Primary, Secondary and Tertiary Sales: What They Mean and Why Your Claims Depend on Them

What primary, secondary and tertiary sales mean, where each tier's data lives, how to verify it, and why Indian trade claims settle on secondary data.

Every unit an Indian manufacturer sells moves through three distinct sales events: the manufacturer sells to a distributor (primary sales), the distributor sells to retailers (secondary sales), and the retailer sells to the consumer (tertiary sales). Three tiers, three sets of books, three very different levels of visibility. The catch that defines Indian channel finance: most trade schemes — secondary schemes, retailer incentives, damage and expiry claims — settle on secondary data the manufacturer does not natively possess. It sits in the distributor's systems, arrives as claims and reports, and has to be verified before money moves. This guide defines each tier, shows where the data lives, and explains why your claims process depends on getting the secondary tier right.

What is primary sales?

Primary sales are the manufacturer's sales to the first tier of the channel — distributors, super stockists or C&F-routed billing, depending on the route-to-market (the tier structure itself is covered in distributor vs dealer vs super stockist).

Primary is the easiest tier to measure, because it is recorded in the manufacturer's own invoicing and ERP. Every primary sale generates a tax invoice the manufacturer raised, a ledger entry the manufacturer controls, and a receivable the manufacturer tracks. There is no reporting dependency on anyone else: if you want last month's primary sales by SKU and distributor, your own systems answer the question.

That ease of measurement is exactly why primary sales carry a known distortion: channel loading. Because primary billing is what sales teams are most often targeted and measured on, stock gets pushed into the channel at period-end to hit numbers — whether or not retail demand exists to pull it through. The invoice is real; the demand may not be. A business that reads only its primary line can look healthy while the channel silently fills up (more on this in the channel loading section below).

What is secondary sales?

Secondary sales are the distributor's sales to the next tier down — retailers, dealers or sub-stockists. This is the tier where product actually moves toward the market rather than merely into a warehouse.

The defining feature of secondary sales is where the data lives: in the distributor's billing software or distributor management system, not in the manufacturer's ERP. The manufacturer never raises these invoices and has no native record of them. Whatever secondary visibility a manufacturer has is visibility the channel gave it — through reports, uploads, or system integrations.

Manufacturers care about secondary data for three reasons:

- True offtake. Secondary sales are the closest reliable proxy for real market demand. Primary tells you what you billed; secondary tells you what the channel actually sold onward.

- Scheme settlement basis. Most Indian trade schemes — display incentives, retailer slabs, secondary-driven distributor incentives — pay on secondary performance. No secondary data, no defensible settlement. (See secondary scheme settlement for how that settlement works end to end.)

- Stock-in-trade visibility. Primary minus secondary equals the stock sitting in distributor godowns. Watching that gap is how you spot over-stocking, ageing inventory and looming expiry or stock compensation exposure before it becomes a claim.

A closely related distinction — whether a rebate should pay on the buy-in tier or the sell-through tier, and what behaviour each choice incentivises — is the subject of sell-in vs sell-through rebates; this article stays on the definitions, the data and the claims that ride on it.

What is tertiary sales?

Tertiary sales are the retailer's sales to the end consumer — the last tier, and the only one that represents final consumption rather than movement between trade partners.

Tertiary is also the hardest tier to measure. In practice it is approximated rather than recorded:

- Retail audits — sampling stores to estimate offtake and market share for a category.

- Point-of-sale data in modern trade — organised retail chains can share till-level sell-out data, giving genuinely transactional tertiary visibility for that slice of the business.

- Loyalty and consumer-activation programs — scan-based or code-based consumer promotions generate a partial tertiary signal for participating purchases.

An honest note: in Indian general trade — the lakhs of independent kirana and counter stores that carry most FMCG volume — tertiary sales are largely estimated. The typical neighbourhood store does not run a POS system that reports to anyone. For most manufacturers, tertiary is a directional planning input, not a settlement-grade dataset — which is one reason schemes rarely settle on it, and why secondary remains the practical frontier for claims.

Primary vs secondary vs tertiary at a glance

| Primary sales | Secondary sales | Tertiary sales | |

|---|---|---|---|

| Who sells to whom | Manufacturer → distributor | Distributor → retailer | Retailer → consumer |

| Where recorded | Manufacturer's ERP / invoicing | Distributor's billing software / DMS | Retail POS (modern trade); estimated elsewhere |

| Who controls the data | Manufacturer | Distributor | Retailer (or nobody, in general trade) |

| Typical accuracy | High — first-party records | Medium — reported, needs verification | Low to medium — largely estimated in general trade |

| Decisions relying on it | Revenue recognition, receivables, production planning | Scheme settlement, claims validation, stock-in-trade, demand sensing | Brand share, category trends, consumer promotions |

The pattern is simple: accuracy and control fall with every tier you descend, while decision relevance for trade spend rises. The money decisions — which claims to pay, which schemes performed — depend on the middle tier, where the manufacturer controls neither the recording nor, without deliberate verification, the quality.

