Channel Claims and Rebates in Indian Automotive

How claims, incentives and warranty work in the Indian automotive channel — the OEM and dealer network, aftermarket parts, warranty claims and settlement.

In Indian automotive an OEM sells vehicles through a dealer network, and the aftermarket sells parts, tyres and lubricants through distributors to retailers and mechanics. The money flowing back up those two lanes is dealer incentives, warranty reimbursements and scheme claims. What makes automotive claims distinct from other channels is warranty — a technical, evidence-heavy reimbursement — and incentive-in-kind, where non-cash rewards drag Section 194R tax into the settlement. Get those two right and the rest of the channel behaves like any other claims process.

What is the Indian automotive channel, tier by tier?

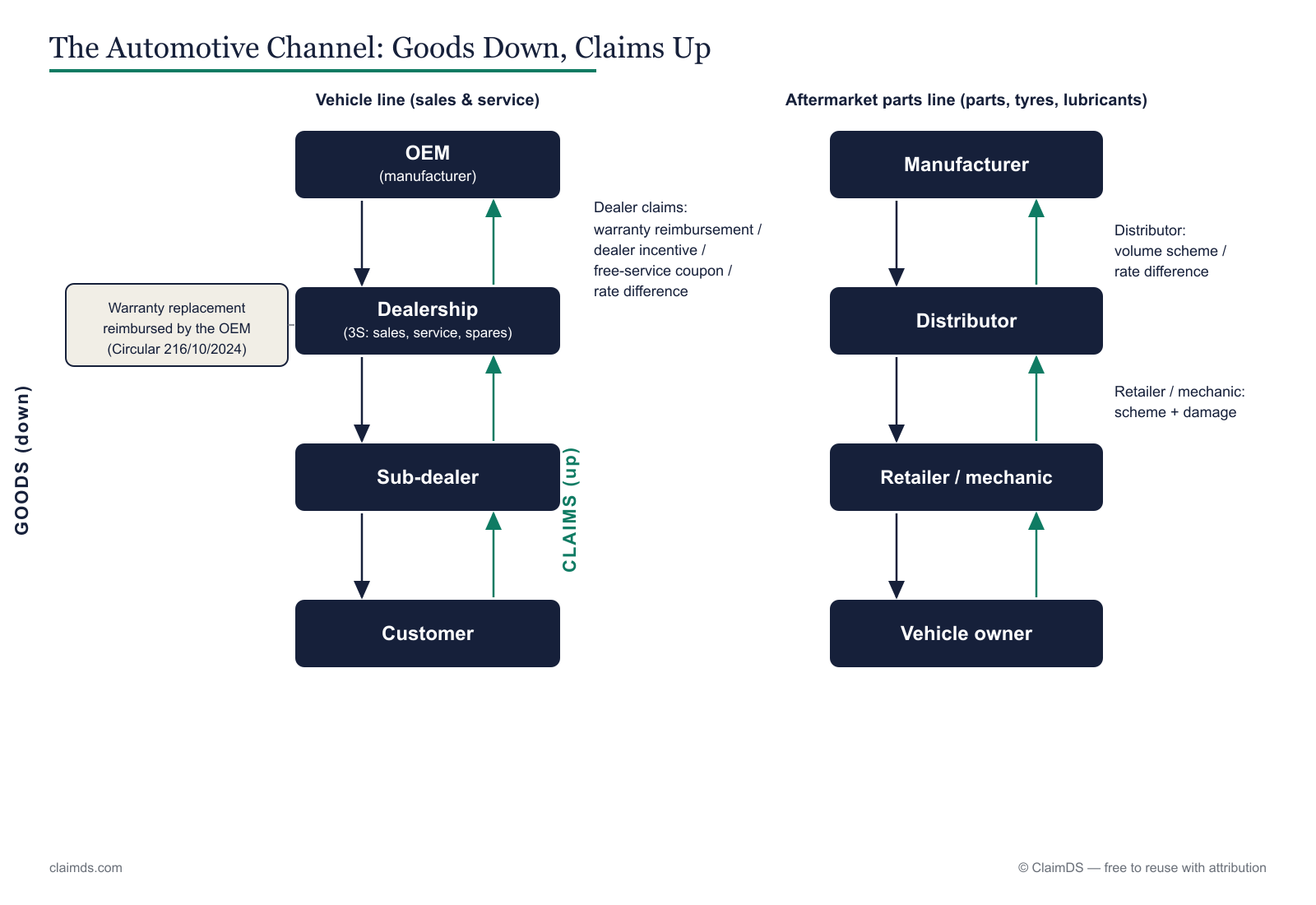

Automotive in India runs on two parallel lanes that meet at the same vehicle. The first is the OEM lane that puts new vehicles on the road; the second is the aftermarket lane that keeps them running. Each tier earns something different and claims it from someone different, so mapping the tiers is the prerequisite for understanding every claim that follows.

In the OEM lane, the OEM (original equipment manufacturer — the vehicle maker) owns the products, declares the incentive schemes, and carries the warranty liability. It sells to an authorised dealer, usually a 3S dealership that handles Sales, Service and Spares under one roof. The dealer is the workhorse of the channel: it buys vehicles and parts, runs a workshop, executes incentive schemes, and files warranty claims on behalf of customers. Below a dealer, a sub-dealer or satellite outlet extends reach into smaller towns, selling and servicing under the parent dealer's appointment. At the base sits the customer — the vehicle owner who buys, services and claims warranty through the dealer.

The aftermarket lane runs alongside it. Here a parts, tyre or lubricant manufacturer sells through a distributor, who redistributes to a retailer or mechanic, who fits the product to a vehicle owner. This lane never touches the vehicle dealership; it is a separate route to market with its own margins, volume schemes and claims. A single garage may buy filters from one distributor, tyres from another and oil from a third, each on its own scheme terms.

| Tier | What it does | What it claims | From whom |

|---|---|---|---|

