Deduction Management: Challenges, Best Practices and the AR Deductions Process

The AR deductions process — 6-stage lifecycle, the 7 biggest deduction management challenges, invalid-deduction recovery and a best-practice checklist.

When a distributor or retail chain pays less than the invoice — citing a scheme claim, a sales return, damaged stock or a pricing difference — the gap is a deduction, and someone in your AR team now owns a small investigation. The visible cost is the leakage; the larger, quieter cost is the hours spent reconstructing what happened, weeks or months after the fact. Our pillar guide to deduction management for accounts-receivable teams covers what accounts receivable deductions are and why they arise: amounts customers net from payments that must each be matched to a valid claim, with the invalid ones disputed and recovered. This article goes deeper into the process itself — the lifecycle, the challenges, and deduction management best practices for Indian manufacturers selling through distributors and retail chains.

The deduction process in accounts receivable: a 6-stage lifecycle

Handling deductions in accounts receivable is not one task but a repeatable lifecycle. Most teams do stages one and four and improvise the rest — which is exactly where the leakage hides. The deduction process in accounts receivable runs through six stages.

Stage 1 — Identification. A deduction announces itself as a short-payment on the remittance advice: the customer pays ₹9,35,000 against a ₹10,00,000 invoice and the bank statement, remittance email or payment advice explains — or fails to explain — the ₹65,000. Identification means catching every such gap at the point of cash application, not during a quarter-end reconciliation. If your cash-application process posts partial payments without flagging the shortfall as a distinct, trackable item, deductions are invisible from day one.

Stage 2 — Capture and coding. Each identified deduction gets logged as its own record with a standard reason code: scheme claim, return, damage, rate difference, shortage, promotional allowance, unidentified. Coding is the single highest-leverage step in ar deductions management — an uncoded deduction cannot be routed, aged, analysed or recovered. One remittance often carries several deductions with different reasons; capture them as separate coded lines, not one lump.

Stage 3 — Research and validation. Now each coded deduction is checked against the source of truth for its reason: the scheme circular and its validity window, the claim the customer submitted, proof-of-delivery documents for shortage or damage, and the operative price list for rate differences. This is where a deduction meets the claim lifecycle — a short-payment citing a scheme should correspond to a claim that is somewhere between Submitted, Validated, Approved and Settled. If the referenced claim was validated and approved, the deduction is likely good; if no such claim exists, or it was rejected, you have a problem worth pursuing. Validation math follows the same discipline as calculating FMCG distributor claims — slab, base value, window — applied to whichever of the scheme types the customer cites.

Stage 4 — Resolution. Every researched deduction ends in one of three states: approved (the deduction was valid — issue the matching credit note and close the claim), disputed (the deduction fails validation — raise it formally with the customer), or recover (the customer accepts it was invalid — collect or offset). Resolution should be an explicit recorded decision with an owner and a date, never a silent reconciliation adjustment.

Stage 5 — Recovery of invalid deductions. Disputed deductions that the research sustains become recovery cases: a debit note or dispute letter with evidence attached, a response window, escalation through the sales relationship if ignored, and settlement by collection or offset against the customer's next payable credit note. Recovery is a clock — the longer an invalid deduction sits, the closer it drifts to an unplanned write-off.

Stage 6 — Root cause and write-off policy. The lifecycle closes with two disciplines. First, root-cause analysis: why did this deduction happen, and is it a pattern — a scheme communicated ambiguously, a price list not synced to the customer, a recurring damage lane? Second, a written write-off policy: below what value, and after what recovery effort, may a deduction be written off, approved by whom. Without a documented policy, write-offs become the default resolution for anything inconvenient.

Two numbers tell you whether this lifecycle is working. The first is the coding rate — the share of short-payments carrying a real reason code within a week of landing; anything sitting as "unidentified" beyond that is stage two failing. The second is days-deduction-outstanding, the ageing measure introduced in the pillar guide: how long deductions sit between identification and resolution. When DDO rises, stages three to five are the bottleneck, and every additional week of age converts a little more recoverable money into write-off.

