Claims & Deductions Management for CFOs: A Revenue-Leakage Playbook

A CFO's playbook for channel claims and deductions — quantifying revenue leakage, accrual visibility, GST exposure, the control framework and the KPIs to track.

For a CFO, claims and deductions management is a revenue-leakage problem dressed up as an admin one. Unmanaged channel claims commonly bleed an estimated 1–3% of turnover through miscalculation, unclaimed accruals and under-settled credit notes. The fix is a control framework: live accrual visibility, audit trails, a credit-note policy, and a handful of KPIs.

Quantifying the leakage

The first job is to size the problem in rupees, not adjectives. Leakage is the gap between what schemes should have settled and what was actually settled, plus unclaimed accruals and write-offs. As a rule of thumb, businesses running manual processes commonly estimate 1–3% of channel turnover lost — but a finance leader should measure their own number, not borrow one. The transparent method is in the ROI & settlement-time benchmark guide.

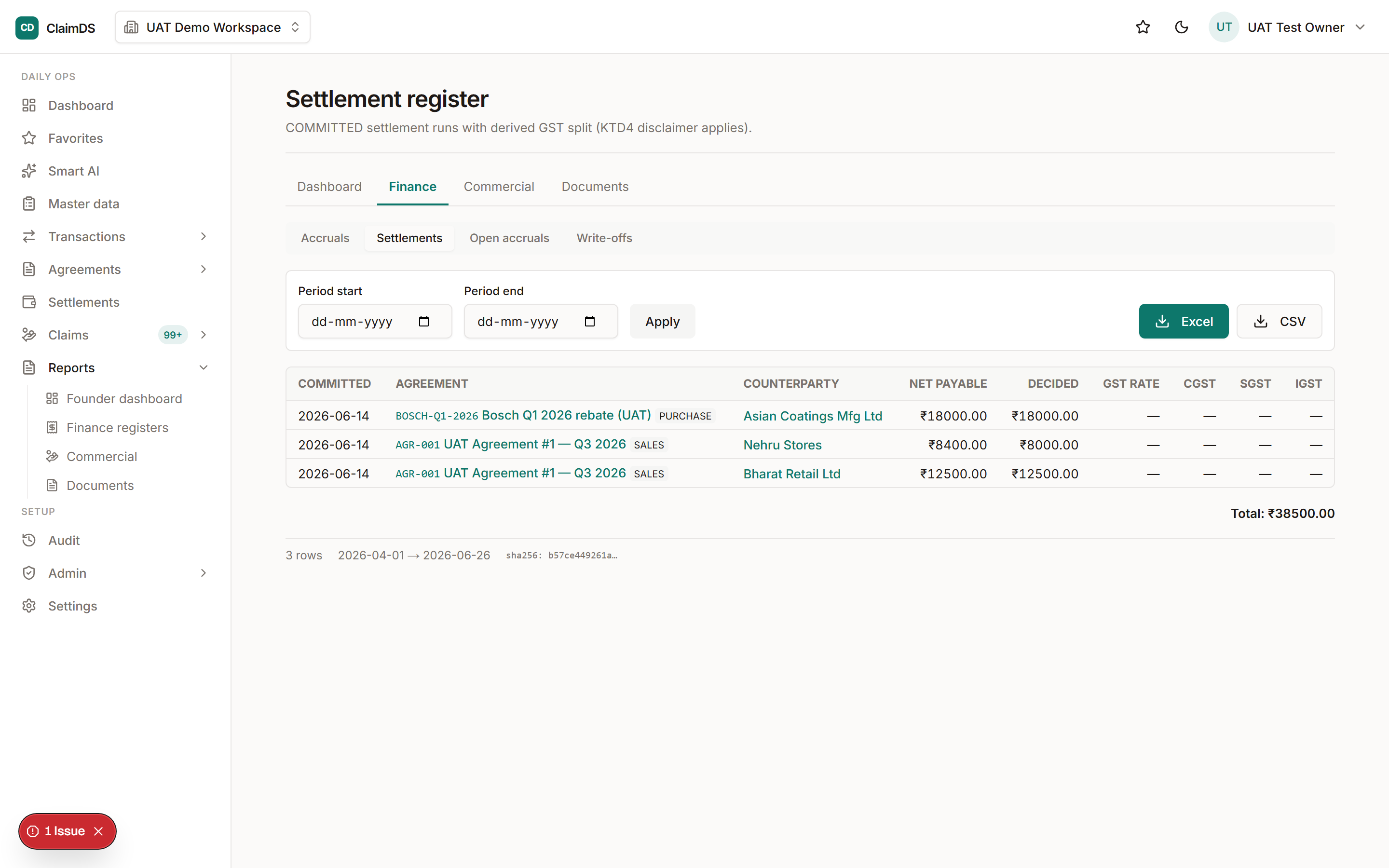

Accrual visibility

You cannot control what you cannot see. A live accrued-liability view — what the business owes and is owed across every scheme — is the single most valuable thing a CFO can demand. Spreadsheets give a quarter-end estimate; software gives a real-time number. This underpins rebate accounting and the operational view in distributor claims management.

GST exposure

The compliance exposure is concentrated in one decision: the credit-note type. Issuing a tax credit note where a financial one applies — or the reverse — can create unexpected ITC reversals or lost tax at assessment. A documented policy and audit trail manage it; see financial vs. tax credit notes and CBIC Circular 251.

The control framework

- Single source of truth for every scheme and claim.

- Live accrual with exact-decimal math.

- Validation of every claim against agreement and data.

- Segregation of duties in approval.

- Documented credit-note policy (tax vs financial).

- Immutable audit trail for assessment and disputes.

- Reconciliation of settlement to accrual before close.

KPIs to demand

| KPI | What it reveals |

|---|---|

| Settlement TAT | How fast claims close |

