GST Adjustments for Channel Settlements in India

Which document corrects what — credit notes, debit notes, e-invoice cancellation and GSTR-1 amendments for rebates, claims, returns and schemes.

In GST you cannot edit a document once it has been reported — you correct it. Which correction route applies depends on what changed and when you caught it: cancel the e-invoice while the window is still open, issue a credit or debit note against it after the window, or amend the figure through the return. For a channel finance team settling a rebate, claim, return or price adjustment, the choice is not cosmetic. Pick the wrong instrument and you hand your distributor an input-tax-credit mismatch to chase — and yourself an audit finding.

This guide is not another e-invoice walkthrough. It is the correction map for the moment you have already settled a channel event — a rebate paid, a scheme claim cleared, stock returned, a price protected — and you have to choose the document that makes the GST paperwork agree with what actually happened. It describes the mechanics and their consequences, not portal steps. The operational side of a reversal — the claim record, the approval and the audit trail behind the document — is covered in returns, reversals and cancellations in channel claims.

Which correction goes with which channel scenario?

Start from what changed, then from when you noticed it — those two facts pick the route. The table below maps the common channel settlements to a correction route, the document it produces, the effect on your channel partner's ITC, and where it shows up in the returns. Every row is a pointer; the deep mechanics live in the linked articles.

| Channel scenario — what changed | Correction route | Document | Effect on recipient's ITC | Where it is reported |

|---|---|---|---|---|

| Post-sale discount or rebate settled (tax by instrument) | Value falls after supply; tax adjusts only if the discount met Section 15(3)(b) conditions | Section 34 tax credit note if it qualifies; otherwise financial credit note (Circular 251 position) | Reverse proportionate ITC on a tax credit note; no reversal on a financial one | Tax CN in GSTR-1; flows to recipient's GSTR-2B |

| Scheme claim settled (particulars a credit note must carry) | Same value-fell logic; hinges on pre-agreed conditions and invoice linkage | Tax or financial credit note per the scheme terms | Reverse on tax CN; reconcile against GSTR-2B | Tax CN in GSTR-1; commercial CN off-portal |

| Goods returned, saleable | Value of the original supply is reversed for the returned quantity | Section 34 credit note (goods move on a delivery challan) | Recipient reverses ITC on the returned goods | GSTR-1; recipient's GSTR-2B |

| Goods expired or destroyed (expiry and damage routes) | Return or destroy; ITC on destroyed stock reverses under Section 17(5)(h) | Credit note (tax or commercial, by timing) | Reverse under Section 17(5)(h) on destruction | GSTR-1 for the CN; reversal in GSTR-3B |

| Price reduced after supply — price protection (rate-difference credit notes) | Taxable value drops for stock already billed | Section 34 credit note if conditions met; else financial | Reverse proportionate ITC on a tax CN | GSTR-1; recipient's GSTR-2B |

| Price increased after supply | Taxable value rises; more tax is due | Section 34 debit note | Recipient may claim the extra ITC | GSTR-1; recipient's GSTR-2B |

| Quantity or rate error on the original invoice | Original figure was wrong — over or under | Credit note if overcharged; debit note if undercharged | Reverse (CN) or claim more (DN) | GSTR-1; recipient's GSTR-2B |

| Wrong GSTIN on the invoice | Recipient identity was reported incorrectly | Amendment, not a credit or debit note | Recipient sees the corrected document in GSTR-2B | GSTR-1 amendment tables |

| Wrong tax rate applied | Tax charged too high or too low | Credit note (rate too high) or debit note (rate too low) | Reverse or claim the tax difference | GSTR-1; recipient's GSTR-2B |

| Claim settled but never invoiced | No original document to correct | Fresh invoice, or a debit note only against an existing invoice | Recipient claims ITC on the new document | GSTR-1; recipient's GSTR-2B |

Two things read straight off the table. First, a credit note and a debit note are not interchangeable — the direction of the change decides which one you raise. Second, whether the correcting document carries tax at all is a separate question from which document you use. The next two sections take those in turn.

Credit note or debit note? The direction rule

Issue a credit note when the taxable value or tax charged was more than it should be, or when goods came back; issue a debit note when it was less. That single rule settles most channel corrections, and it holds regardless of who feels aggrieved. Both documents must reference the original invoice — a credit or debit note that floats free of the supply it corrects is not doing its GST job.

The correcting document — and whether it carries tax — follows what changed and whether the discount met the agreed conditions.

Read it from both sides of the settlement. The supplier issues the note; the recipient receives it. On a credit note, the supplier reduces its output tax (if the note carries tax) and the distributor must reverse the matching input tax credit. On a debit note, the supplier adds output tax and the distributor gets to claim the extra credit. The document is one piece of paper, but it moves two ledgers in opposite directions — which is exactly why a mismatch here surfaces as a reconciliation break weeks later.