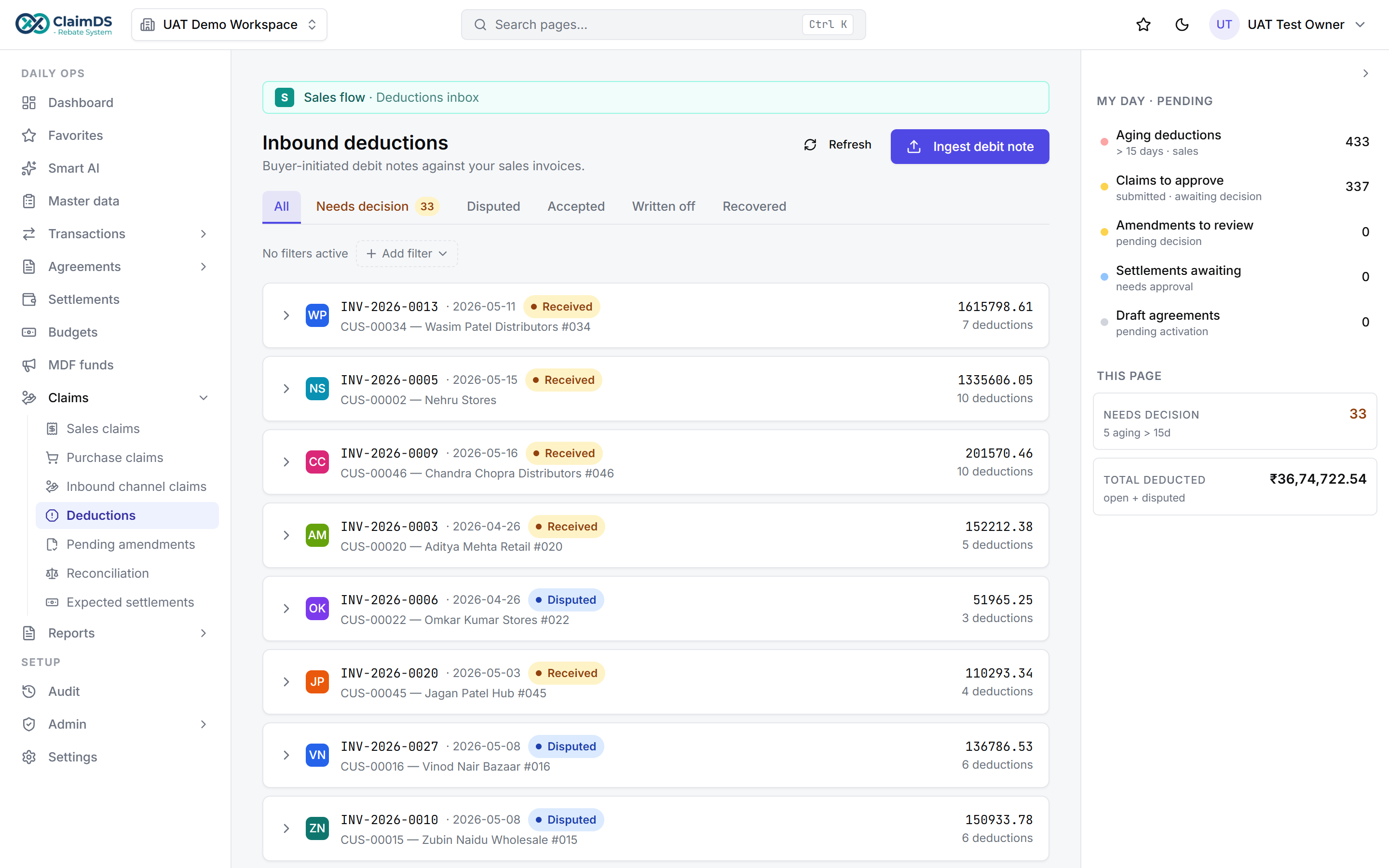

Here is that inbox in practice — customer deductions captured, coded and tracked against their originating claims:

The 7 biggest deduction management challenges

Ask any AR manager running ar customer deductions by hand and the same failure modes come up. These are the seven deduction management challenges that do the most damage, each with the operational fix.