How secondary sales are tracked in India

Indian manufacturers capture secondary data through a ladder of methods, each trading effort for reliability. Most mid-market channels run a mix — a few hundred digitised distributors, a long tail on spreadsheets.

Manual distributor statements. The floor: distributors submit periodic sales statements, usually as spreadsheets or scanned summaries. Cheap to start and universally available, but slow, inconsistent in format, easy to fat-finger and easiest to inflate — this is the tier where claim disputes are born, and where revenue leakage concentrates.

Billing-software exports. A step up: the distributor exports invoice-level data from whatever billing package they run. Because the export comes from the system that actually raised the retailer invoices, it is harder to fabricate wholesale — but formats vary by package, master data (SKU codes, retailer names) rarely matches the manufacturer's, and the mapping effort is real.

Distributor management systems. A DMS puts distributor billing on a platform the manufacturer sponsors, so secondary sales are captured at source in a consistent structure with aligned masters. Reliability is the best of any method — but so is the effort: licensing, onboarding, and the ongoing push to keep distributors actually billing through it rather than around it. Coverage in mid-market networks is typically partial.

SFA-reported retail orders. Sales force automation tools capture the orders a company salesperson books at retail outlets. Useful as a near-real-time demand signal and a cross-check, but an order booked is not an invoice billed — SFA data approximates secondary sales rather than recording them, and is best treated as corroboration, not settlement basis.

The practical implication: for most Indian manufacturers, settlement-grade secondary data arrives as files, in mixed formats, from systems they do not control — which is why verification, not collection, is the real discipline.

How to verify secondary sales data

Because secondary data is channel-originated, it should be treated the way an auditor treats any third-party representation: reconcile it, sample it, cross-check it. Four checks do most of the work:

- The stock equation. Opening stock + primary purchases − closing stock = maximum possible secondary sales. If a distributor claims secondary of 5,000 cases but opening stock plus primaries minus a plausible closing stock supports only 4,200, the claim is arithmetically impossible. This single reconciliation catches the largest category of inflation, and it uses primary data you already own. (Worked distributor-level examples are in how to calculate FMCG distributor claims.)

- Invoice-level sampling. Pick a sample of reported secondary lines and ask for the underlying retailer invoices. You are not auditing every line — you are making fabrication risky. Distributors who know invoices get sampled report more carefully.

- GST-document cross-checks. Where the downstream buyer is registered, the distributor's outward supplies leave a GST trail that reported secondary data should be consistent with — a pointer-level sanity check, not a line-by-line audit. The documentation side of this is covered in the scheme settlement GST documentation playbook.

- Duplicate-retailer checks. Screen reported data for the same retailer appearing under multiple spellings or codes, impossible volumes for a single outlet, and retailers that appear only in scheme windows. Inflated universes and ghost outlets are a classic pattern in incentive-linked reporting.

None of these checks require live systems integration. They require the claim to arrive structured — with the stock statement, the invoice sample and the retailer detail attached — so the checks can actually run before approval.

Why claims and schemes depend on secondary data

Here is why the definitions above are a finance problem and not just a sales-analytics one: almost every rupee of Indian trade spend that flows back up the channel settles on secondary-tier evidence.

Walk through the claim types (a full taxonomy is in types of trade schemes in India):

- Secondary schemes pay the distributor on sales to retailers — the qualifying quantity is a secondary number.

- Retailer incentives (displays, slabs, visibility programs) are funded by the manufacturer but executed and first-paid a tier down; the reimbursement claim rides on secondary records of who sold what to whom.

- Damage and expiry claims depend on stock reconciliation — and the stock position is only known if secondary movement is known.

- Stock compensation and price protection pay on the inventory held in trade on a cut-off date — again, a number derived from primary minus secondary.

Now consider the standard failure mode: these claims arrive as unverified spreadsheets attached to emails. Nothing structurally prevents a claimed secondary quantity that exceeds the stock equation. Nothing flags the same retailer invoice supporting two different claims across two schemes. Nothing tracks which claims have sat unresolved for 90 days while the distributor nets the disputed amount off a payment. The predictable results are over-claiming that gets paid because checking is manual, duplicates that surface only in year-end reconciliation, and ageing disputes that poison distributor relationships — the same leakage patterns catalogued in revenue leakage in rebate programs and mirrored on the receivables side in deduction management.