A worked mini-example makes the symmetry concrete. Take an original channel invoice of ₹1,00,000 taxable plus ₹18,000 GST (an 18% rate used purely for illustration). Credit-note way: you agree a post-supply reduction of ₹10,000 that qualifies for a tax adjustment. You raise a credit note for ₹10,000 taxable and ₹1,800 GST; your output tax falls by ₹1,800, and the distributor reverses ₹1,800 of ITC. Debit-note way: you later find the same invoice undercharged by ₹10,000. You raise a debit note for ₹10,000 plus ₹1,800; your output tax rises by ₹1,800, and the distributor claims ₹1,800 more ITC. Same amounts, opposite direction — the conceptual difference between a credit memo and a debit memo is the whole game, and the mechanics of a credit note sit behind it.

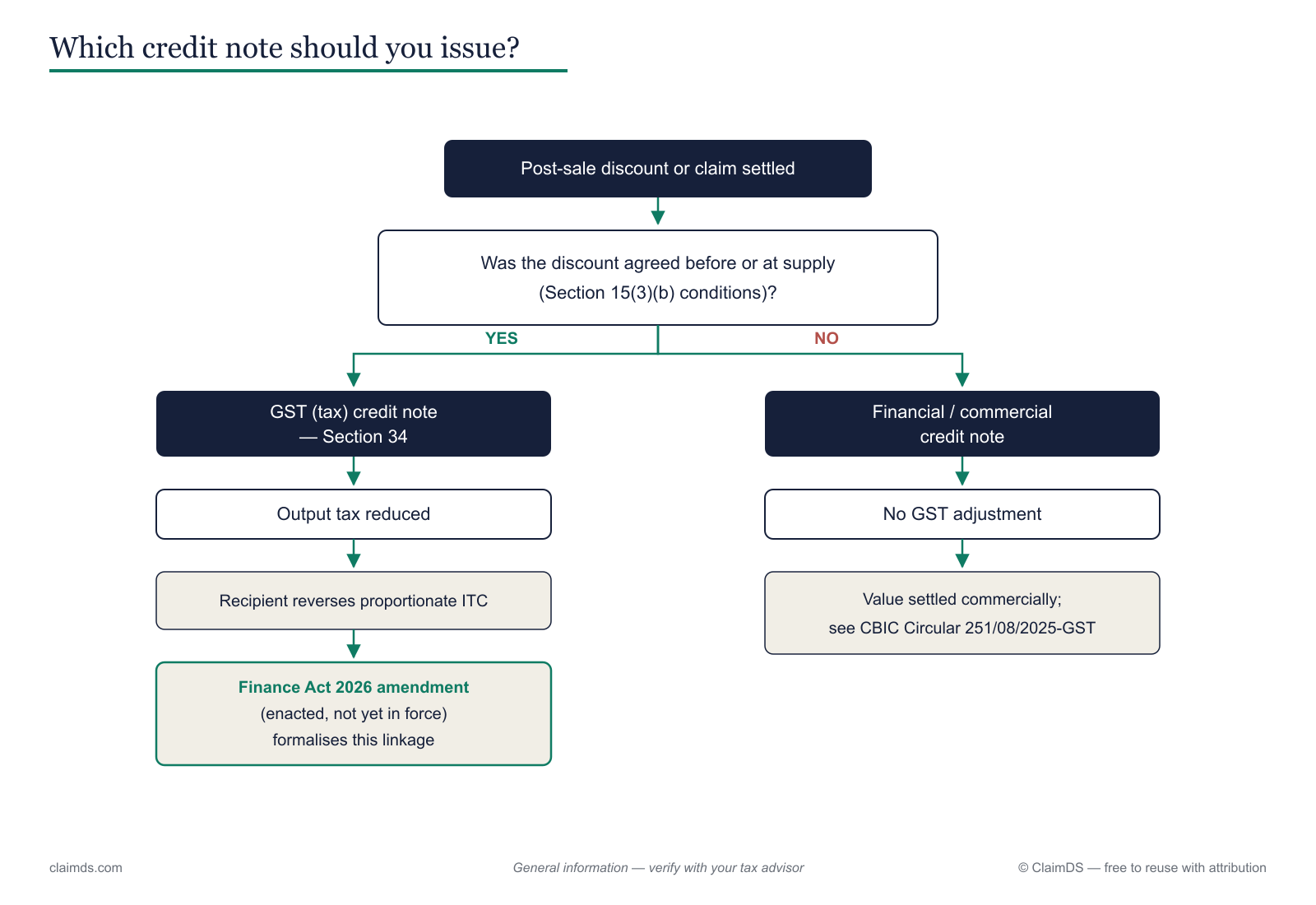

GST credit note vs financial or commercial credit note

Not every credit note carries tax — and choosing the wrong kind is the most expensive correction mistake in channel settlement. A Section 34 tax credit note reduces the supplier's output tax and obliges the recipient to reverse proportionate ITC. A financial or commercial credit note settles money only: no output-tax reduction, no ITC reversal, and no entry in the GST returns. The two look almost identical on the page and behave completely differently in the ledger.