| OEM | Owns vehicles, declares schemes, carries warranty | Nothing (settles claims) | — |

| Dealer (3S) | Sells, services, stocks spares | Incentives, warranty, free-service, parts margin | OEM |

| Sub-dealer | Extends sales and service reach | Share of incentive, service claims | Dealer / OEM |

| Customer | Owns and runs the vehicle | Warranty repair, free service | Dealer |

| Aftermarket manufacturer | Makes parts, tyres, lubricants | Nothing (settles claims) | — |

| Aftermarket distributor | Redistributes to retail and garages | Volume schemes, margin, rate difference | Manufacturer |

| Retailer / mechanic | Sells and fits parts | Volume benefit, display support | Distributor |

If the distinction between a distributor, a dealer and a super stockist blurs in your own network, the difference between a distributor, dealer and super stockist explainer untangles it, and India's multi-tier channel claim map shows how the tiers connect across industries.

What do automotive companies settle with their channel?

Automotive companies pay their channel through several distinct claim types, and treating them as one bucket is the first mistake most manual processes make. Each has its own evidence, validation rule and settlement path — and each has its own satellite article for the detail.

Dealer incentive schemes are target and volume rewards: sell a defined number of vehicles in a month, cross a value slab, or move a specified model mix, and a per-unit or percentage benefit applies. Because so many of these are paid in kind, they carry a tax wrinkle covered in GST and TDS on automotive dealer incentives.

Warranty claims and reimbursements are the category unique to automotive: the dealer repairs a vehicle free under warranty, absorbs the parts and labour, then claims reimbursement from the OEM against the fault and job-card evidence. The full mechanics live in the automotive warranty claims satellite.

Free-service coupons cover the scheduled services an OEM bundles with a new vehicle. The customer redeems the coupon at the dealer, who performs the service and claims the value back from the OEM — an evidence-and-redemption claim rather than a performance reward.

Spare-parts margin and rate difference protects the dealer's parts business. When an OEM revises parts prices, stock already with the dealer at the old price is reimbursed for the difference — the same protection logic as price protection and rate-difference credit notes under GST.

