Channel Claims and Rebates in Indian FMCG

How claims, schemes and rebates work in Indian FMCG — the multi-tier channel, QPS and secondary schemes, damage and expiry claims, and settlement.

In Indian FMCG the manufacturer sells to a distributor — the primary sale — and the distributor sells onward to retailers, the secondary sale. Most trade schemes are earned on that secondary sale, which the manufacturer never sees directly. The distributor funds a discount at the counter, then files a claim to recover it. The gap between what a scheme promised and what a claim finally settles is where FMCG channel money quietly leaks — and closing it is a data-and-evidence problem before it is a finance one.

What is the Indian FMCG channel, tier by tier?

Indian FMCG rarely moves in a straight line from factory to shopper. It passes through a layered distribution channel, and each layer earns something different and claims it from someone different. Understanding who sits where is the prerequisite for understanding every claim that follows.

At the top, the manufacturer (the FMCG company or brand) owns the products, declares the schemes, and carries the ultimate liability for every claim. It usually does not ship directly. Instead it appoints a C&F agent (carrying and forwarding agent) — a logistics partner who holds stock in a depot on the company's behalf and dispatches against orders, working on a fee rather than owning the goods.

Below the C&F, a super stockist buys stock and redistributes it across a wide geography to smaller distributors, typically in markets too dispersed for the company to service directly. The distributor (also called a stockist) is the workhorse of the channel: it buys from the company or super stockist, maintains a beat of retail outlets, and executes most schemes at the retail counter. In some categories a wholesaler sits alongside or below the distributor, buying in bulk and selling on to smaller retailers at thin margins.

At the base is the retailer — from an organised modern trade outlet to the neighbourhood kirana store that still accounts for the bulk of Indian FMCG volume. This distinction matters: general trade (kirana, wholesale, traditional counters) runs on distributor-funded schemes and manual claims, while modern trade (supermarkets, large-format retail) negotiates its own terms directly with the company and claims through structured billing.

| Tier | What it does | What it claims | From whom |

|---|---|---|---|

| Manufacturer | Owns brands, declares schemes | Nothing (settles claims) | — |

| C&F agent | Holds and dispatches stock | Handling and freight fees | Manufacturer |

| Super stockist | Redistributes across geography | Margin, QPS, secondary schemes | Manufacturer |

| Distributor | Services retail beat, funds schemes | Trade schemes, L&D, price-drop | Company / super stockist |

| Wholesaler | Bulk resale to small retail | Volume and cash discounts | Distributor / company |

| Retailer / kirana | Sells to shopper | Display, secondary scheme benefit | Distributor |

The difference between a distributor, dealer and super stockist is worth reading in full if these roles blur together in your own channel.

What do FMCG companies pay their channel?

FMCG companies pay their channel through several distinct claim types, and lumping them together is the first mistake most manual processes make. Each has its own evidence, its own validation rule, and its own settlement path.

Trade schemes are the largest bucket: time-bound incentives to buy, stock or sell more — quantity purchase schemes, slab schemes, target schemes and the rest. Because there are so many variants, they get their own deep dive in the FMCG trade schemes explained satellite, and a broader taxonomy in types of trade schemes in India.

Damage and expiry (L&D) claims cover stock that is broken, leaked or has reached expiry unsold. These are not performance rewards; they are reimbursements for a loss the channel absorbed on the company's behalf. Evidence is physical — photographs, batch numbers, expiry dates — and settlement often includes destruction certificates.

Display and visibility payments reward retailers and distributors for executing merchandising — a branded shelf, a gondola end, a window board. The claim rests on proof of execution, usually a dated photograph tied to an outlet, and increasingly on geo-tagged app captures.

Price-drop and rate-difference claims protect the channel when a company cuts its list price. Stock already sitting with a distributor at the old price would otherwise lose margin overnight, so the company reimburses the difference on documented closing stock — the same protection logic covered in the price-protection literature.