The decision is not aesthetic. A post-sale discount carries tax only if it met the pre-agreed, invoice-linked conditions of Section 15(3)(b); a discount that fails those conditions cannot be dressed up as a tax credit note just because the parties would prefer the output-tax relief. The full framework — which discounts qualify, and what the recipient must do about ITC — is set out in financial vs. tax credit notes under GST, and the current CBIC position on commercial credit notes and ITC is in Circular 251 and post-sale discounts. The corresponding reversal duty on the recipient's side is covered in ITC reversal on post-sale discounts and credit notes.

For the correction decision, hold on to one test: did the value genuinely change under conditions GST recognises, or are you simply moving money between two accounts? If it is the former and the timing window is open, a tax credit note is the instrument. If it is the latter — or the window has closed — a financial credit note is the honest document, and it leaves both parties' GST positions untouched. This article stops at that fork; the linked pieces walk each branch in full.

E-invoice: cancellation, and why it cannot be modified

An e-invoice, once its IRN is generated, cannot be edited — the correction is either a cancellation inside the window or a credit or debit note after it. For channel finance this is the crux, because your distributor's ITC is built from what you report. Get the instrument wrong here and the mismatch propagates straight into their GSTR-2B. State each mechanic conservatively and verify it before you rely on it.

- An IRN cannot be edited once generated. There is no "edit invoice" action on the IRP. If the value, rate or party on a channel invoice is wrong, the reported document stays as it is until you either cancel it or correct it with another document. This is the single fact that makes everything else in this section follow.

- Cancellation is permitted only within a short window after IRN generation — commonly stated as 24 hours. <!-- TODO VERIFY AT PUBLISH: 24-hour IRP cancellation window --> Inside that window you can cancel the e-invoice on the IRP and, if needed, issue a fresh one. This is the cleanest correction when you catch the error immediately after settling a claim.

- Partial cancellation is not possible. You cannot cancel a single line or a single amount — an IRN is cancelled in full or left standing. A one-line error on a multi-line channel invoice therefore means either a full cancel-and-reissue inside the window, or a targeted credit or debit note after it.

- A cancelled invoice number cannot be reused. Once a number has been attached to an IRN that is then cancelled, the series moves on; your next document takes a new number. Settlement records must point to the number that actually carries the tax.

- An active e-way bill blocks cancellation until it is addressed. If an e-way bill is live against the IRN, cancellation is not available until that is resolved. <!-- TODO VERIFY AT PUBLISH --> For channel movements this is routine: the goods leg and the invoice leg have to be unwound together, not independently.

- After the window, the route is a credit or debit note — and, where a wholly different document is warranted (for example a genuinely new supply), a fresh invoice with a new number. The e-invoice you cannot cancel is not deleted; it is corrected by the adjusting document that references it.

- Reported details are amended in the GSTR-1 amendment tables, not on the IRP. Corrections to what was reported flow through the return's amendment tables, subject to an outer time limit; the IRP is not an amendment tool. <!-- TODO VERIFY AT PUBLISH: current GSTR-1 amendment tables and outer time limit -->

Frame each of these in the channel context. When you cancel and reissue inside the window, your distributor simply sees the corrected e-invoice. When you miss the window and correct with a credit or debit note, their GSTR-2B moves by the note, and their ITC has to follow it. When you amend in GSTR-1, the corrected figure reaches them through the amendment tables. The distributor's credit position is always downstream of the instrument you pick.

What is the time limit for correcting a settlement with a credit note?

