Expiry and Breakage Returns in Pharma

How pharma expiry and breakage returns work — saleable vs non-saleable, near-expiry, destruction, and how the stockist claim settles by credit note.

Time-expired and damaged stock is the biggest reverse flow in pharma. It comes back up the CFA and stockist chain, gets sorted into saleable and non-saleable, and settles either by replacement stock or a credit note — with the batch and expiry trail deciding how the tax lands. This is the pharma-specific playbook: the return-policy norms, the near-expiry window, and destruction. The cross-industry version, covering FMCG too, is in credit notes for expired and damaged goods returns; the wider channel picture sits in the pharma channel claims and rebates guide.

What is the difference between saleable and non-saleable returns?

The first sort every pharma return goes through is saleable versus non-saleable, because it decides whether the stock re-enters inventory or heads for destruction — and often who carries the cost.

A saleable return is stock that is still fit to sell: good packaging, adequate shelf life, correct batch. It is typically near-expiry stock a stockist sends back to rebalance, or over-supply pulled from a slow branch. It can be re-warehoused and redistributed, so the manufacturer recovers value and the credit reflects that.

A non-saleable return cannot go back on a shelf — it is expired, broken, leaking, or otherwise unfit — so it is destroyed. There is no recovery; the credit note is the whole settlement, and a destruction certificate stands in for the goods.

| Saleable return | Non-saleable return | |

|---|---|---|

| Condition | Fit to sell — shelf life intact, packaging sound | Expired, damaged, or unfit |

| Typical trigger | Near-expiry rebalancing, over-supply | Post-expiry, breakage, quality failure |

| Physical outcome | Re-warehoused, redistributed | Destroyed against a certificate |

| Who usually bears it | Shared or manufacturer, per policy | Manufacturer, within window |

| Settlement instrument | Credit note or replacement | Credit note plus ITC reversal on destruction |

Who bears each is set by the return policy, not decided per claim. Most agreements have the manufacturer absorb non-saleable returns inside the window and share or decline stock returned late or beyond a value cap. Getting the split wrong is a classic leakage point — the same discipline covered in deduction management best practices and the broader distributor claims management workflow. Where the return is really a price event rather than an expiry event, it belongs with price-protection rate-difference credit notes, not here.

How does the expiry return window and near-expiry handling work?

Pharma return policies are built around a window rather than a single date. Stock is accepted for return within a defined period before and after the printed expiry — commonly a few months on each side, set by the manufacturer's policy — so the channel is not stuck with stock that turned unsaleable overnight.

The pre-expiry side is the near-expiry return. A stockist watching a batch approach expiry can send it back proactively, while it still holds value, rather than let it expire on the shelf. Returning early lets the manufacturer redistribute the batch to a faster-moving market or plan destruction in an orderly run, and it converts a probable full write-off into a partial recovery. This is why near-expiry visibility matters: the earlier a batch is flagged, the more of its value survives.

The post-expiry side is the true expiry return. Here the stock is non-saleable by definition, so the claim is about value recovery and correct destruction, not resale. Policies usually taper the credit — full value near expiry, reduced value the further past it the return arrives — and cut it off entirely once the outer window closes. Stock returned after that stays with the channel.

Everything keys on the batch and expiry evidence. Each returned line is validated batch-wise against the original supply: which invoice it traces to, how much shelf life remained, whether the quantity claimed is plausible against what was bought. A return without a batch number cannot be placed on the timeline and cannot be checked for duplication against claims already settled. The batch-level settlement mechanics carry over from chargebacks in pharma distribution and the pharma stockist claim settlement process, and connect upstream to primary, secondary and tertiary sales records.

How are breakage, damage and transit shortage handled?

Breakage and damage differ from expiry in one practical way: the trigger is physical, not a date, and the stock often never travels back.

