Channel Rebates in India: How Scheme Settlement Works

What a channel rebate is and how multi-tier scheme and claim settlement works in India — credit notes, secondary schemes and the vocabulary that differs.

A channel rebate is money a manufacturer pays back to its distribution channel for hitting agreed targets or performing agreed activities. In India these are usually called schemes and claims, and they settle through credit notes rather than rebate cheques — netted against the partner's account instead of paid out separately. If you are new to the underlying idea, start with what a rebate is.

What is a channel rebate?

A channel rebate is an incentive a manufacturer or brand owner pays to the partners who move its product to market — distributors, dealers, stockists and retailers. Instead of cutting the list price for everyone, the company keeps the invoice price firm and returns value after the partner performs: buys a target volume, stocks a full range, sells through to the next tier, or runs a branding activity.

That "pay back after performance" shape is what separates a rebate from a plain discount. A discount reduces the price at the moment of sale; a rebate is earned over a period against agreed rules and settled later. Because the payout is conditional and retrospective, someone has to track the target, gather the proof, validate the claim and issue the settlement — which is the entire discipline of rebate management software.

In Western usage the word rebate covers this whole family, from volume rebates to customer rebates to supplier rebates. Indian trade rarely uses the word at all. The same money is called a scheme when it is offered and a claim when it is recovered. The vocabulary gap is not cosmetic — it changes how finance teams search, file and reconcile. Our rebate meanings explained guide maps the overlapping terms, and the glossary keeps the definitions in one place.

How channel rebates work, step by step

Strip away the local vocabulary and every channel rebate runs through the same five stages.

1. Define the scheme. The company sets the terms — a target (say ₹10 lakh of quarterly purchases), a qualifying period, the eligible products, and the reward (a percentage, a slab, or free goods). The clearer the rule, the cleaner the eventual settlement. The types of trade schemes used in India show how varied these terms get.

2. Communicate it to the channel. Distributors and dealers are told what they must do to earn the payout. In a multi-tier network this cascades down several levels, which is where ambiguity — and disputes — creep in.

3. Perform and accrue. The partner buys or sells under the terms. On the company side, finance should accrue the expected liability as sales happen, so the payout is provisioned rather than a quarter-end surprise. Getting this provisioning right is the heart of clean supplier rebate accrual.

4. Claim and validate. The partner files a claim with supporting data — purchase records, secondary-sales reports, proof of activity. Finance checks it against the scheme rules and the accrued amount, and queries anything that does not reconcile.

5. Settle. The approved amount is paid out. In India this is almost always a credit note that reduces the partner's outstanding balance, not a separate cheque — a point the next section returns to. For a worked end-to-end example, see how distributor claims are managed.

The step most teams underestimate is the fourth. A scheme with loose rules generates claims that cannot be validated cleanly, and every ambiguous claim becomes a phone call, an email chain, or a write-off. Building a repeatable claim and rebate approval workflow — with the accrual, the claim and the settlement reconciled against one another — is what turns rebates from a quarter-end fire drill into routine finance. Where the settlement adjusts GST, the credit note also has to reconcile back to the return, which is why GST adjustments on channel settlements sit inside the same workflow rather than beside it.

Why India is different

The generic mechanism above is universal. What changes in India is the shape of the channel and the instrument of settlement. Three differences matter most.