Aftermarket volume schemes are the buy-side and sell-side incentives that run down the parts, tyre and lubricant lane — quantity slabs, display support and turnover rebates — detailed in automotive spare parts and aftermarket claims. The buy-side mirror, where a company earns rebates from its own suppliers, is in supplier and purchase rebates in automotive India.

What automotive vocabulary will you see on claim forms?

Automotive claim forms are dense with abbreviations, and the same term can mean different things to sales and to service. This table is the quotable glossary — bookmark it, and see the full product glossary for terms beyond the channel.

| Term | What it means |

|---|---|

| OEM | Original equipment manufacturer — the vehicle maker that owns the brand and declares schemes. |

| 3S dealership | A dealer offering Sales, Service and Spares under one roof — the standard full-service format. |

| Sub-dealer | A satellite outlet that sells and services under a parent dealer's appointment. |

| Dealer margin | The dealer's built-in spread between its buy price and the customer price. |

| Dealer incentive | A performance reward paid to the dealer for hitting sales or volume goals. |

| Target incentive | An incentive earned only on reaching a defined sales target in a period. |

| Warranty claim | A dealer's request to be reimbursed for a free repair done under manufacturer warranty. |

| Warranty reimbursement | The parts and labour value the OEM pays back on an approved warranty claim. |

| Extended warranty (AMC) | A paid contract extending cover, or an annual maintenance contract, beyond the standard warranty. |

| Free-service coupon | A bundled voucher a customer redeems for a scheduled service, claimed back by the dealer. |

| PDI | Pre-delivery inspection — the checks a dealer performs before handing over a new vehicle. |

| DLP | Dealer landing price — the net cost to the dealer after discounts, the base for its margin. |

| Spare-parts margin | The dealer's margin on parts sales, protected against OEM price revisions. |

| Aftermarket | The channel supplying parts, tyres and lubricants for vehicles already on the road. |

Why are automotive claims harder than they look?

Automotive claims look like simple arithmetic — a rate times a quantity — but five structural features make them genuinely hard to run at scale. Each carries a consequence that shows up as delay, dispute or leakage.

Warranty settlement has its own GST rule and evidence. A warranty repair is not a normal sale; the part and labour move without a customer invoice, and the tax treatment of a warranty replacement differs from an ordinary supply. Consequence: warranty claims cannot be settled like a discount — they need fault codes, job cards and part returns, and a GST position of their own, as GST on stock transfers and warranty replacements sets out.

Dealer incentives are often benefits in kind. A free trip, an accessory, or gold given as a reward is not cash — but it is still a taxable benefit. Consequence: settlement pulls in Section 194R TDS, so finance must classify each incentive before paying it, per Section 194R TDS on dealer and distributor incentives.

The aftermarket runs a separate multi-tier channel. Parts, tyres and lubricants move through their own distributors and retailers, disconnected from the vehicle dealership. Consequence: a company runs two claim systems at once, and volume data from the aftermarket lane is as hard to see as secondary sales in any other channel.

Claim values range from small parts to a whole vehicle. A wiper-blade warranty and a full-vehicle incentive sit in the same queue with very different stakes. Consequence: a flat approval process either over-scrutinises small claims or waves through large ones — the authority matrix has to flex by value.

Settlement crosses a GST document decision. Every settlement resolves into a credit note, and the choice of note type has tax consequences. Consequence: finance cannot rubber-stamp settlement; it must classify each one — the discipline in financial vs. tax credit notes under GST.

