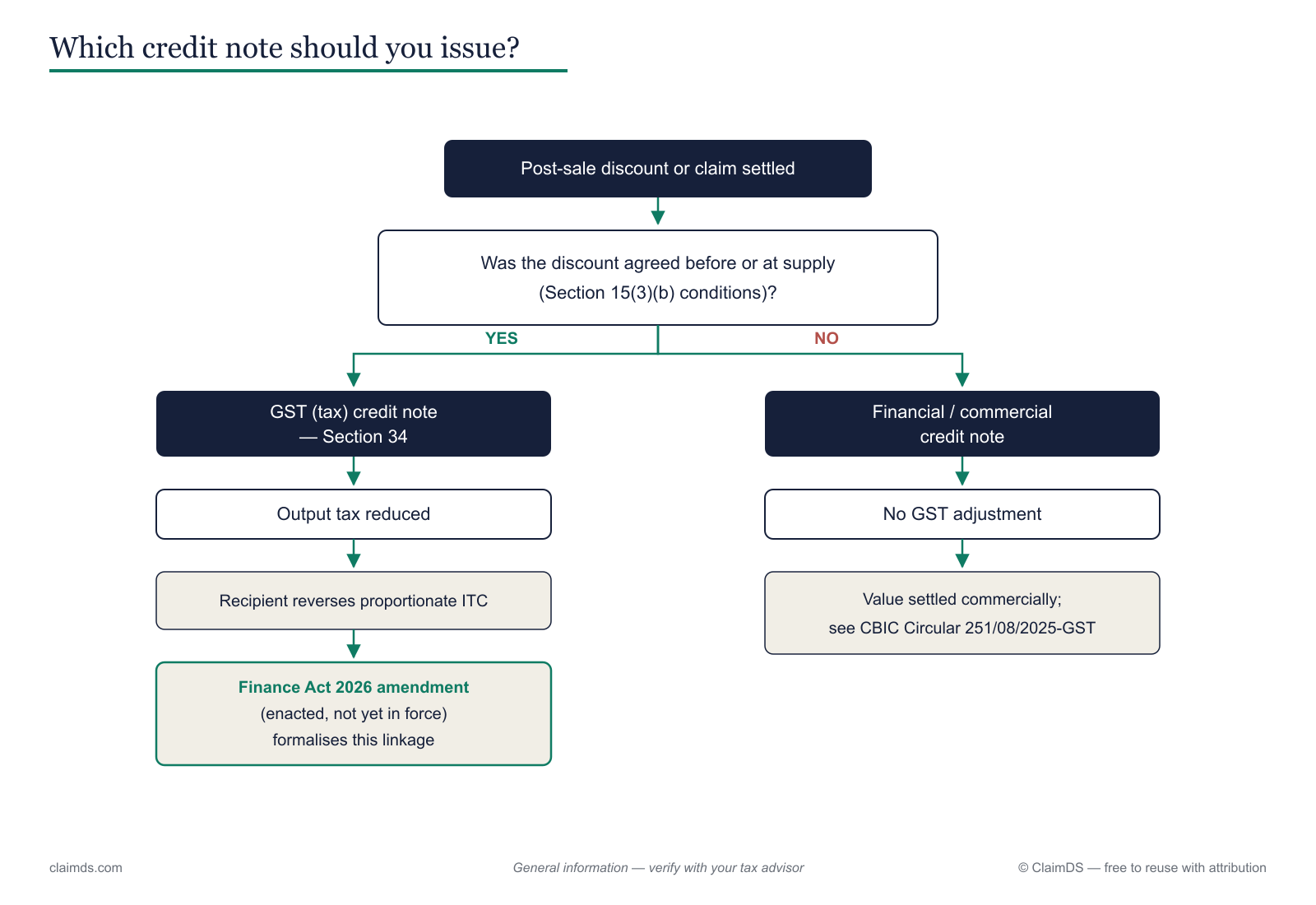

Which credit note applies depends on whether the discount met the Section 15(3)(b) conditions agreed before supply.