1. No reason codes — the suspense bucket

Short-payments get posted against the account as "on account" or parked in a suspense ledger with no reason attached. Six months later nobody can say whether ₹18 lakh of accumulated suspense is valid scheme settlement or pure leakage — and researching it now means archaeology. The bucket also flatters your books: it looks like receivables, but much of it will never be collected. Fix: a mandatory, standard reason-code list applied at capture — including an explicit "unidentified" code that is itself tracked and aged, so unknowns are a visible queue rather than an invisible pile.

2. Evidence scattered across email, WhatsApp and the ERP

The scheme circular is a PDF in someone's inbox, the damage photos are on a sales officer's WhatsApp, the claim is in a spreadsheet and the invoice is in the ERP. Validating one deduction means assembling a jigsaw across four systems and three people — the defining trait of manual claim and rebate processing. When the sales officer changes territory, the evidence leaves with them. Fix: a single system of record where scheme, claim, evidence and deduction live together — with the ERP integrated so invoices and payments flow in rather than being re-keyed.

3. Small-value auto-write-offs below the radar

Most teams set a tolerance — say, write off anything under ₹2,000 without research. Sensible in isolation; dangerous unmonitored. Customers learn the threshold, deductions cluster just below it, and a thousand small write-offs a year quietly become a material number that no one ever approved as a policy decision. This is revenue leakage in its most respectable disguise. Fix: keep the threshold, but report the aggregate written off per customer per quarter — and review the threshold itself quarterly. A customer whose sub-threshold deductions triple deserves research regardless of individual value.

4. Scheme-vs-deduction mismatch — netting off unapproved claims

The customer submits a scheme claim, does not wait for validation, and simply nets the amount off their next payment. Now the same rupees exist twice in your process: once as a claim awaiting approval, once as a deduction already taken. If the two are not linked, you risk settling twice — approving the claim with a credit note while the deduction also stands. Fix: match every scheme-coded deduction to its originating claim before resolution, and make "deduction taken against unapproved claim" an explicit exception status that pauses the credit note until the two are reconciled.

5. Ageing — researching months later when proof is gone

A deduction researched in week one is a lookup; the same deduction researched in month six is a dispute you will probably lose. Scheme windows have closed, the POD is untraceable, the sales officer who knew the context has moved on, and the customer's own records have hardened. Ageing converts recoverable money into write-offs by pure passage of time. Fix: an ageing dashboard for deductions — the same discipline you apply to receivables — with a same-week coding SLA and a research SLA measured in days, not quarters.

6. No ownership split between sales, finance and claims

Finance says sales agreed to the scheme; sales says finance owns collections; the claims team says the deduction is not a claim. The deduction sits in the gap between three functions, owned by none. Disputes and deductions management fails most often not on analysis but on accountability. Fix: an explicit ownership matrix — finance owns identification, coding and the ledger; the claims team owns validation against schemes; sales owns customer-facing dispute conversations and recovery escalation. One named owner per deduction, visible in the system.

7. No root-cause loop — the same deduction repeats

The team resolves each deduction as a one-off and never asks why the same customer takes the same rate-difference deduction every month. Without a feedback loop, deduction volume grows with sales volume forever, and the AR team scales headcount instead of shrinking the problem. Fix: a monthly root-cause review — deductions by reason code and customer, trended — with sales in the room, and one corrective action per recurring pattern: fix the price-list sync, clarify the circular, or confront the customer's behaviour directly.

Invalid deductions and recovery

An invalid deduction is a short-payment with no legitimate basis. In an Indian channel context the common species are:

- Duplicate netting — the customer deducts for a claim that was already settled by credit note, or takes the same deduction on two remittances.

- Expired scheme window — the scheme is real, but the purchases cited fall outside its validity period or the claim was submitted after the cut-off.

- Quantity inflation — damage or shortage deducted for more units than the POD or the return record supports.

- Unsupported pricing — a rate difference deducted against a price the operative price list never contained, or a discount that was proposed but never approved.