A tax credit note against a supply has an outer reporting limit — and once it passes, the tax can no longer be adjusted. The general rule is that a credit note carrying a GST adjustment must be reported within a window commonly tied to the November following the end of the financial year of supply, or the date of filing the annual return, whichever is earlier. State it as the general rule and confirm the exact cut-off before acting. <!-- TODO VERIFY AT PUBLISH: current credit-note outer time limit -->

The practical consequence for channel settlement is blunt. If a rebate, claim or price adjustment is finalised after that window has closed, you can still pay the distributor — but not through a document that moves GST. The settlement typically shifts to a financial or commercial credit note with no tax adjustment: the money changes hands, the output tax and the distributor's ITC do not. That keeps you compliant instead of forcing a tax reduction the law no longer permits. The full timing detail and the reporting mechanics are in GST credit-note time limits and reporting, and the choice between a tax and a commercial instrument is the same fork covered in financial vs. tax credit notes under GST. The discipline is to watch the clock at settlement time, not at year-end, so the window decision is made while a tax credit note is still an option.

What happens when the supplier never files the credit note?

A credit note on paper that never reaches GSTR-2B leaves the distributor with books and ITC that disagree — and no clean way to close the claim. This is the distributor's version of the pain. You settled the claim, you hold the supplier's credit note, and your ledger reflects it. But if the supplier has not reported that credit note, it does not appear in your GSTR-2B, so the input-tax-credit position the portal shows and the position your books show have drifted apart.

What the recipient can actually do is bounded but real. Reconcile first: match every credit note you hold against what GSTR-2B carries, by document number, date and GSTIN, so you know precisely which notes are missing rather than assuming a blanket gap. Follow up with the supplier to get the note reported. And hold the reversal decision on the disputed items until the position is resolved — reversing against a note the portal has not yet recognised only manufactures a second mismatch. The reconciliation mechanics are in reconciling scheme credit notes across GSTR-2B and 3B, and the reversal duties that sit behind them — including the 180-day payment condition under Rule 37 and the wider reversal triggers on post-sale discounts — decide what actually has to move once a note is confirmed.

The structural lesson is why settlement records must tie each claim to its document number. When every reversal, credit note and claim carries the same reference, a GSTR-2B gap is a two-minute lookup, not a quarter-end investigation. The workflow for that linkage is in reconciling a claim to a credit note.

Both sides of the ledger — what each party does, and must not do

Every correction instrument has a supplier-side action and a recipient-side action, and the mistakes cluster where one side assumes the other has acted. The consolidated view:

| Instrument | Manufacturer / supplier issues | Distributor / dealer receives |

|---|---|---|

| GST (Section 34) credit note | Reduce output tax; report in GSTR-1 within the window; reference the original invoice. Must NOT use it for a discount that fails the Section 15(3)(b) conditions. | Reverse proportionate ITC once it appears in GSTR-2B. Must NOT keep the full ITC after a tax credit note lands. |

| Financial / commercial credit note | Settle money only; no GST; keep it off the return. Must NOT reduce output tax on it or report it as a tax CN. | Book the commercial credit; do NOT reverse ITC and do NOT expect it in GSTR-2B. |

| Debit note | Add output tax; report in GSTR-1; reference the original invoice. Must NOT use it to raise value on a supply it cannot tie to an invoice. | Claim the additional ITC once it appears in GSTR-2B. Must NOT claim before the note is reported. |

| Cancelled e-invoice | Cancel only within the window and in full; resolve any active e-way bill first; do NOT reuse the cancelled number. Must NOT attempt a partial cancel. | Rely on the reissued e-invoice; do NOT claim ITC on the cancelled number. |

| GSTR-1 amendment | Correct reported details through the amendment tables within the outer limit. Must NOT treat the IRP as an amendment tool. | Pick up the corrected figure from GSTR-2B; do NOT act on the pre-amendment version once superseded. |

The pattern across every row is symmetry: what the supplier reports, the recipient must mirror, and neither side should move ahead of the document. The ITC reversal lifecycle walks the recipient side end to end.

Making corrections auditable

A correction you cannot trace back to its instrument is a correction you cannot defend. Every claim reversal should carry the document type and number it was corrected with — tax credit note, financial credit note, debit note, cancelled-and-reissued e-invoice, or GSTR-1 amendment — so that months later the settlement, the ledger and the return all point at the same reference. That is the difference between a two-minute reconciliation and a quarter-end scramble. A claims platform like ClaimDS is designed to tie each claim to its correcting document and keep that linkage auditable across the settlement. <!-- TODO: confirm capability wording with founder --> The reconciliation workflow behind it is in reconciling a claim to a credit note.