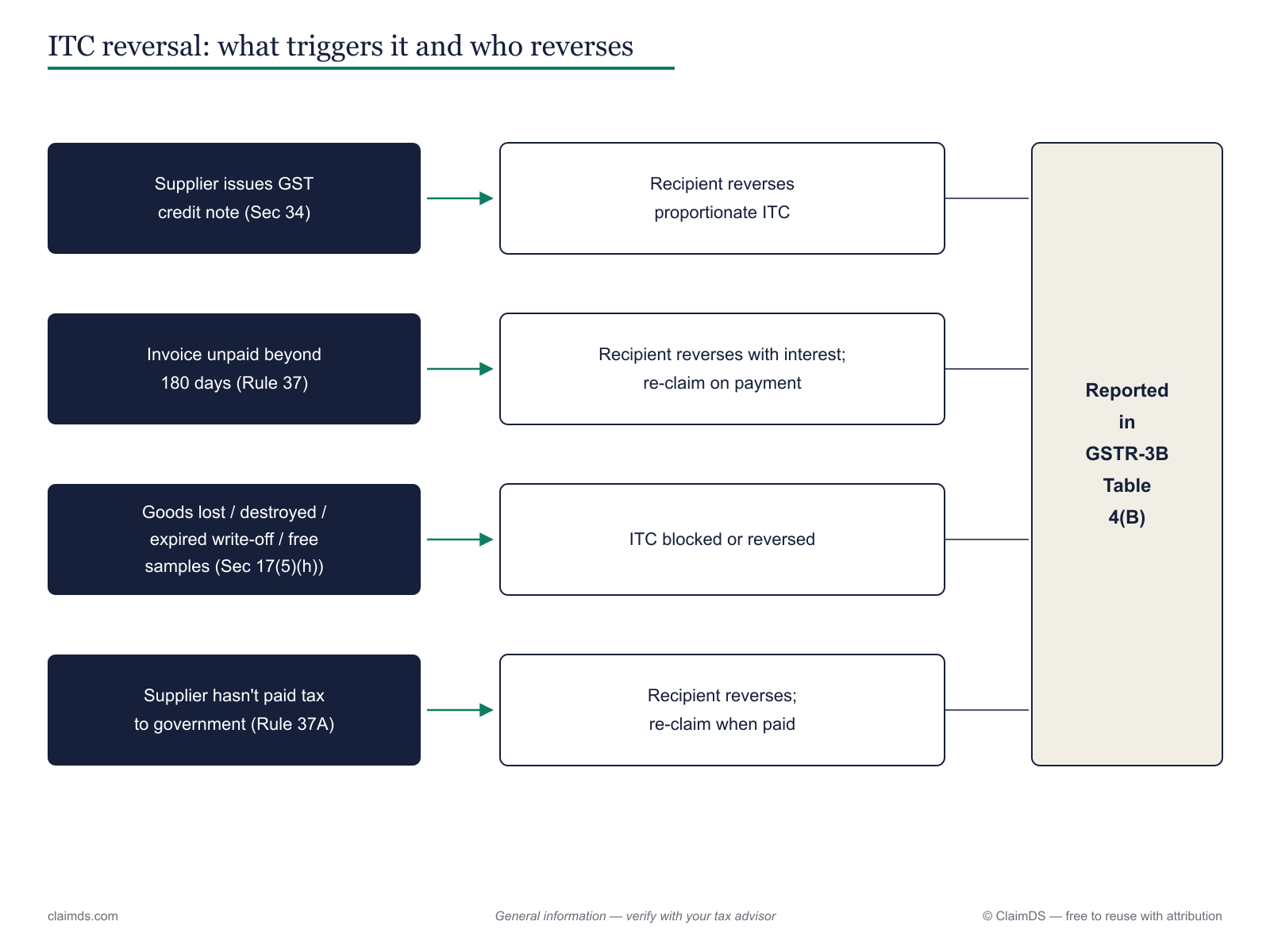

A post-sale rebate reduces GST only when it is settled through a tax credit note under Section 34 of the CGST Act — and only when the Section 15(3)(b) conditions are met. Section 15(3)(b) lets a supplier exclude a post-supply discount from the taxable value on three cumulative conditions: the discount was established in an agreement entered into before or at the time of supply, it is linked to specific invoices, and the recipient reverses the input tax credit attributable to it. Miss any one condition and the discount cannot leave the taxable value.