| Claim-to-settlement accuracy | How often the settled amount matches the claim |

| Leakage % | Value lost vs turnover |

| Days-deduction-outstanding | Ageing of unresolved deductions |

| Dispute recovery rate | Share of disputed amounts recovered |

The deduction-specific view is in deduction management.

GST note: This article is general information, not tax or legal advice. GST positions — including CBIC Circular No. 251/08/2025-GST and the Finance Act 2026 amendments to Section 34 of the CGST Act, assented 30 March 2026 but not yet notified into force as of publication — must be re-verified at publish time with a qualified professional.

Frequently asked questions

How do you quantify revenue leakage from channel claims?

Estimate leakage as the gap between what schemes should have settled and what was actually settled, plus unclaimed accruals and write-offs. Expressed as a percentage of channel turnover, it is commonly in the 1-3% range for businesses running manual processes, though you should measure your own.

What KPIs should a CFO track for claims and deductions?

Settlement turnaround time, claim-to-settlement accuracy, leakage percentage, days-deduction-outstanding, and dispute recovery rate. Together they show whether the claim process is controlled and where it leaks.

What is the GST exposure in channel claims?

The main exposure is issuing the wrong credit-note type — a tax credit note where a financial one applies, or vice versa — which can create unexpected ITC reversals or lost tax. A documented credit-note policy and audit trail manage this.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Claims Management ROI & Settlement-Time Benchmark Guide

A transparent ROI framework for channel-claim automation and a settlement-time benchmark methodology — inputs, formula and a worked, illustrative example.

Trade Promotion Software for CPG: Control Trade Spend in India

Trade promotion software for CPG & FMCG in India: why trade spend leaks, what to manage, and how to use ClaimDS to plan, settle and measure schemes.

What Is Claims Management Software? A Practical Guide

Claims management software, explained: what it is, the claim lifecycle, the Indian claim types it settles, GST credit notes, and how to choose one.