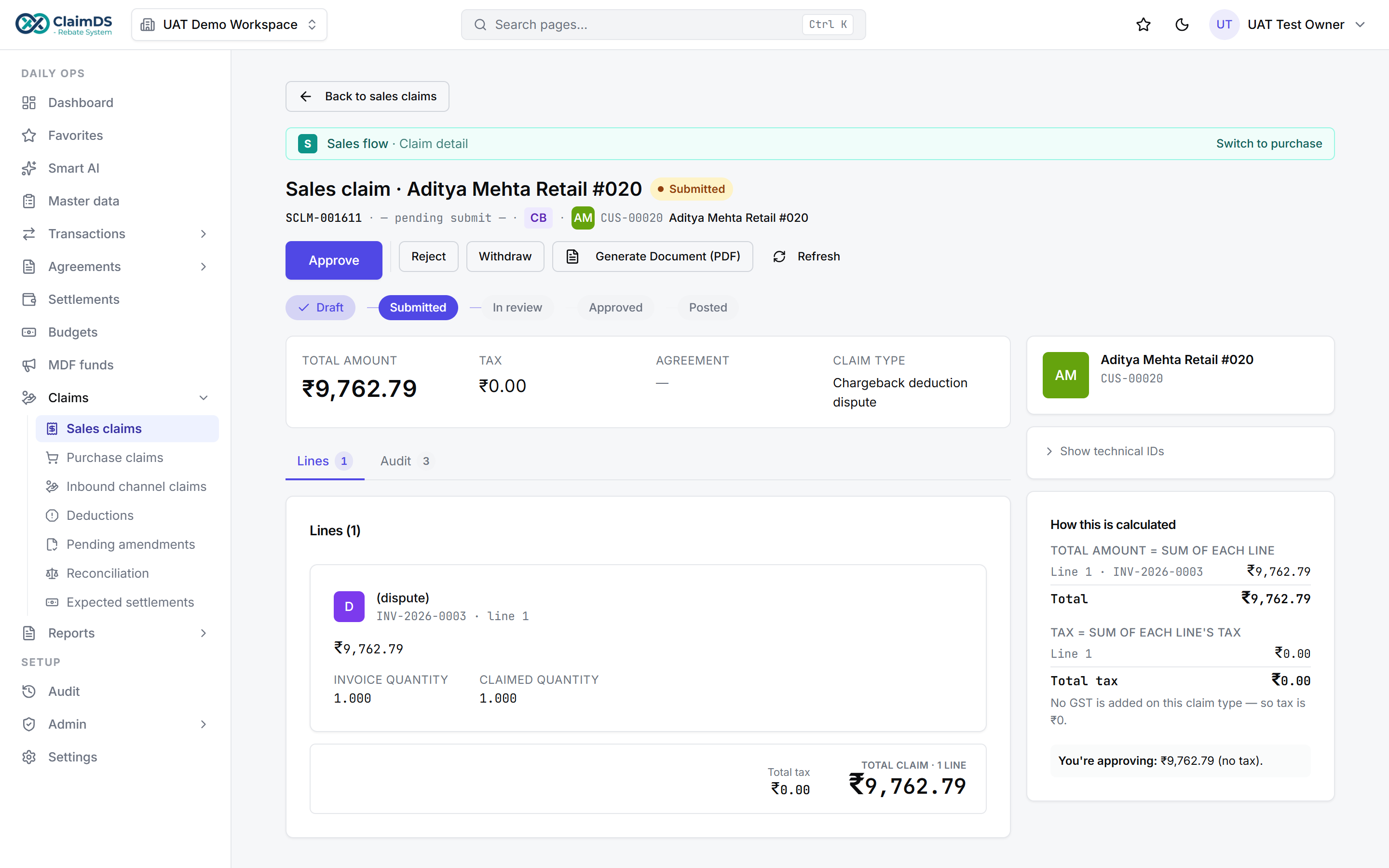

The fix is structural, not heroic effort: structured claim intake with supporting data, followed by validation before approval. Each claim enters as a record — scheme, period, distributor, claimed quantity and value — with its evidence (stock statements, invoice samples, retailer detail) attached to the claim itself rather than buried in an inbox. Validation rules run the checks from the previous section against the claim. The claim then moves through a controlled lifecycle: Submitted, then Validated once the data survives the checks, then Approved by someone with the authority and the evidence in front of them, then Settled — with every state change logged. That is the working model behind claims management software and the approval workflow discipline that goes with it.

Here is what that looks like in practice — a distributor claim validated against its supporting data before settlement:

Once intake is structured, the secondary-data problem becomes tractable: the claim can only be approved when its evidence reconciles, duplicates are caught at entry rather than at year-end, and disputes age visibly instead of silently.