That single test forks into two instruments. A tax credit note under Section 34 reduces the supplier's output tax and obliges the recipient to reverse proportionate ITC. A financial (commercial) credit note does neither — it settles the money without touching either party's GST. The recipient-side consequence is the crux, and it runs through the ITC reversal on post-sale discounts mechanics; the two-instrument choice is unpacked in financial vs tax credit notes under GST, with the Rule 53(1A) content requirements in GST credit notes for rebates. The current administrative position on all of this sits in CBIC Circular 251/08/2025-GST on post-sale discounts.

Worked example (illustrative). A distributor buys ₹10,00,000 of net purchases in a quarter and earns a 3% rebate — that is ₹30,000.

- (a) Settled as a GST (tax) credit note. The ₹30,000 is treated as a reduction in taxable value. At an illustrative rate of 18%, the GST adjusted is ₹30,000 × 18% = ₹5,400, so the tax credit note reads ₹30,000 taxable value plus ₹5,400 GST = ₹35,400 total. The manufacturer reduces output tax by ₹5,400; the distributor reverses ₹5,400 of ITC.

- (b) Settled as a financial credit note. A single credit note of ₹30,000 with no tax line. Output tax is unchanged, and the distributor reverses no ITC — a financial credit note attracts no GST.

- (c) Settled as a payout. A ₹30,000 bank transfer with no GST credit-note document at all. This route sidesteps the credit-note mechanics entirely, but the benefit-in-kind rule (below) must be checked before assuming it is tax-neutral.

How to calculate GST on a rebate (the arithmetic). Start from the rebate base: ₹10,00,000 × 3% = ₹30,000 taxable value. Apply the illustrative 18% rate to that base: ₹30,000 × 18% = ₹5,400. The taxable value is ₹30,000 and the credit-note (invoice) value is ₹35,400 — the two are not the same number, and only the ₹5,400 tax component moves through GST returns. On a financial credit note, there is no rate to apply and nothing to calculate. The accrual side of these numbers is covered in rebate accounting with GST credit notes, and the FMCG claim maths in calculating FMCG distributor claims.

Rebates and post-sale discounts — both sides of the ledger

| In the manufacturer / supplier books (payer) | In the distributor / dealer / retailer books (receiver) | |

|---|---|---|

| Document | Issues a tax or financial credit note | Receives the credit note; issues no GST document of its own |

| GST effect | Output tax reduced only on a tax credit note under Section 34 | Reverses proportionate ITC only against a tax credit note |

| Accounting nature | Reduction of revenue or rebate expense — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> | Reduction of purchase cost or other income — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> |

For the broader trade-discount framing, see GST on trade discounts and dealer incentives.