A worked example makes the triage concrete. The figures are illustrative:

| Item | Detail | Amount |

|---|---|---|

| Invoice value | Invoice to distributor | ₹10,00,000 |

| Remittance received | Paid per remittance advice | ₹9,35,000 |

| Total deducted | Coded as three separate deductions | ₹65,000 |

| Deduction 1 — scheme claim | Matches an approved quantity-discount claim, in window | ₹40,000 — validated, credit note issued |

| Deduction 2 — damage claim | Same damage already settled by credit note last month (duplicate netting) | ₹15,000 — invalid, debit note raised, recovered |

| Deduction 3 — rate difference | Cited rate not on the operative price list; sales confirms no approval | ₹10,000 — disputed, under review with the customer |

The dispute and debit-note step is a checklist, not a template:

- State the deduction reference, invoice number, remittance date and amount.

- State the specific reason the deduction fails — duplicate, out of window, quantity unsupported, price unsupported — with the evidence attached (credit-note reference, scheme circular dates, POD, price list).

- Raise the debit note or formal dispute in your books so the amount is a tracked receivable, not a memo.

- Give a defined response window and a named contact on both sides.

- Escalate through the sales relationship on breach — the pattern mirrors the chargeback dispute process.

- Close by collection, offset against the next payable credit note, or an approved write-off under policy — never by silence.

Deduction management best practices

Ten habits separate teams that control accounts receivable deductions management from teams that absorb it. Use this as an audit checklist:

- Standard reason codes, mandatory at capture. A fixed list everyone uses, including "unidentified" as a tracked code — because an uncoded deduction cannot be managed at all.

- Same-week coding SLA. Every short-payment identified and coded within the week it lands; coding lag is the root of ageing.

- Evidence capture at claim intake. Collect the circular reference, proofs and documents when the claim is born — the standard is the scheme settlement documentation playbook — so deduction research is a lookup, not a hunt.

- An approval matrix with segregation of duties. Who may approve a deduction at what value, with the researcher never being the approver — the same design as claim and rebate approval workflows.

- Quarterly materiality-threshold review. Keep the small-value write-off tolerance, but review the level and the per-customer aggregates every quarter.

- An ageing dashboard. Deductions by age band, reason and customer, reviewed weekly — rising age in any band is the earliest recoverable warning.

- Scheme-claim-deduction matching before any write-off. Never write off a scheme-coded deduction without confirming whether an approved claim exists — it may simply be settlement taken early.

- Monthly root-cause review with sales. Trend deductions by reason and customer; assign one corrective action per recurring pattern.

- Named recovery ownership. Every disputed deduction has one owner and a next-action date until it is collected, offset or written off under policy.

- An audit trail on every resolution. Who validated, who approved, what evidence supported it — recorded in the system, because deduction resolutions are exactly what auditors and large customers ask about later.

None of these require software to start — a disciplined team can run reason codes, SLAs and the monthly review from tomorrow morning. What software changes is enforcement at volume: codes become mandatory fields instead of habits, SLAs escalate on their own, and the matching in item seven happens automatically instead of depending on whoever remembers the claim. Run the ten as a quarterly self-audit; the items you fail consistently are the ones that justify tooling.

The India angle: deductions, claims and credit notes

In an Indian channel business, ar deductions rarely arrive as abstract disputes — they arrive as short-payments against scheme claims that are still awaiting settlement. The distributor has run the secondary scheme, submitted the claim, and rather than wait for your credit note, nets the amount off the next payment. That makes deduction resolution inseparable from GST settlement mechanics: closing a valid deduction means issuing the right instrument — a financial credit note or a GST credit note with tax adjustment — and the choice carries consequences for both sides. The decision framework is in financial vs tax credit notes under GST, and the buyer-side effect — whether the distributor must reverse input tax credit — is covered in ITC reversal on post-sale discounts. Resolution is not truly closed until the credit note also reconciles in the customer's returns, the discipline described in reconciling scheme credit notes with GSTR-2B and GSTR-3B. A deduction resolved with the wrong instrument type is not resolved — it is a future reconciliation dispute with tax attached.