Disclaimer: This article is general information, not tax or legal advice. It references Section 34, Section 15(3)(b), Rule 37 and Section 17(5)(h) of the CGST framework, the GSTR-1 amendment tables, GSTR-2B and GSTR-3B, the IRN/IRP and e-way bill mechanics, CBIC Circular 251/08/2025-GST, and the Finance Act 2026 (enacted but not yet notified as of the date above). Numeric mechanics — cancellation windows and credit-note time limits — must be verified against current provisions before you act. Consult a qualified professional for your specific facts. <!-- TODO: CA/CMA reviewer name and credential before publish — THIS ARTICLE MUST NOT PUBLISH WITHOUT REVIEW -->

Getting the correcting document right the first time is cheaper than reconciling a mismatch later — and far cheaper than defending one in an audit. If your channel team settles rebates, claims, returns and price adjustments across many partners, the instrument-selection and document-linkage discipline in this guide is exactly what ClaimDS builds into the settlement flow. When a settled rebate has to be recovered rather than corrected, that shifts into rebate clawbacks and scheme cancellations — the recovery routes and the tax questions they raise.

Frequently asked questions

Can an e-invoice be modified?

No. Once an IRN is generated the reported invoice cannot be edited on the IRP. To correct a channel settlement you either cancel the e-invoice inside the permitted window and issue afresh, or leave it standing and issue a credit or debit note against it. Reported details are amended only through the GSTR-1 amendment tables. Verify current rules before acting.

How do you cancel an e-invoice?

Cancellation happens on the IRP, not by deleting anything in your books, and only within the allowed window after IRN generation. The whole document is cancelled — you cannot strike out one line. If an e-way bill is active against that IRN, resolve it first. After the window, a credit or debit note is the route. Verify the current window at publish.

What if 24 hours have passed since the e-invoice?

Then IRP cancellation is generally no longer available, so the e-invoice stands as reported. You correct the channel settlement with a credit note (if value or tax was too high, or goods came back) or a debit note (if too low), always referencing the original invoice. Where a fresh invoice is warranted, it carries a new number. Verify the window before relying on it.

Can an e-invoice be partially cancelled?

No. Partial cancellation is not possible — an IRN is cancelled in full or not at all. If only one line or amount on a channel invoice is wrong, cancelling and reissuing the whole document may be cleaner inside the window; outside it, a credit or debit note adjusts the specific difference without disturbing the rest of the invoice. Verify current mechanics.

Can a cancelled invoice number be reused?

No. Once an invoice number is used for an IRN that is then cancelled, that number cannot be reused for a fresh e-invoice. Your next document takes a new number in the series. For channel teams this matters because settlement records must point to the number that actually carries the tax, not the abandoned one. Verify current portal behaviour before relying on it.

When do you issue a credit note vs a debit note?

Issue a credit note when the taxable value or tax originally charged was more than it should be, or when goods are returned — it reduces what the recipient can claim. Issue a debit note when the value or tax was too low and more is due. Both must reference the original invoice. The direction follows what changed, not who is unhappy.

Can a GST credit note be cancelled?

A credit note reported under Section 34 is corrected the same way any reported document is — you do not quietly delete it. If it was wrong, the usual route is a further adjusting document and an amendment in the GSTR-1 amendment tables, subject to the outer time limit. Treat a raised credit note as part of the audit trail. Verify current amendment mechanics.

What is the time limit for a GST credit note?

A credit note carrying a tax adjustment against a supply must be reported within an outer limit generally tied to the November following the financial-year end, or the annual-return filing, whichever is earlier. Miss it and the tax cannot be adjusted, so the settlement usually moves to a financial credit note with no GST effect. Verify the current limit before acting.

What do you do if the supplier's credit note is not in GSTR-2B?

First reconcile: confirm the document number, date and GSTIN, then follow up with the supplier, because a credit note on paper but absent from GSTR-2B means your ITC and books disagree. Hold the reversal decision until it is resolved, and keep the claim tied to its document number. This is a reconciliation and evidence problem, not a reason to guess. Verify treatment with your advisor.

Which credit note should be used to settle a rebate?

It depends on whether the discount met the agreed pre-supply conditions. Where a rebate qualifies under Section 15(3)(b) and the supplier wants to reduce output tax, a Section 34 tax credit note fits, with the recipient reversing proportionate ITC. Where it does not qualify, or the window has closed, a financial credit note settles the money with no tax movement. Verify the position.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Tax on Rebates, Chargebacks, Billbacks and Buybacks in India

How each channel settlement is taxed in India — rebates, chargebacks, billbacks, buybacks and MDF — GST and TDS for both payer and receiver.

Credit Notes for Expired and Damaged Goods Returns (Pharma and FMCG)

Expiry and damage returns under GST for pharma and FMCG — the two Circular 72/46/2018 routes, credit notes, ITC reversal, e-way bills and documentation.

GST Credit Notes for Trade Schemes: Issuance, Time Limits and GSTR Reporting

The 30 November time limit under Section 34(2), GSTR-1 Table 9B and 3B reporting, e-invoicing of credit notes, IMS and retention — for scheme teams.