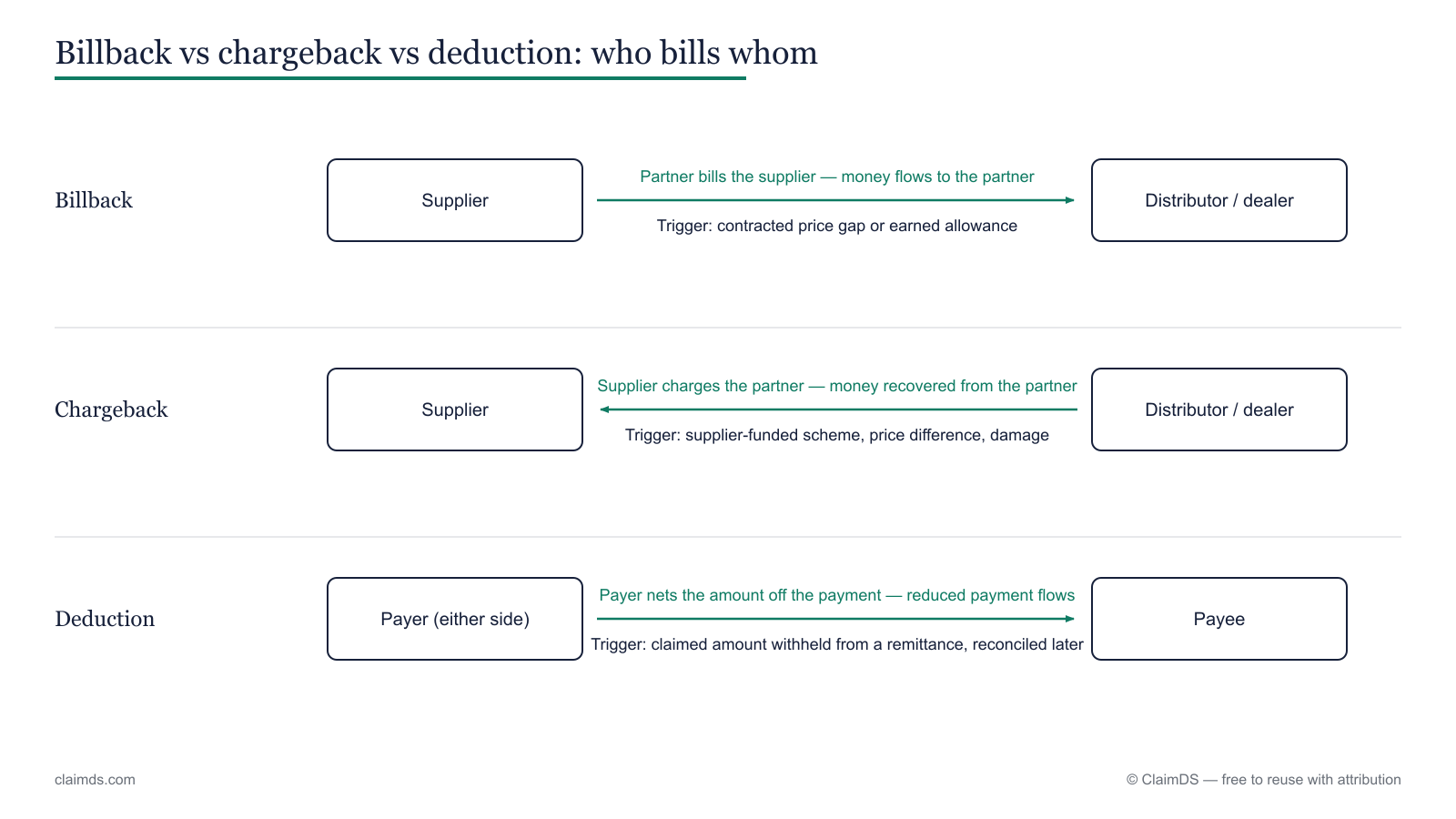

Is there tax on chargebacks and deductions?

A chargeback is a deduction, not a taxable supply — so its GST effect follows the credit note that finally resolves it, never the deduction memo. In the field, a distributor short-pays or debits the manufacturer for a claim it believes it is owed. That debit note or deduction memo is an accounts-receivable event. It does not, by itself, move any GST. The question that decides the tax is which instrument the manufacturer issues to close the claim: a tax credit note under Section 34 (GST adjusts, recipient reverses ITC) or a financial credit note (nothing moves for GST). The document, not the deduction, governs — the same principle set out in financial vs tax credit notes.

Two practical wrinkles matter. First, unresolved deductions leave the manufacturer holding an open receivable while the distributor has already taken the cash; where the underlying invoice remains unpaid beyond the statutory window, the Rule 37 180-day ITC reversal can bite on the recipient side, so ageing deductions has a tax dimension, not only a working-capital one. Second, disciplined deduction management best practices — matching each deduction to a validated claim before a credit note is cut — is what keeps the GST treatment defensible.

A disambiguation: the phrase chargeback rebates is sometimes used loosely to mean a rebate that a distributor recovers by charging it back to the manufacturer. That is still, in substance, a rebate settled by a credit note — treat it under the rebate rules above, not as a separate instrument. The chargeback process itself is a claims-and-deduction workflow; the tax attaches only at the credit-note step.

