How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Settling an agri-input dealer or distributor claim runs through six stages: the seasonal scheme circular fixes the terms, the dealer files the claim at the season or period cut-off with stock and sell-through data, a field or sales officer verifies it, finance validates it against the scheme rules and stock data, an approver signs off per the delegation-of-authority matrix, and the claim is settled by credit note and reconciled. The season cycle and the shelf life of agri-inputs make two controls decisive: the stock and liquidation declaration at the cut-off, and filing inside the claim window.

All ₹ figures below are illustrative, not benchmarks. Your scheme circular, dealer agreement and stock records always govern. This guide owns the end-to-end settlement process; for the wider picture across agri-input channel claims, schemes and returns, see the pillar on agrochemical channel claims and rebates in India. The seasonal and liquidation mechanics sit in agri-input seasonal schemes and liquidation claims, and the returns side in agri-input expiry, damage and season returns. Agri-input claims sit inside a multi-tier structure, mapped in the India multi-tier channel claim map and the distributor vs dealer vs super-stockist distinction.

The six-stage agri-input claim settlement process

Every agri-input claim — a seasonal scheme claim, a liquidation claim, a near-expiry return, a price-protection claim — moves through the same six stages. What makes the agri-input version distinctive is the season: schemes open and close on the crop calendar, stock has a shelf life, and the claim you file depends on what actually liquidated to farmers, not just what you bought. The generic version of this lifecycle is set out in the claim process explained; below is the agri-input-specific shape.

Stage 1 — Seasonal scheme circular and terms

Everything downstream traces back to the scheme circular. For an agri-input season it fixes the qualifying products, the crop-season window (Kharif, Rabi or a specific dispatch period), the slab or per-unit rate, any caps, whether the scheme pays on purchase or on liquidation, and — critically — the claim window and the stock declaration required at the cut-off. If the circular is ambiguous about whether it rewards primary purchase or secondary liquidation, every claim under it inherits that ambiguity and disputes multiply at validation. A clean circular names the base, states whether unsold or returned stock nets off, and fixes the evidence a claim must carry. The menu of scheme designs a circular can describe is mapped in types of trade schemes in India, and the purchase-versus-liquidation choice in purchase incentives. This stage costs little time but sets the ceiling on how cleanly the rest run.

Stage 2 — Dealer or distributor files the claim at the cut-off

At the season or period cut-off, the dealer or distributor computes the claim against the circular and files it with supporting data. Because agri-input schemes usually pay on liquidation, this means more than the purchase invoice: it means the stock-in-hand declaration at the cut-off, and the sell-through or liquidation data showing what actually moved to retailers and farmers. The gap between stock bought and stock liquidated is the whole story of a seasonal claim. Filing inside the claim window matters as much as the amount — a correct claim filed after the window closes is still rejected, and season windows are tight. The distinction between what the channel buys and what it retails is the primary-versus-secondary split in primary, secondary and tertiary sales. In ClaimDS, dealers and internal teams file claims against the specific scheme circular and attach the stock declaration, invoices and liquidation data in one place. <!-- TODO: confirm capability wording with founder --> The step-by-step is documented in submit a sales claim.

Stage 3 — Field or sales-officer verification

Before finance sees the claim, someone closer to the market verifies what the data alone cannot show. A field or sales officer confirms the declared stock is really on the shelf, that the liquidation to farmers looks genuine for that territory, and — for a near-expiry return — that the stock is what the claim says it is. This is the human check on the cut-off declaration, and it is where inflated-stock and phantom-liquidation leakage is caught early rather than clawed back later. The trade-off is speed: routing every claim through a field visit slows the pipeline, so most companies verify by exception — value threshold, claim type, or a risk flag on the stock declaration — rather than universally. Near-expiry and damage claims almost always need it, because they hinge on physical stock; the treatment of those movements sits in GST on stock transfers and warranty replacements in the channel. Clear ownership at this stage keeps it from becoming a bottleneck.