Channel loading vs real demand

A short warning that ties the tiers together: primary-only measurement misleads, systematically and in one direction. When targets are set on primary billing, month-end loading follows — distributors are pushed to accept stock that demand has not asked for. The primary line looks strong; the secondary line, if anyone looked, would show the gap opening up as stock-in-trade.

The costs land later and lower: distributors carry the working-capital burden of inventory they did not need, ageing stock converts into expiry and damage claims, and next period's primaries sag because the channel is already full. The scheme design counterweight — paying on sell-through rather than sell-in — is covered in sell-in vs sell-through rebates; the measurement counterweight is simpler: track secondary, and read primary against it.

Settling claims on verified secondary data

The three-tier vocabulary is the easy part. The operational reality is that secondary data — the tier your schemes and claims actually settle on — originates in systems you do not control and arrives in formats you did not choose. The businesses that run channel finance well are not the ones with perfect data; they are the ones whose claims process assumes imperfect data and verifies it before paying.

ClaimDS is built for exactly that: structured claim intake with supporting data, validation rules that run the stock-equation and duplicate checks before approval, a controlled Submitted-to-Settled lifecycle with an audit trail, and GST-compliant credit-note settlement. It works alongside your DMS and ERP through file-based import — the same spreadsheets and exports your channel already produces, given structure and verification (the integration patterns are in ERP integration for claims and rebate software). The broader platform context sits in rebate management software and trade promotion management software, and the channel-incentive side in channel partner incentive tracking.

Note: This article is general information about Indian distribution and trade-scheme practice, not accounting, tax or legal advice. Verify scheme, GST and documentation positions for your specific facts with a qualified professional.

Frequently asked questions

What is the difference between primary and secondary sales?

Primary sales are the manufacturer's sales to its distributors, recorded in the manufacturer's own invoicing or ERP. Secondary sales are the distributor's onward sales to retailers, recorded in the distributor's billing software or DMS. The manufacturer owns primary data natively; secondary data must be reported up from the channel.

What is tertiary sales?

Tertiary sales are the retailer's sales to the end consumer — the final tier of the chain. In Indian general trade they are rarely measured directly; they are approximated through retail audits, point-of-sale data in modern trade, and loyalty or consumer-activation programs.

Where does secondary sales data come from?

From the distributor's side of the chain — their billing software, a distributor management system (DMS), or retail orders captured by a sales force automation (SFA) tool. In less digitised channels it arrives as manual statements or spreadsheet exports submitted by the distributor.

What is secondary sales tracking?

Secondary sales tracking is the process of capturing distributor-to-retailer sales — by SKU, retailer and period — so the manufacturer can see real offtake, monitor stock in trade, and settle schemes that pay on sell-through rather than on primary billing.

Why do manufacturers need secondary sales data?

Because primary billing only shows what was pushed into the channel, not what moved through it. Secondary data reveals true demand, exposes channel loading, shows stock held in trade, and is the settlement basis for most Indian trade schemes — secondary schemes, retailer incentives and damage or expiry claims all depend on it.

What is a secondary scheme?

A secondary scheme is a trade incentive that pays on the distributor's sales to retailers rather than on the distributor's purchases from the manufacturer. Because the qualifying data originates in the distributor's records, secondary schemes require reported secondary sales data to compute and settle.

What is channel loading?

Channel loading (or channel stuffing) is billing extra stock to distributors near period-end to inflate primary sales — often to hit targets. It books revenue without real demand, pushes working-capital cost onto distributors, and typically shows up later as returns, expiry claims and slow subsequent-period primaries.

How can secondary sales data be verified?

The core check is a stock reconciliation - opening stock plus primary purchases minus closing stock should equal claimed secondary sales. Beyond that, sample underlying retailer invoices, cross-check against GST documents where applicable, and screen for duplicate or non-existent retailers in the reported data.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

How to Calculate Supplier Rebate Accruals Accurately (Step-by-Step)

A step-by-step method for calculating supplier rebate accruals (rebates receivable) — measurement basis, attainment estimation, reconciliation to supplier statements, and true-up.

ERP Integration for Claims, Rebate & TPM Software: What Indian Businesses Should Check

Why ERP integration decides claims/rebate/TPM software success in India — the data flows that matter, integration patterns, the Indian ERP landscape, and a readiness checklist.

Rebate Analytics: Reporting, Dashboards & Opportunity Analysis

What rebate analytics should deliver — real-time accrual dashboards, liability forecasting, scheme profitability, partner performance and slab-proximity opportunity analysis.