Chargebacks and deductions — both sides of the ledger

| In the manufacturer / supplier books (payer) | In the distributor / dealer / retailer books (receiver) | |

|---|---|---|

| Document | Receives a distributor debit note; issues a credit note to settle | Issues a debit note or deduction memo; receives the credit note |

| GST effect | Output tax moves only if the settling note is a tax credit note under Section 34 | Reverses ITC only against a tax credit note; Rule 37 may apply if the invoice stays unpaid |

| Accounting nature | Reduction of revenue against an open receivable — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> | Reduction of payable or purchase cost — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> |

How are billbacks and rate differences taxed?

Billback, chargeback and deduction differ by direction of money and document — and the tax follows the document, not the label.

A billback settles as a credit note, so it faces exactly the same financial-versus-tax choice as a rebate. A billback is a claim the dealer raises for a rate difference the manufacturer agreed to fund — the dealer sold at a supported price and bills the gap back. When the manufacturer accepts the claim, it issues a credit note. If that note is a tax credit note under Section 34 and the Section 15(3)(b) conditions were met, GST adjusts and the dealer reverses proportionate ITC; if it is a financial credit note, neither GST nor ITC moves. The mechanics are identical to a rebate because the settlement instrument is identical. For the concept itself, see what is a billback; for the instrument choice, financial vs tax credit notes.

Worked mini-example (illustrative). A dealer bills back a ₹40,000 rate difference. Routed through a tax credit note at an illustrative 18% rate, the GST adjusted is ₹40,000 × 18% = ₹7,200, and the credit note totals ₹47,200; the manufacturer reduces output tax by ₹7,200 and the dealer reverses ₹7,200 of ITC. Routed through a financial credit note, it is a flat ₹40,000 with no tax line and no reversal.

Billbacks and rate differences — both sides of the ledger

| In the manufacturer / supplier books (payer) | In the distributor / dealer / retailer books (receiver) | |

|---|---|---|

| Document | Receives the billback claim; issues a credit note in response | Raises the billback claim; receives the credit note |

| GST effect | Output tax reduced only on a tax credit note under Section 34 | Reverses proportionate ITC only against a tax credit note |

| Accounting nature | Reduction of revenue or scheme expense — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> | Reduction of purchase cost or scheme income — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> |

Is GST applicable on buybacks and returns?

Destroyed or written-off stock triggers an ITC reversal under Section 17(5)(h); a return runs through a Section 34 credit note instead.

A genuine sales return runs through a Section 34 credit note; stock that is bought back and then destroyed triggers a Section 17(5)(h) ITC reversal instead — and the two are taxed very differently. When goods come back into trade as a real return, the original supplier issues a credit note under Section 34 of the CGST Act, reversing the GST charged on the original supply. The goods physically moving back should travel on a delivery challan, with an e-way bill where the value threshold requires it — the document names matter for defending the movement, even though they are not themselves the tax event.

The picture changes when bought-back stock is expired, damaged or otherwise written off and destroyed rather than resold. Here Section 17(5)(h) blocks input tax credit on goods destroyed or written off, so the party holding the ITC must reverse it. Commercially, who bears that cost is a negotiation: if the manufacturer takes the stock back and destroys it, the manufacturer typically absorbs the reversal; if the dealer scraps it, the dealer does. Getting this right is the subject of credit notes for expired and damaged goods returns.

A third variant is a buyback triggered by a rate change — the manufacturer takes stock back because the price dropped. That is closer to price protection than to a scrap event, and it is generally settled by a credit note for the rate difference; see price-protection rate-difference credit notes under GST. The label buyback covers all three fact patterns, so pin down which one you have before choosing the document.

Buybacks and returns — both sides of the ledger

| In the manufacturer / supplier books (payer) | In the distributor / dealer / retailer books (receiver) | |

|---|---|---|

| Document | Issues a Section 34 credit note; records delivery challan / e-way bill for the inward movement | Receives the credit note; issues the delivery challan for goods sent back |

| GST effect | Original GST reversed on a genuine return; ITC reversed under Section 17(5)(h) if the stock is destroyed | Reverses ITC taken on the returned goods; no output tax on a pure return |

| Accounting nature | Reversal of sale, or write-off of destroyed stock — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> | Reversal of purchase, or scrap loss — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> |

What is the tax treatment of MDF, co-op and marketing support?