Secondary-scheme reimbursement is the structurally hardest category: the distributor gives a retailer a discount that the company promised, funds it from its own working capital, and then claims it back. Because it depends on secondary-sales data the company cannot independently see, it drives most claim disputes — the mechanics are in secondary scheme settlement.

Two more payments round out the picture. Cash discounts (CD) reward prompt payment against an invoice, and turnover discounts (TOD) are paid in arrears on a partner's total volume over a period — both are earned on the primary sale, so they are the easiest to validate and the least disputed. The pattern holds across the taxonomy: the closer a payment sits to the company's own invoice, the cleaner the claim; the further down the tiers it is earned, the harder it is to prove.

What FMCG vocabulary will you see on claim forms?

FMCG claim forms are dense with abbreviations, and the same word can mean different things to sales and to finance. This table is the quotable glossary — bookmark it, and see the full product glossary for terms beyond the channel.

| Term | What it means |

|---|---|

| QPS | Quantity purchase scheme — a benefit earned by buying a defined quantity in a defined window. A primary-sale scheme. |

| Slab scheme | A tiered incentive where the rate rises as purchase or sales volume crosses defined thresholds (slabs). |

| Secondary scheme | An incentive earned on the distributor-to-retailer sale, funded by the distributor and claimed back from the company. |

| Primary sales | The company's sales to its distributors — invoiced and directly visible to the company. |

| Secondary sales | The distributor's onward sales to retailers — the basis of most schemes, not directly visible to the company. |

| Tertiary sales | The retailer's sales to the end shopper — the deepest and least visible tier. |

| DLP | Distributor landing price — the net cost to the distributor after discounts, the base for its margin. |

| RLP | Retailer landing price — the net cost to the retailer, the base for retail margin. |

| ROI | Return on investment — the distributor's return on the capital it deploys to run the business. |

| Beat | A fixed route of retail outlets a salesperson covers on a set day of the week. |

| L&D | Loss and damage — a claim for broken, leaked or expired stock. |

| CD | Cash discount — a discount for early or prompt payment against an invoice. |

| TOD | Turnover discount — a rebate paid on total turnover over a period, usually paid in arrears. |

The three sales tiers underpin almost every dispute, so the dedicated explainer on primary, secondary and tertiary sales is the companion to this table.

Why are FMCG claims harder than they look?

FMCG claims look like simple arithmetic — a rate times a quantity — but five structural features make them genuinely hard to run at scale. Each carries a consequence that shows up as delay, dispute or leakage.

Secondary data lives in the distributor's books, not the company's. The company sells to the distributor and sees that invoice; the sale that earns the scheme happens one tier down, in the distributor's own sales records. Consequence: the company must trust, sample or integrate distributor data it does not control, and every scheme becomes a reconciliation exercise.

Schemes stack. A single case can carry a QPS benefit, a slab uplift, a secondary scheme and a cash discount at once, applied in a specific order. Consequence: a claim is rarely one calculation — it is several interacting ones, and getting the order wrong changes the answer, as the calculation of FMCG distributor claims shows.

Evidence is photos and paper. Display claims need dated images; L&D claims need batch photos and destruction proof; secondary claims need retailer-level sales sheets. Consequence: validation is a document-matching task at volume, and missing or mismatched evidence is the single biggest reason claims stall.

High volume, small values. A large distributor network generates thousands of claims a month, most worth a few thousand rupees each. Consequence: no single claim justifies deep manual scrutiny, so errors and duplicates slip through — the mechanism behind revenue leakage in rebate programs.

Settlement crosses a GST document decision. Every settlement resolves into a credit note, and the choice of note type has tax consequences. Consequence: finance cannot rubber-stamp settlement; it must classify each one — the discipline in deduction management best practices and the chargebacks in FMCG distribution playbook.

Scheme definitions and their claim rules, held in one place.

How does settlement actually happen?