Stage 4 — Finance validation against scheme rules and stock data

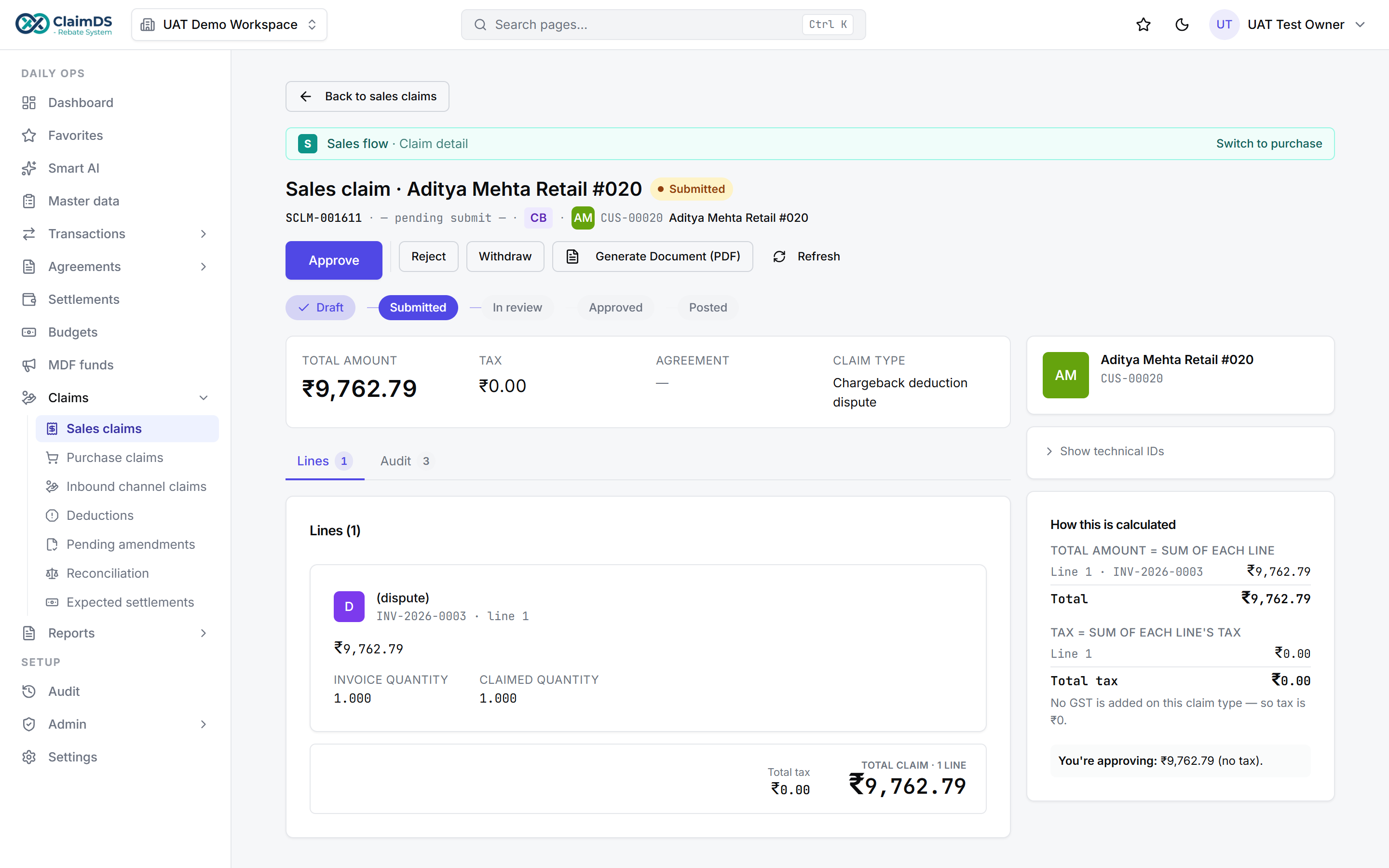

This is the stage that most determines whether settlement is defensible. Finance recomputes the claim from the base rather than trusting the filed figure: does the declared stock reconcile to system stock and dispatch records, does the liquidation match secondary-sales data, is the rate the circular's rate on the correct base, is it within any cap, was it filed in the window, was the right season period claimed, does it duplicate a claim already settled? For agri-inputs the extra test is stock integrity — an overstated cut-off declaration is the single biggest over-claim risk. Validation is arithmetic plus rule-checking against the scheme and the stock ledger, and it is exacting precisely because a wrong approval here becomes a real over-payment. ClaimDS validates each claim against its own scheme circular, eligibility, caps and the stock and liquidation data, and flags mismatches, breached caps and likely duplicates for a reviewer rather than passing them silently. <!-- TODO: confirm capability wording with founder -->

Validation: a seasonal claim checked against its scheme rules and stock data.

Validation: a seasonal claim checked against its scheme rules and stock data.

The over-claims caught here are the ones that otherwise become deductions and disputes downstream — the mechanism behind revenue leakage in rebate programs and the discipline in deduction management best practices.