<!-- TODO CA REVIEW MANDATORY: characterisation of dealer marketing support (service vs discount) — reviewer to confirm current position and add citations -->The tax treatment of marketing support turns entirely on how the arrangement is characterised, and that characterisation is fact-specific. The same marketing development fund, co-op contribution or promotional support can be seen two fundamentally different ways, and the two lead to opposite GST outcomes.

Under the first characterisation, the support is a discount the manufacturer gives its channel partner, passed through a credit note. It reduces what the partner effectively paid for goods, and it moves through the credit-note machinery like any other post-sale adjustment.

Under the second characterisation, the support is consideration for a service the dealer supplies — advertising, in-store display, local promotion, activation — which the dealer invoices to the manufacturer with GST charged on it. Here the dealer is a service provider, the manufacturer is the recipient of that service, and the manufacturer may be able to claim input tax credit on a valid dealer service invoice. Whether such ITC is actually available depends on the same characterisation question and the validity of the invoice, so treat that too with caution.

The right characterisation is fact-specific — confirm the current position with your CA before relying on it. Because the outcomes diverge so sharply, this is the one area in this guide where you should not lean on a general article at all. For the ClaimDS view of how these claims are captured and settled operationally, see MDF and co-op claims in India — but take the tax characterisation itself to a professional.

Marketing support — both sides of the ledger

| In the manufacturer / supplier books (payer) | In the distributor / dealer / retailer books (receiver) | |

|---|---|---|

| Document | Receives a dealer service invoice, or issues a credit note — depending on characterisation | Issues a service invoice with GST, or receives a credit note — depending on characterisation |

| GST effect | May claim ITC on a valid service invoice; no adjustment on a discount credit note | Charges GST on a service invoice; a discount credit note carries none |

| Accounting nature | Marketing expense, or reduction of revenue — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> | Service income, or reduction of purchase cost — journal entries out of scope <!-- TODO: link journal-entries article when it exists --> |

When does TDS under Section 194R apply?

<!-- TODO VERIFY AT PUBLISH: 194R rate/threshold and Income-tax Act 2025 section mapping -->Section 194R brings TDS on benefits and perquisites given in a business relationship — the classic channel case is a benefit-in-kind, not a cash discount. The distinction that drives it is cash versus benefit-in-kind. A benefit or perquisite provided to a distributor or dealer — free goods over and above what was billed, a foreign trip, a gift, sponsored travel — arising out of the business relationship falls within the provision. TDS is deducted at 10% of the value of the benefit, and the obligation is triggered once the aggregate value of such benefits to a single recipient crosses ₹20,000 in a financial year.

Cash incentives paid straight to a bank account are usually looked at under other provisions rather than 194R, but the line between a genuine price discount and a disguised benefit is exactly where disputes arise — so the characterisation of the scheme matters here as much as it does for MDF. The provision now sits within the broader Income-tax Act 2025 framework, and both the section mapping and the figures should be re-checked at publish time. The detailed treatment is in Section 194R TDS on dealer and distributor incentives.

The document decides the tax

A channel claim is only settled when a document is chosen — and the tax follows that document, every time. Claim raised, document chosen, tax determined: that is the whole chain. A rebate, a chargeback, a billback and a buyback can each end as a tax credit note, a financial credit note, a payout or (for marketing support) a service invoice — and the GST and TDS consequences are set by which one you pick, not by the label on the scheme. This is why a settlement system has to record the instrument and the document type per claim, not just the amount. In ClaimDS, a claim is validated and then settled by a recorded credit note or payout, so the tax-determining fact is captured at settlement rather than reconstructed later. <!-- TODO: confirm capability wording with founder --> The operational walkthroughs are in run a settlement, the credit-note reference and the ITC reversal lifecycle.

In ClaimDS, a settlement records the instrument and document type per claim — the fact that decides the tax.