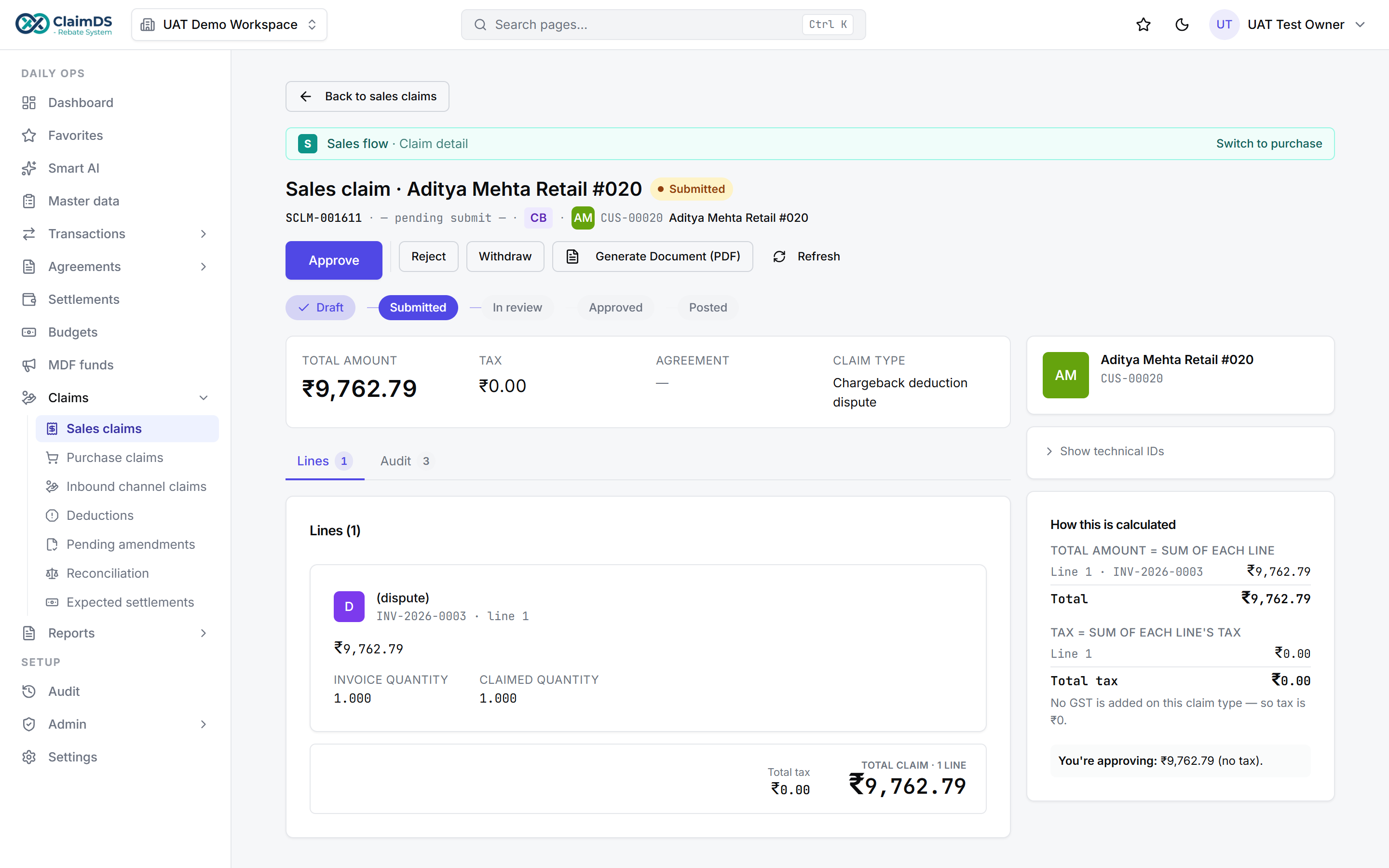

A claim moving through validation and approval before settlement.

How does settlement actually happen?

Settlement turns an approved claim into money — or, more often, into a credit note. The path is consistent even when the claim types are not: a claim is filed with proof, validated against the scheme terms, warranty rules or coupon record, approved by whoever the authority matrix names for its value band, and then settled. The claim process explained walks each stage in depth, and the claim approval workflow covers the routing.

The settlement instrument is almost always a credit note against the dealer's parts or vehicle account, offsetting future purchases rather than moving cash. Here two tax decisions bite. First, the credit-note type: a tax credit note reduces the original GST liability and the dealer's input tax credit, while a financial credit note does not — routed to the GST detail in GST and TDS on automotive dealer incentives. Second, where an incentive is paid in kind, the Section 194R TDS step attaches before the benefit is booked. Keep every credit note referencing its claim, and every claim referencing the scheme, warranty or coupon behind it — an unbroken trail from entitlement to settlement document.