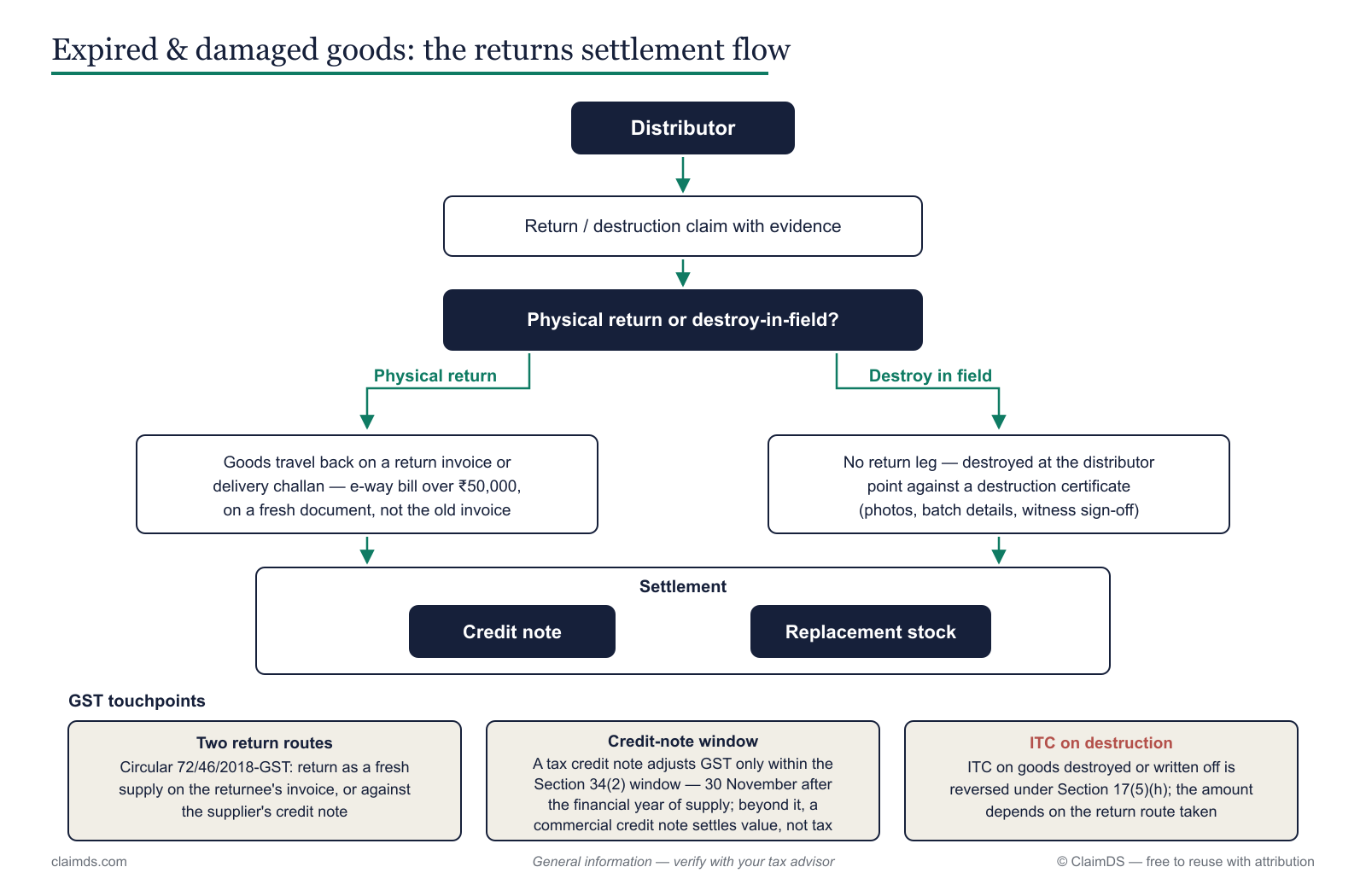

Breakage and damage — crushed strips, broken vials, leaking bottles — are usually discovered at the stockist or retail point. Freight rarely justifies returning broken stock, so field practice is destruction at the point of discovery against a destruction certificate, with photographs and batch details, followed by a credit note. The evidence is the certificate and the images; there is no goods-received leg to match.

Transit shortage is different again: the quantity billed did not arrive. The evidence is the delivery documentation — the gate or goods-received note against the invoice and packing list, ideally flagged at the point of receipt. Because the goods were never received, this is a supply-side reconciliation, not a return of unfit stock, and it settles as a short-supply credit rather than a destruction claim.

The common thread is that each route has its own evidence standard and its own settlement path, and mixing them up is where disputes start. A breakage claim needs a certificate; a shortage claim needs receipt documentation; an expiry claim needs the batch-and-window trail. Handling these consistently is part of the same post-settlement discipline as returns, reversals and cancellations on channel claims and the mechanics explained in reversals explained.

Return, replacement or destruction — which route settles the claim?

Every accepted return resolves down one of three routes, and each leaves a different mark on the claim record, the stock ledger and the tax document.