This is general information, not tax or legal advice — consult a qualified professional. <!-- TODO: CA/CMA reviewer name and credential before publish -->

Ready to make every settlement record its own instrument and document type, so the tax treatment is never guessed after the fact?

Frequently asked questions

Is GST applicable on rebates?

It depends on the document. A rebate given through a tax credit note under Section 34 of the CGST Act reduces the supplier's output tax, so GST is adjusted. A rebate settled through a financial credit note leaves GST untouched. The instrument chosen, not the word rebate, decides whether GST moves.

How do you calculate GST on a rebate?

Only when the rebate is settled through a tax credit note. Treat the rebate as a reduction in taxable value and apply the applicable GST rate. On a ₹30,000 rebate at an illustrative 18 percent, the tax adjusted is ₹5,400 and the total credit note is ₹35,400. Settled as a financial credit note, no GST is calculated at all.

Is there tax on chargebacks?

A chargeback is a deduction, not a supply, so it carries no GST of its own. The tax effect depends entirely on the credit note that resolves it. If the manufacturer issues a tax credit note under Section 34, GST adjusts; if a financial credit note, it does not. The distributor debit memo alone changes nothing for GST.

Is GST applicable on a chargeback?

Not on the chargeback itself. A chargeback records that a distributor has short-paid or debited the manufacturer for a claim; it is an accounts step, not a taxable event. GST moves only when the manufacturer issues a credit note to settle the claim, and only if that note is a tax credit note under Section 34.

How are billbacks taxed in India?

A billback is a claim for a rate difference the manufacturer agreed to fund, and it settles as a credit note. The same choice applies: a tax credit note under Section 34 adjusts GST and requires the recipient to reverse proportionate ITC; a financial credit note leaves GST and ITC untouched. The label billback does not fix the treatment.

Is GST applicable on buyback of goods?

A genuine sales return is handled through a credit note under Section 34 by the original supplier, reversing the original GST. If bought-back stock is later destroyed or written off, the supplier must reverse input tax credit under Section 17(5)(h) of the CGST Act. So buyback GST depends on whether the goods return to trade or are scrapped.

Is TDS applicable on rebates and incentives?

Yes, potentially under Section 194R of the Income-tax Act. Where a business provides a benefit or perquisite — free goods, trips, gifts — arising from a business relationship, TDS at 10 percent applies once the value crosses ₹20,000 in aggregate for the recipient in a financial year. Cash incentives may fall under other TDS provisions instead.

What is the tax treatment of MDF?

It depends on characterisation, and this is genuinely fact-specific. Marketing development funds can be treated as a discount the manufacturer passes through a credit note, or as a service the dealer supplies — advertising, display, promotion — invoiced with GST to the manufacturer. The two routes have very different GST outcomes. Confirm the correct position with your CA.

Does a financial credit note attract GST?

No. A financial or commercial credit note is an accounting settlement that does not reduce the original transaction value, so it carries no GST and adjusts no output tax. Because the supplier's tax is unchanged, the recipient reverses no input tax credit. This is why financial credit notes are the simpler route for discretionary scheme settlements.

Who pays the tax on a scheme settlement — manufacturer or distributor?

It depends on the instrument and document. On a tax credit note, the manufacturer reduces its output GST and the distributor reverses proportionate input tax credit, so the adjustment lands on both sides. On a benefit-in-kind, the manufacturer bears TDS under Section 194R. On a financial credit note, neither side has a GST movement.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

GST Adjustments for Channel Settlements in India

Which document corrects what — credit notes, debit notes, e-invoice cancellation and GSTR-1 amendments for rebates, claims, returns and schemes.

Credit Notes for Expired and Damaged Goods Returns (Pharma and FMCG)

Expiry and damage returns under GST for pharma and FMCG — the two Circular 72/46/2018 routes, credit notes, ITC reversal, e-way bills and documentation.

GST Credit Notes for Trade Schemes: Issuance, Time Limits and GSTR Reporting

The 30 November time limit under Section 34(2), GSTR-1 Table 9B and 3B reporting, e-invoicing of credit notes, IMS and retention — for scheme teams.