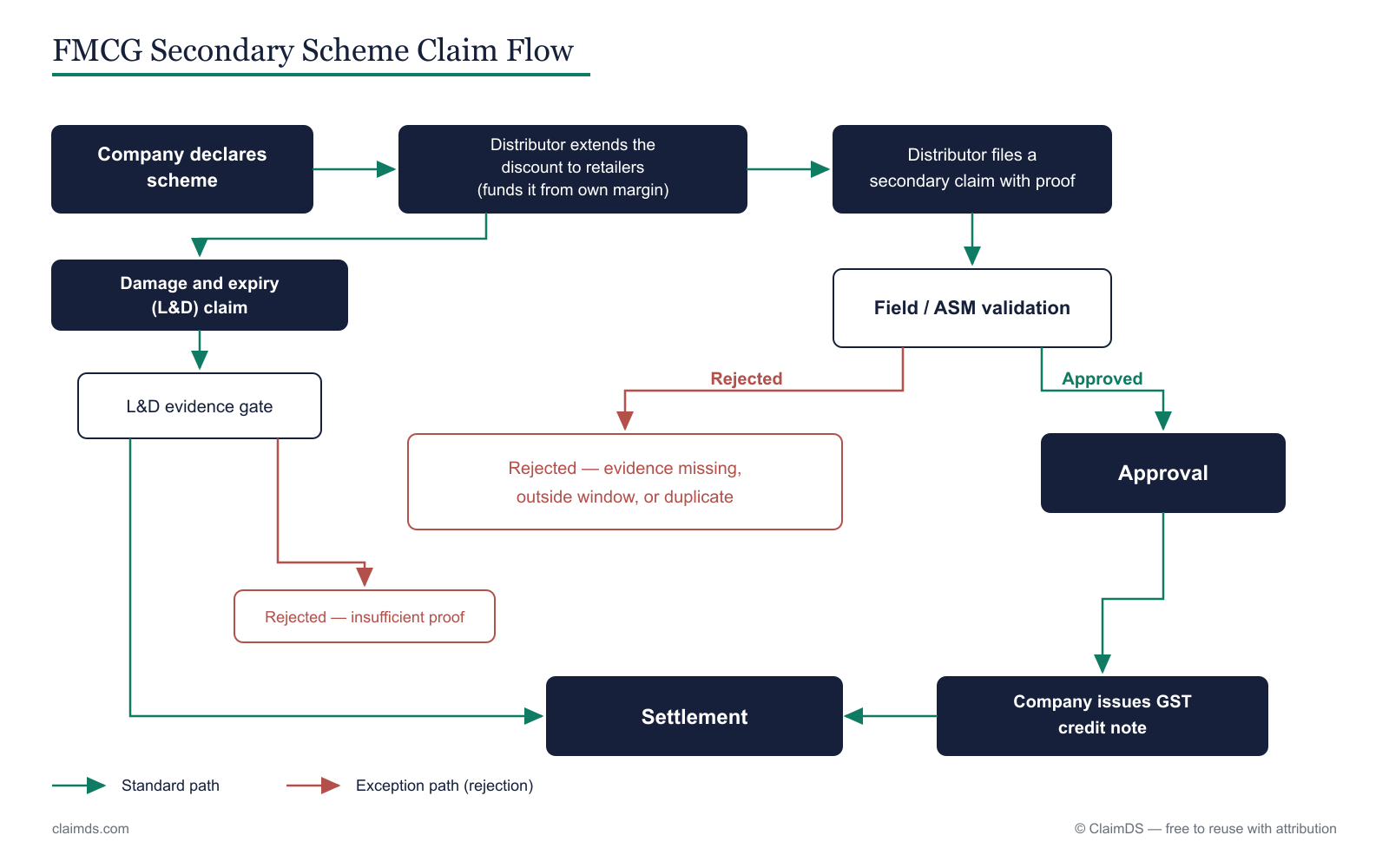

Settlement turns an approved claim into money — or, more often, into a credit note. The path is consistent even when the scheme types are not: a claim is filed with proof, validated against the scheme terms and the underlying data, approved by whoever the authority matrix names for its value band, and then settled. The claim process explained walks each stage in depth, and the claim approval workflow covers the routing.