Ready to see validation run on your own agri-input claims? Book a demo and we will walk a live seasonal claim through the six stages on your data.

Stage 5 — Approval per the delegation-of-authority matrix

A validated claim still needs sign-off, and the delegation-of-authority matrix decides who signs. Approval routes by value: a territory or area manager clears smaller claims, while larger seasonal settlements escalate to a regional controller or finance head. The matrix exists to keep small claims fast without letting a large one settle on one person's say-so — and to leave an audit trail of who approved what. In a season-driven business, where a whole territory's claims land in the same fortnight, well-designed approval routing is the difference between a queue that clears before the next season opens and one that stalls on a single approver; the patterns are in claim and rebate approval workflows and the finance-owner view in claims and deductions management for the CFO. ClaimDS routes each claim to the right approver by value and records every approval and rejection with a reason. <!-- TODO: confirm capability wording with founder --> The workflow is documented in the claim approval workflow.

Stage 6 — Credit-note settlement and reconciliation

Once approved, the claim is settled — in the Indian agri-input channel, usually by credit note against the dealer or distributor account rather than cash, because it offsets what the party owes and keeps the GST trail clean. The credit note must carry the right GST treatment; whether it is a financial or tax credit note changes the reporting, as set out in financial vs tax credit notes under GST and GST credit notes for rebates under Rule 53(1A). Scheme payouts to dealers can also attract TDS — the ground covered in Section 194R TDS on dealer and distributor incentives. The GST treatment specific to agri-input schemes is in GST treatment of agri-input claims and schemes. Settlement is not the end: the credit note has to be reconciled back against the accrual and, on the GST side, against the returns — the discipline in reconciling scheme credit notes to GSTR-2B/3B. ClaimDS settles approved claims by credit note or payment and reconciles each one against its accrual and the party account. <!-- TODO: confirm capability wording with founder --> The how-to is in reconcile a claim to a credit note, and cancellations in rebate clawbacks and scheme cancellations.

The evidence standard

An agri-input claim is only as strong as the evidence it carries, and agri-input evidence is unusual because it reaches back to stock and shelf life, not just to a sale. A valid claim ties an amount to a declared stock position at the cut-off, the liquidation that actually happened, and the scheme it is claimed under — so validation can recompute it and audit can trace it later. The table below sets out what each claim type must carry. Where any row is missing, the claim stalls at verification; the same evidence gap is what turns a legitimate claim into a downstream deduction, as covered in returns, reversals and cancellations in channel claims.

| Claim type | Evidence required |

|---|---|

| Seasonal scheme | Scheme circular reference, purchase invoices for the period, stock-in-hand declaration at the cut-off, qualifying-product proof |

| Liquidation / sell-through | Secondary-sales or sell-through data to retailers and farmers, opening and closing stock, batch detail where required |

| Near-expiry return | Batch number and expiry date, physical stock proof, original inward invoice, return authorisation |

| Price protection | Original purchase price, revised price with effective date, stock-in-hand at the revision date |

| Damage | Damage proof or photograph, batch and quantity, inward invoice, claim authorisation |

The control that runs through every row is the stock declaration at the season cut-off. It fixes what was bought, what liquidated and what remains, and it is also the highest fraud risk in the agri-input channel: an inflated stock declaration inflates the claim directly, and unsold stock declared as liquidated becomes a return or a write-off next season. This is why validation reconciles the declared figure against system stock and sell-through before anything settles, and why near-expiry and damage handling is a discipline of its own, covered in credit notes for expired and damaged goods returns.

Why agri-input claims get rejected

Most rejections are not judgement calls — they are concrete failures against the scheme circular or the stock ledger, and each has a specific fix. Knowing the recurring eight lets a dealer file clean the first time and lets finance reject consistently rather than case by case. The eight below account for the bulk of a typical agri-input claim reject pile.

- Filed outside the claim window. A correct claim submitted after the season's window closed. Fix: file inside the window; in a season-driven trade the window is tight and a late claim is rejected however valid the amount.

- Stock mismatch. The declared cut-off stock does not reconcile to system stock or dispatch records. Fix: reconcile the stock statement to the ledger before filing, and file the corrected figure.

- Missing sell-through proof. A liquidation scheme is claimed with no secondary-sales data to show stock actually moved. Fix: attach the sell-through or retailer-liquidation data the circular requires.