GST note: The GST references above are general information, not tax or legal advice — verify current positions with a qualified professional before acting.

Retail chargebacks vs deductions

The terms travel together but are not synonyms. A deduction is the customer-initiated act of short-paying an invoice, whatever the reason. A chargeback is one specific reason — a retailer or channel partner charging a cost back to you, such as a compliance penalty, a promotional charge or a margin support amount; it may be taken as a deduction at payment or billed separately, in which case it behaves like a billback. The full disambiguation is in the billbacks vs chargebacks vs deductions glossary, and the operational hub for handling chargebacks specifically is chargeback management software. In short: every chargeback taken at payment is a deduction; most deductions in an FMCG or pharma channel are scheme claims, not chargebacks.

Deduction management, done in minutes instead of months

Every stage above gets harder when the deduction, the claim and the scheme live in different systems. ClaimDS ties every deduction to its originating claim and scheme on one ledger — so validation is a lookup against the claim's own lifecycle (Submitted → Validated → Approved → Settled), duplicate netting is visible the moment it happens, and the resolution issues the correct credit-note type with the audit trail already attached. That is the difference between researching a short-payment in minutes and reconstructing it months later. For where deduction handling sits in the wider settlement stack, start with the claims management software hub and the rebate management software guide.

Frequently asked questions

What is deduction management?

Deduction management is the accounts-receivable process of handling amounts customers pay short of invoice value — identifying each short-payment, coding its reason, validating it against schemes and claims, resolving it as approved or disputed, recovering invalid amounts, and feeding root causes back so the same deduction does not repeat.

What are deductions in accounts receivable?

Deductions in accounts receivable are the gaps between invoice value and what the customer actually remits. Distributors and retail chains take them for scheme claims, returns, damaged stock, pricing differences or promotional allowances — sometimes validly, sometimes not, which is why each one must be coded and researched.

What is the deduction process in accounts receivable?

A six-stage lifecycle: identify the short-payment on the remittance, capture and code it with a reason, research and validate it against scheme circulars, claims, PODs and price lists, resolve it as approved or disputed, recover invalid amounts through debit notes or offsets, and run root-cause analysis with a written write-off policy.

What are the biggest deduction management challenges?

The recurring ones: uncoded deductions sitting in a suspense bucket, evidence scattered across email, WhatsApp and the ERP, small-value auto-write-offs that creep below materiality thresholds, customers netting off unapproved claims, deductions ageing until proof disappears, unclear ownership between sales and finance, and no root-cause loop so the same deduction repeats every cycle.

What are invalid deductions?

Invalid deductions are short-payments with no legitimate basis — a claim netted off twice, a scheme claimed outside its validity window, quantities inflated beyond what was sold or damaged, or pricing differences the price list does not support. They are recoverable, but only if researched and disputed before the evidence goes stale.

How do you recover invalid deductions?

Research the deduction against the scheme circular, claim record and proof documents; document why it fails; raise a debit note or formal dispute with the evidence attached; give the customer a defined response window; escalate through sales if unanswered; and either collect, offset against the next payable credit note, or write off with approval under a documented policy.

What is the difference between a deduction and a chargeback?

A deduction is the customer-initiated act of paying less than invoice value for any reason. A chargeback is one specific reason a deduction (or a billed claim) exists — typically a retailer or channel partner charging back a cost such as a compliance penalty or promotional charge. Every chargeback taken at payment shows up as a deduction; not every deduction is a chargeback.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

What is a Billback? Meaning, Process and How It Differs from a Chargeback

Billback meaning in plain English — how billbacks work, billback pricing, a worked example, and billback vs chargeback in Indian channels.

CPQ Software vs. Rebate and Claims Management: Which Do You Actually Need?

CPQ meaning, in one line: Configure-Price-Quote software for pre-sale quoting. Here is how it differs from post-sale rebate and claims management.

How Rebate Schemes Work for Online Sellers & E-Commerce Channels in India

How rebate and incentive schemes work for India's e-commerce channel — brands running schemes for marketplace/D2C sellers, and sellers reconciling rebates against platform deductions.