Two habits keep automotive settlement clean. Batch credit notes on a predictable cycle so dealers can reconcile against their own parts and vehicle ledgers rather than chasing individual notes. And settle warranty, incentive and aftermarket claims on their own tracks — they carry different evidence and different tax treatment, so folding them into one run is where mis-classification and part-settlement leakage creep in.

Source: ClaimDS — free to reuse with a link back to this article.

Where should you go next?

This pillar defines the territory; the satellites go deep on each part of it.

- The automotive dealer claim settlement process — the end-to-end journey from filing to credit note, with owners and turnaround.

- Automotive warranty claims — how a free repair becomes a reimbursed claim, and the evidence the OEM demands.

- GST and TDS on automotive dealer incentives — how incentives are taxed, and when 194R and a tax credit note apply.

- Automotive spare parts and aftermarket claims — the separate parts, tyre and lubricant lane and its volume schemes.

- Supplier and purchase rebates in automotive India — the buy-side mirror: rebates a company earns from its own suppliers.

For the tooling behind this — dealer rebate software, dealer claims management software and channel loyalty programs — and the wider picture in channel rebates in India and types of trade schemes in India.

Running incentives, warranty and aftermarket claims across every tier in one place — scheme terms, dealer claims, evidence and GST-ready settlement — is what turns this from a monthly reconciliation scramble into a controlled flow.

<!-- TODO: confirm capability wording with founder -->To see it working on your own dealer network and claim volumes, book a demo.

GST note: This article is general information, not tax or legal advice. Where settlement involves GST credit notes or Section 194R TDS, positions must be re-verified at publish time with a qualified professional.

Frequently asked questions

What is a dealer incentive scheme?

A dealer incentive scheme is a benefit an automotive company offers its dealers to reward sales performance — hitting a monthly target, moving a slow model, or crossing a volume slab. It can be paid as a credit note, a payout, or a benefit in kind such as a free trip. The dealer earns it by meeting the stated terms over a defined period.

What is a warranty claim in automotive?

A warranty claim is a dealer's request to be reimbursed for a repair it carried out free of charge under the manufacturer's warranty. The dealer replaces the defective part and absorbs the labour, then files a claim with the fault details, part numbers and job-card evidence. The manufacturer validates it against warranty terms and reimburses the approved parts and labour.

What is a 3S dealership?

A 3S dealership offers all three core functions under one roof: Sales of vehicles, Service of vehicles, and Spares — the sale of spare parts. It is the standard full-service format for an authorised automotive dealer. Some networks also run 2S outlets that handle only service and spares, or satellite sales points without a workshop.

What is the automotive aftermarket?

The automotive aftermarket is the channel that supplies parts, tyres, lubricants, batteries and accessories for vehicles already on the road, outside the OEM's new-vehicle dealer network. Parts move from a manufacturer through distributors to retailers, garages and mechanics, who fit them to a customer's vehicle. It runs its own volume schemes and claims, separate from the vehicle dealer channel.

Who settles automotive dealer claims?

The automotive company that declared the scheme or issued the warranty settles the claim, usually through its finance or commercial team after the claim passes validation and approval. Dealers file claims upward; the company checks them against scheme terms, warranty rules and evidence, then issues settlement — most often as a credit note against the dealer's parts or vehicle account.

What is Section 194R for dealers?

Section 194R of the Income-tax Act requires the deduction of TDS on benefits or perquisites a business gives, including many dealer incentives paid in kind — free foreign trips, gold coins, or goods given as a reward. It matters in automotive because incentives are often non-cash, which brings them into the 194R net and adds a tax step to settlement.

How are automotive claims settled — credit note or reimbursement?

Most automotive dealer claims settle by credit note against the dealer's account, offsetting future vehicle or parts purchases rather than moving cash. Warranty claims are a reimbursement of the parts and labour the dealer already spent, also usually issued as a credit. The GST document choice — tax credit note versus financial credit note — decides the input-tax-credit effect.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.