- Wrong season period. Stock or sales from the wrong crop season or dispatch period is claimed. Fix: check the circular's period boundary and claim only the qualifying window.

- Expired stock claimed as saleable. Near-expiry or expired stock is filed as eligible scheme stock. Fix: route expired stock through the returns process, not the scheme claim; only saleable stock qualifies.

- Wrong price-revision date. A price-protection claim uses the wrong effective date for the revised price. Fix: claim protection only on stock held at the correct revision date, per price protection and rate-difference credit notes under GST.

- Duplicate claim. The same scheme, period and stock was already claimed and settled. Fix: check the claim history for that party and period and withdraw the duplicate.

- Scheme-rule misread. The claim assumes a base or rate the circular does not support — buy-in read as liquidation, or a slab misapplied. Fix: validate against the circular's exact terms before filing.

The over-claims and disputes these prevent are the same leakage discussed in revenue leakage in rebate programs; the arithmetic behind eligibility sits in the accrual view of purchase incentives.

Spreadsheets vs a claims system

Most agri-input claim operations start in a spreadsheet, and for a handful of claims a season that is fine. What breaks is the season peak — agri-input claims are stock-level and liquidation-level, they all land in the same fortnight, and a spreadsheet has no way to check one cut-off declaration against system stock or against the thousands of claims already settled. The comparison below is about operational reality, not a promised return; it is the argument for a purpose-built dealer claims management system over a shared file, and it applies equally to a distributor claim settlement desk running the same seasonal volume.

| What has to happen | In a spreadsheet | In a claims system |

|---|---|---|

| Stock declaration vs ledger | Manual lookup across tabs and files | Declared stock checked against system stock |

| Liquidation / sell-through match | Re-keyed, easily missed | Claim tied to its secondary-sales data |

| Duplicate detection | Eyeballed at season peak | Flagged automatically on party and period |

| Audit trail | Overwritten cells, no history | Every action recorded with who and when |

| Ageing visibility | Rebuilt by hand each week | Ageing and status across the network live |

| Validation against the circular | Re-typed rules, drift over time | Claim checked against its own scheme rules |