Physical return — the goods travel back up the chain for re-warehousing (saleable) or centralised destruction (non-saleable). The claim record carries a goods-received verification; the stock ledger books the return; the tax document is a credit note, or the return moves as a fresh supply.

Replacement — instead of crediting money, the manufacturer ships fresh stock in place of the returned batch. The claim closes against replacement stock, the ledger swaps one batch for another, and the value is settled in kind rather than in a credit note.

Destruction — the stock never comes back; it is destroyed in the field or at the depot against a certificate. The claim record leans on that certificate, the stock is written off, and the tax document is a credit note plus a reversal on the destroyed goods.

Expiry and damage returns settle by credit note or replacement; destroyed stock triggers an ITC reversal — the full GST routes are in the pharma GST guide.

The tax treatment of each route — the two Circular 72/46/2018 return routes, whether the credit note carries tax, and the Section 17(5)(h) ITC reversal on destroyed stock — is a topic in its own right. It lives in the GST treatment of pharma claims and returns satellite, alongside financial vs. tax credit notes under GST and ITC reversal on post-sale discounts and credit notes. Choosing a route is a claim decision here; its tax consequence is documented there, and the underlying instrument is defined in credit note.

What evidence and audit trail does an expiry claim need?

An expiry or breakage claim survives audit only if the physical, financial and tax trails line up, and that depends on a short, non-negotiable evidence set:

- Batch number and expiry date — the key everything else links to; without it the claim cannot be placed on the window or checked for duplication.

- Original supply reference — the invoice the returned stock traces to, so quantity and value can be validated batch-wise.

- Destruction certificate or goods-received proof — a countersigned certificate with photographs for destroyed stock, or a receipt record for stock that travels back.

- Return-policy reference — the clause that admits the claim: which window applied, saleable or non-saleable, what credit percentage the taper allows.

- Claim window and dates — the return date against the expiry date, proving the claim falls inside the accepted period.

- Credit note linkage — the settlement document cross-referenced to the claim and, where relevant, the GSTR reconciliation and credit-note time limits.

Kept together, this file lets a claim be reconstructed end to end. It also keeps expiry returns clean of the clawback and cancellation problems described in rebate clawbacks and scheme cancellations, and sits within the sector-wide buyback in pharma and GST treatment of FMCG claims and schemes context for teams running both.

Bring the three trails together

Every pharma expiry claim lives in three systems at once — a stock trail, a financial trail, and a tax trail — and manual handling lets them drift. ClaimDS ties each return to its batch verification, applies the return-policy window automatically, and keeps the credit note, claim and destruction record linked and auditable. Book a demo to see expiry and breakage returns settle cleanly, or sign up for the ClaimDS newsletter for more on pharma channel claims.

Frequently asked questions

What is an expiry return in pharma?

An expiry return is time-expired medicine sent back up the channel — retailer to stockist to CFA to manufacturer — because it can no longer be sold. Pharma return policies accept stock within a defined window around the printed expiry date, and each claim is validated batch-wise against the original supply before it is credited or destroyed.

What is a non-saleable return?

A non-saleable return is stock that cannot go back into sellable inventory — it is expired, damaged, broken or otherwise unfit — so it is destroyed rather than restocked. The manufacturer typically bears non-saleable returns under the return policy and settles them by credit note, with a destruction certificate standing in for the physical goods.

What is a near-expiry return?

A near-expiry return is stock sent back before its expiry date, inside the notice window the return policy allows — often several months ahead. Returning proactively lets the stockist clear slow-moving batches while they still hold value, and lets the manufacturer redistribute or plan destruction early instead of absorbing a full-value write-off after expiry.

How is a pharma expiry claim settled?

Settlement runs on the batch and expiry trail. Once the CFA or manufacturer verifies the returned quantity and batch against the original supply, the claim settles either by replacement stock or a credit note. The credit note may be a tax or commercial document depending on timing, and destroyed stock triggers a separate ITC reversal.

Who bears the cost of expired pharma stock?

It depends on the return policy. Saleable and non-saleable returns inside the agreed window are usually borne by the manufacturer and credited to the stockist, while stock returned outside the window, or beyond policy limits, often stays with the channel. The batch and expiry records decide which side of the line a given claim falls.

What is a destruction certificate in pharma returns?

A destruction certificate is the document that proves expired or damaged stock was destroyed rather than resold. It records batch numbers, expiry dates and quantities, is countersigned by a company representative or third-party witness, and usually carries photographs. For destroyed stock it replaces the physical return as the evidence the credit note and ITC reversal rely on.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.