The settlement instrument is almost always a credit note against the partner's account, offsetting future purchases rather than moving cash. Here the tax decision bites: a tax credit note reduces the original GST liability and the recipient's input tax credit, while a financial credit note does not — the full treatment sits in the GST treatment of FMCG claims and schemes satellite and in financial vs. tax credit notes under GST.

Two habits keep settlement clean. First, batch credit notes on a predictable cycle so partners can reconcile against their own books rather than chasing individual notes. Second, make every note reference the claim, and every claim reference the scheme and invoices behind it — an unbroken trail from scheme terms to settlement document. Where that trail breaks, part-settlements go unrecorded and the balance quietly disappears, which is exactly the leak the whole process exists to close.

Source: ClaimDS — free to reuse with a link back to this article.

A claim moving through validation and approval before settlement.

Where should you go next?

This pillar defines the territory; the satellites go deep on each part of it.

- FMCG trade schemes explained — every scheme type, from QPS and slab to target and secondary, with worked examples.

- The FMCG claim settlement process — the end-to-end claim journey from filing to credit note, with owners and turnaround.

- GST treatment of FMCG claims and schemes — how schemes, discounts and claims are treated under GST, and when a tax credit note applies.

- Supplier and purchase rebates in FMCG India — the buy-side mirror: rebates a company earns from its own suppliers.

For the broader picture beyond FMCG, see channel rebates in India.

Running claims and schemes across every tier in one place — scheme terms, distributor claims, evidence and settlement — is what turns this from a monthly reconciliation scramble into a controlled flow.

<!-- TODO: confirm capability wording with founder -->To see it working on your own scheme types and claim volumes, book a demo.

GST note: This article is general information, not tax or legal advice. Where settlement involves GST credit notes, positions must be re-verified at publish time with a qualified professional.

Frequently asked questions

What is a trade scheme in FMCG?

A trade scheme is an incentive an FMCG company offers its channel to push volume, stock a range or hit a target — a discount, free goods, or a rebate paid after the fact. Schemes run for a defined period on defined products, and the channel partner earns them by selling or buying under the stated terms.

What is a secondary scheme?

A secondary scheme rewards the sale from the distributor down to retailers — the secondary sale — rather than the distributor's own purchase. The distributor funds the retailer discount at the counter, then files a claim to recover it from the company. Because it rests on data the company cannot see directly, it is the hardest scheme type to validate.

What is a QPS scheme?

QPS stands for quantity purchase scheme: an incentive earned by buying a defined quantity within a defined window. Buy a target number of cases or cross a value slab and a per-unit or percentage benefit applies. QPS is a primary-sale scheme, so the company can validate it against its own dispatch and invoice records.

What is an L&D claim?

L&D means loss and damage: a claim a distributor raises for stock that arrived broken, leaked, or reached its expiry date unsold. The distributor documents the affected units with photos and batch details, and the company settles by credit note or replacement. L&D is an evidence-heavy claim, distinct from a performance-based trade scheme.

What is the difference between primary and secondary sales?

Primary sales are the company's sales to its distributors — the invoice the company raises and can see. Secondary sales are the distributor's onward sales to retailers. Most trade schemes are earned on secondary sales, which is why the data gap between the two tiers is where FMCG claim disputes concentrate.

Who settles FMCG distributor claims?

The company that declared the scheme settles the claim, usually through its finance or commercial team, after the claim passes validation and approval. Distributors and super stockists file claims upward; the company validates them against scheme terms and evidence, then issues settlement. Some companies route settlement through a C&F agent, but the liability stays with the company.

How are FMCG claims settled — credit note or payment?

Most FMCG channel claims settle by credit note against the partner's account, which offsets future purchases rather than moving cash. Under GST the choice between a tax credit note and a financial credit note affects input tax credit, so the instrument matters. Loss-and-damage and some one-off claims may settle by payout, but the credit note is the default.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.