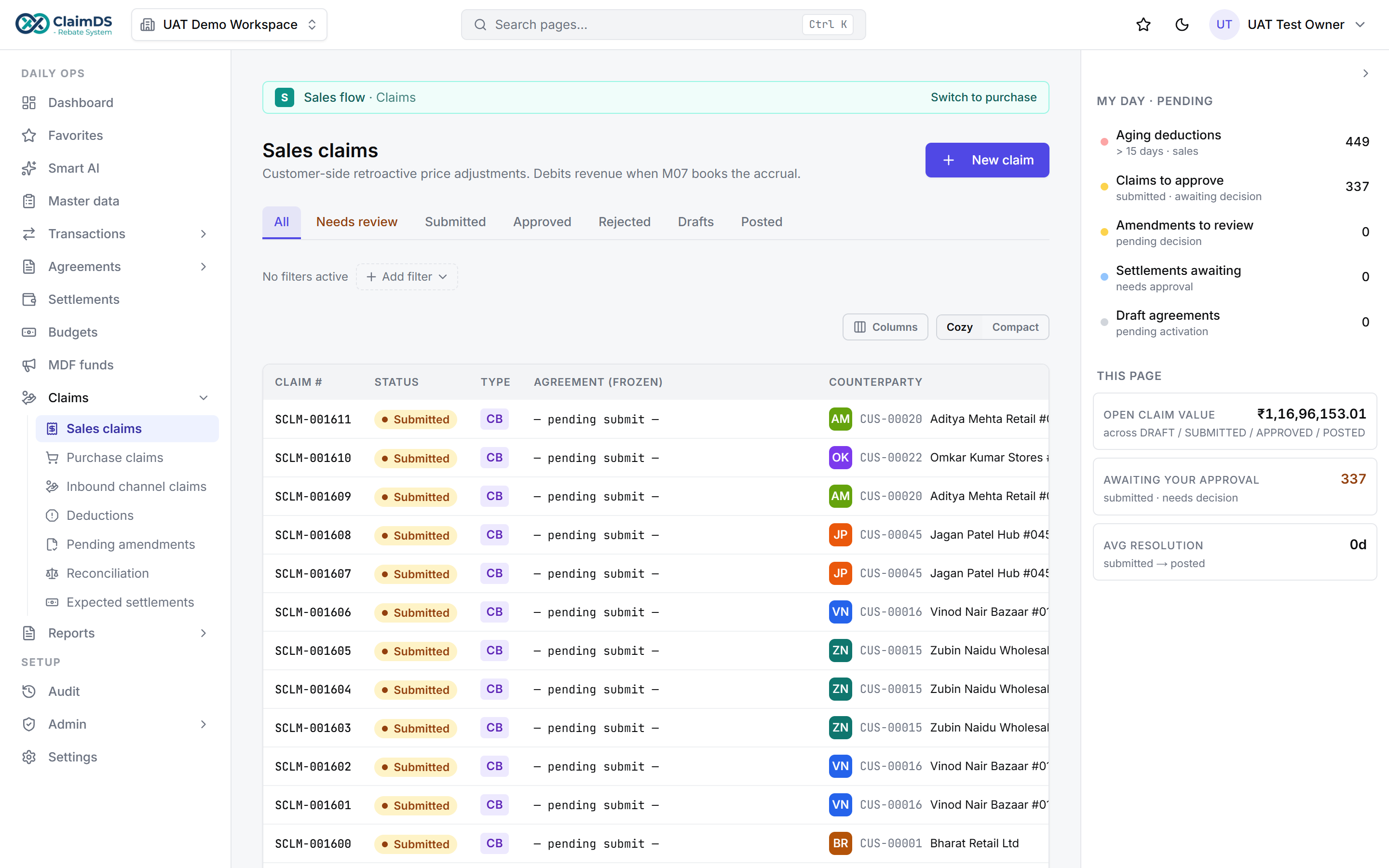

ClaimDS holds each claim against its scheme circular, reconciles the declared stock and liquidation data, flags duplicates and breached caps, and shows claim ageing and status across the agri-input network in one view. <!-- TODO: confirm capability wording with founder -->

Claim ageing and status across the agri-input network, in one view.

Claim ageing and status across the agri-input network, in one view.

The move off spreadsheets is the same one distributors and rebate teams make; the broader case is in distributor claims management, dealer rebate software and incentive management software, and the ERP fit in ERP integration for claims, rebate and TPM software.

See it on your own agri-input claims. Book a demo and we will walk a live seasonal scheme claim and a live liquidation claim through validation, approval and settlement on your data.

Frequently asked questions

How long does an agri-input claim take to settle?

There is no fixed number — it turns on how complete the stock and sell-through data is and how cleanly validation runs against the scheme circular. A claim filed at the season cut-off with a clean liquidation declaration, invoices and the scheme reference moves quickly. A stock mismatch or a claim filed after the window is what stretches settlement into weeks.

What documents does a seasonal scheme claim need?

A seasonal scheme claim carries the scheme circular reference it is filed under, the purchase invoices for the qualifying period, the stock-in-hand declaration at the season cut-off, and sell-through or liquidation data showing what actually moved to farmers. Batch and expiry detail is often required too. Missing the liquidation proof or the cut-off stock statement is what stalls most claims at verification.

Why do agri-input claims get rejected?

The usual reasons are concrete: the claim was filed after the window closed, the declared stock does not match system records, sell-through proof is missing, the wrong season period was claimed, expired stock was claimed as saleable, or the same claim was filed twice. Each has a fix — reconcile the stock, attach the liquidation data, and re-file the eligible portion inside the window.

Is a claim settled by credit note or payment?

In the Indian agri-input channel most dealer and distributor claims are settled by credit note against the party's account rather than by cash, because the claim offsets what the dealer owes and keeps the GST trail clean. Some cases — an exited dealer, or a scheme that specifies a payout — settle by payment. The dealer agreement and scheme circular decide which one applies.

What is a liquidation or sell-through claim?

A liquidation claim rewards the dealer or distributor for stock that actually moved out to retailers or farmers, not just stock bought in. It is validated against secondary sales or sell-through data rather than the purchase invoice alone, because the scheme pays on liquidation. This is what stops the channel from over-buying to book a scheme and then sitting on unsold stock past its shelf life.

Why is the stock declaration at the season cut-off so important?

The cut-off stock declaration is the control the whole seasonal claim rests on, because it fixes what was bought, what liquidated and what remains before the next season's scheme opens. It is also the highest fraud risk — inflated stock inflates the claim. Validation checks the declared figure against system stock and sell-through, so an overstated declaration is caught before it settles rather than clawed back later.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.

Channel Claims and Rebates in Indian Automotive

How claims, incentives and warranty work in the Indian automotive channel — the OEM and dealer network, aftermarket parts, warranty claims and settlement.