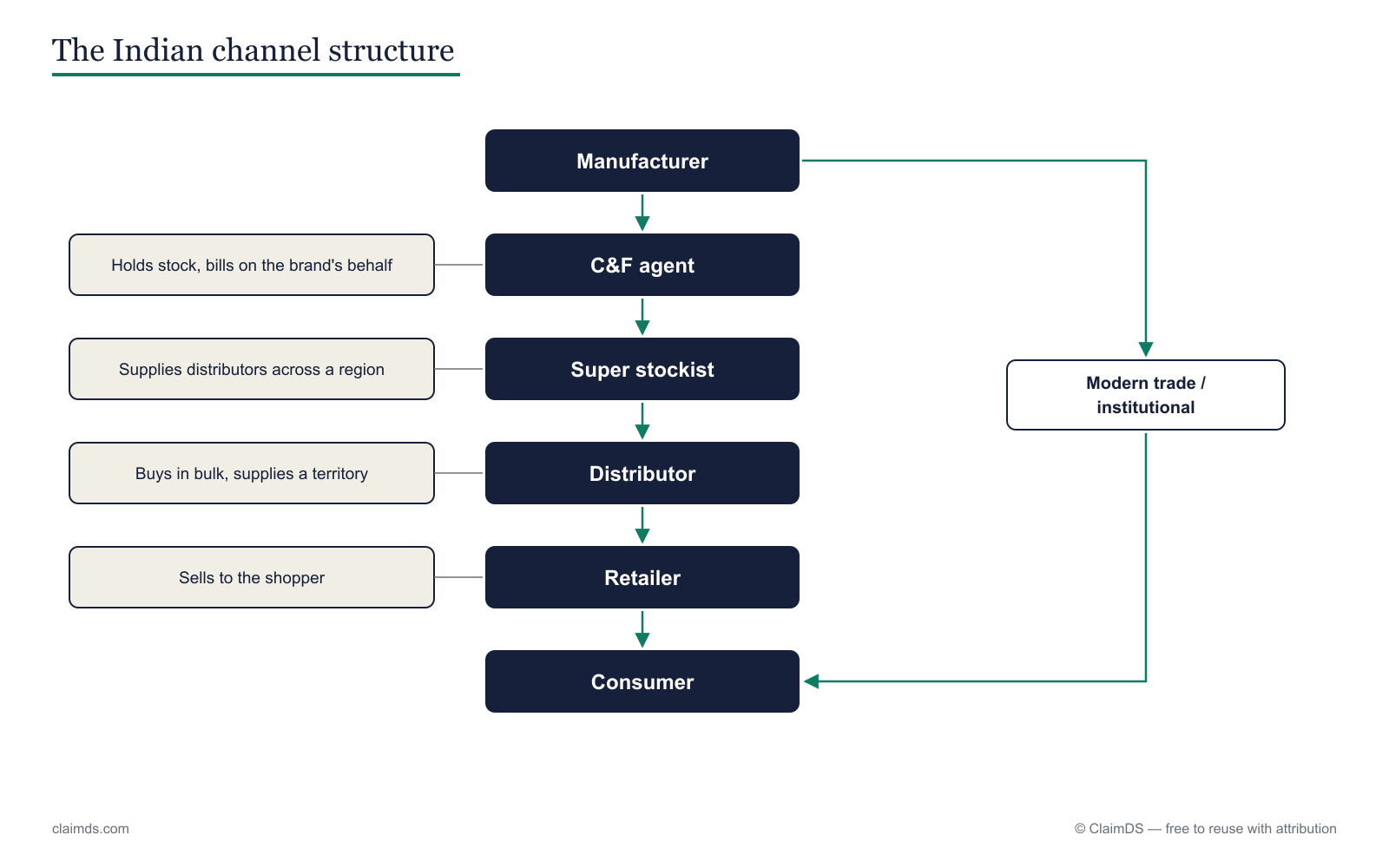

India's channel runs deeper than the Western vendor-distributor-reseller model — and rebates settle by credit note, not cheque.

India's channel runs deeper than the Western vendor-distributor-reseller model — and rebates settle by credit note, not cheque.

(a) Tier depth. A Western channel is often three links: vendor → distributor → reseller. The Indian channel runs far deeper — brand → C&F (carrying-and-forwarding) agent → super stockist → distributor → wholesaler → dealer → retailer. Each extra tier is another place a scheme can be offered, another margin to protect, and another claim to reconcile. Sorting out who sits where is a job in itself, covered in distributor vs dealer vs super stockist.

(b) Settlement by GST credit note. In the West, a rebate is frequently a payment — a cheque or transfer. In India it is settled through a credit note that nets against the partner's ledger, and the credit note itself comes in two flavours with very different tax effects. A tax credit note under Section 34 of the CGST Act reduces the supplier's output tax and forces the recipient to reverse input tax credit; a financial (commercial) credit note does neither. Choosing wrong creates real exposure at assessment — the mechanics are unpacked in financial vs tax credit notes under GST.

(c) Secondary schemes. The sharpest India-only wrinkle. A secondary scheme rewards the sale from the distributor down to retailers rather than the distributor's own purchase. The distributor funds the discount at the counter out of its own pocket, then claims it back from the company. There is no clean Western equivalent, because it depends on secondary-sales data the company cannot see directly — the distributor is both the party being incentivised and the source of the proof. Understanding the primary, secondary and tertiary sales split is a prerequisite, and secondary scheme settlement walks through the validation problem.

| Dimension | Western channel | Indian channel |

|---|---|---|

| Tier depth | Vendor → distributor → reseller (flat) | Brand → C&F → super stockist → distributor → wholesaler → dealer → retailer (deep) |

| Settlement instrument | Rebate payment (cheque or transfer) | GST credit note netted against the ledger — financial or tax |

| Distinctive scheme | Volume and growth rebates | Secondary schemes — distributor funds the discount, then claims it back |

The combined effect is that an Indian channel-finance team is reconciling more tiers, through a tax instrument, on data it does not fully own. A single quarter can carry primary purchase schemes at the distributor level, secondary sell-through schemes at the retailer level, and branding support layered on top — each with its own proof, its own credit note, and its own GST treatment. That is exactly the problem ClaimDS is built for, and the multi-tier channel claim map shows the full route-to-market view. The breadth of scheme types alone — from slab-based volume deals to display and range incentives — is set out in FMCG trade schemes explained.

The vocabulary map

Most confusion in cross-border trade finance is a translation problem, not a concept problem. The mechanics of a rebate and a scheme are the same; the words differ. This table is the single most useful thing to keep on hand when a global playbook meets an Indian channel.

| Western term | What Indian trade actually says |

|---|---|

| Rebate | Scheme (when offered) / claim (when recovered) |

| Rebate accrual | Scheme provision |

| Deduction | Short payment / claim netting |

| MDF (market development funds) | Dealer board / branding support |

| Ship-and-debit | Rate difference |

Read the table both ways. A CFO reading a global rebate policy needs to know that "rebate accrual" is what the local team files under "scheme provision," and that a Western "deduction" is what the ledger shows as a "short payment." An Indian finance manager reading a vendor's contract needs the reverse. Getting the mapping wrong means schemes go unaccrued, short payments go uninvestigated, and branding spend is booked in the wrong place.

The trickiest pairing is the last one. "Ship-and-debit" and "rate difference" both describe the same event — a distributor sells below the price it bought at, on the company's instruction, and reclaims the gap — but a team that only knows one label will not recognise the other in a claim file. The same is true of MDF: what a global playbook calls market development funds, the Indian trade books as a dealer board or branding support, and it settles as its own credit note. The rebate meanings explained guide and the glossary expand each pairing, and the rebate concept reference anchors the base definition.

Channel rebates by industry

The rules bend again by sector — expiry and damage claims dominate one vertical, warranty and price protection another. Explore the vertical pillars:

- FMCG — channel claims and rebates in Indian FMCG, covering QPS, secondary schemes and damage-and-expiry claims.

- Pharma — channel claims and rebates in Indian pharma, covering the CFA and stockist channel, expiry and breakage returns, and their GST treatment.

- Automotive — channel claims and rebates in Indian automotive, covering the OEM and dealer network, warranty claims, dealer incentives and the aftermarket.

- Consumer electronics — channel claims and rebates in consumer electronics, covering price protection through fast price cuts, QPS schemes and DOA and warranty returns.

- Paints — channel claims and rebates in Indian paints, covering the dealer network, rate-difference and damage claims, and painter and contractor loyalty rewards.

- Agri-inputs — channel claims and rebates in Indian agri-inputs, covering the season-driven fertilizer and crop-protection channel, liquidation schemes and near-expiry returns.

- Building materials, tyres and lubricants — dealer boards and volume slabs. <!-- TODO: link when built -->

Bringing it together

Channel rebates in India are the same idea as anywhere — pay the channel for performance — wrapped in a deeper route-to-market, a credit-note settlement, and a secondary-scheme layer with no Western twin. Get the vocabulary, the tier map and the credit-note choice right, and the reconciliation gets dramatically simpler. See how ClaimDS handles distributor claim settlement and rebate management end to end, or book a demo to walk through your own channel.

Frequently asked questions

What is a channel rebate?

A channel rebate is money a manufacturer pays back to its distribution channel — distributors, dealers and retailers — for hitting agreed sales targets or performing agreed activities. In India these are usually called schemes and claims, and they are settled through credit notes rather than rebate cheques, netted against the partner's outstanding account.

How do channel rebates work?

A company sets a scheme with a target, a qualifying period and a reward — say two percent on quarterly purchases above a threshold. The channel partner buys or sells under those terms, then files a claim with supporting data. Finance validates it against the agreed rules and settles the approved amount by issuing a credit note.

What is the difference between a channel rebate and a trade scheme?

They describe the same money from different angles. Channel rebate is the Western category term for a target-linked payout to the channel; trade scheme is what Indian trade actually calls it. A scheme is the offer and its rules, the rebate is the earned amount. In practice, Indian teams say scheme or claim, not rebate.

How are channel rebates settled in India?

Settlement almost never happens by cheque. The company issues a credit note that reduces the channel partner's outstanding balance, and the claim is netted against future invoices. The credit note may be a GST tax credit note or a purely financial one, depending on whether output tax is being adjusted — a distinction with real compliance consequences.

What is a secondary scheme?

A secondary scheme rewards the sale from the distributor down to retailers — the secondary sale — rather than the distributor's own purchase from the company. The distributor funds the retailer discount at the counter, then claims it back from the company. Because it rests on data the company cannot see directly, it is the hardest scheme type to validate.

Are channel rebates taxable?

Tax treatment depends on how the credit note is structured under GST — whether it is a Section 34 tax credit note or a financial credit note — and on income-tax rules such as TDS under Section 194R. See our guide on financial versus tax credit notes under GST for the mechanics, and confirm with your tax advisor.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Supplier and Purchase Rebates in Agri-Inputs

How Indian agri-input makers treat money from raw-material and packaging suppliers — turnover and cash discounts under Ind AS 2 and GST credit notes.

Supplier and Purchase Rebates in Automotive

How Indian automotive treats money received from component and material suppliers — turnover and cash discounts under Ind AS 2 and GST credit notes.

Supplier and Purchase Rebates in Electronics

How Indian electronics makers treat money received from component and packaging suppliers — turnover, cash discounts under Ind AS 2 and GST credit notes.