Supplier and Purchase Rebates in Indian FMCG

How Indian FMCG treats money received from suppliers — turnover discounts, cash discounts and target incentives — under Ind AS 2 and GST credit notes.

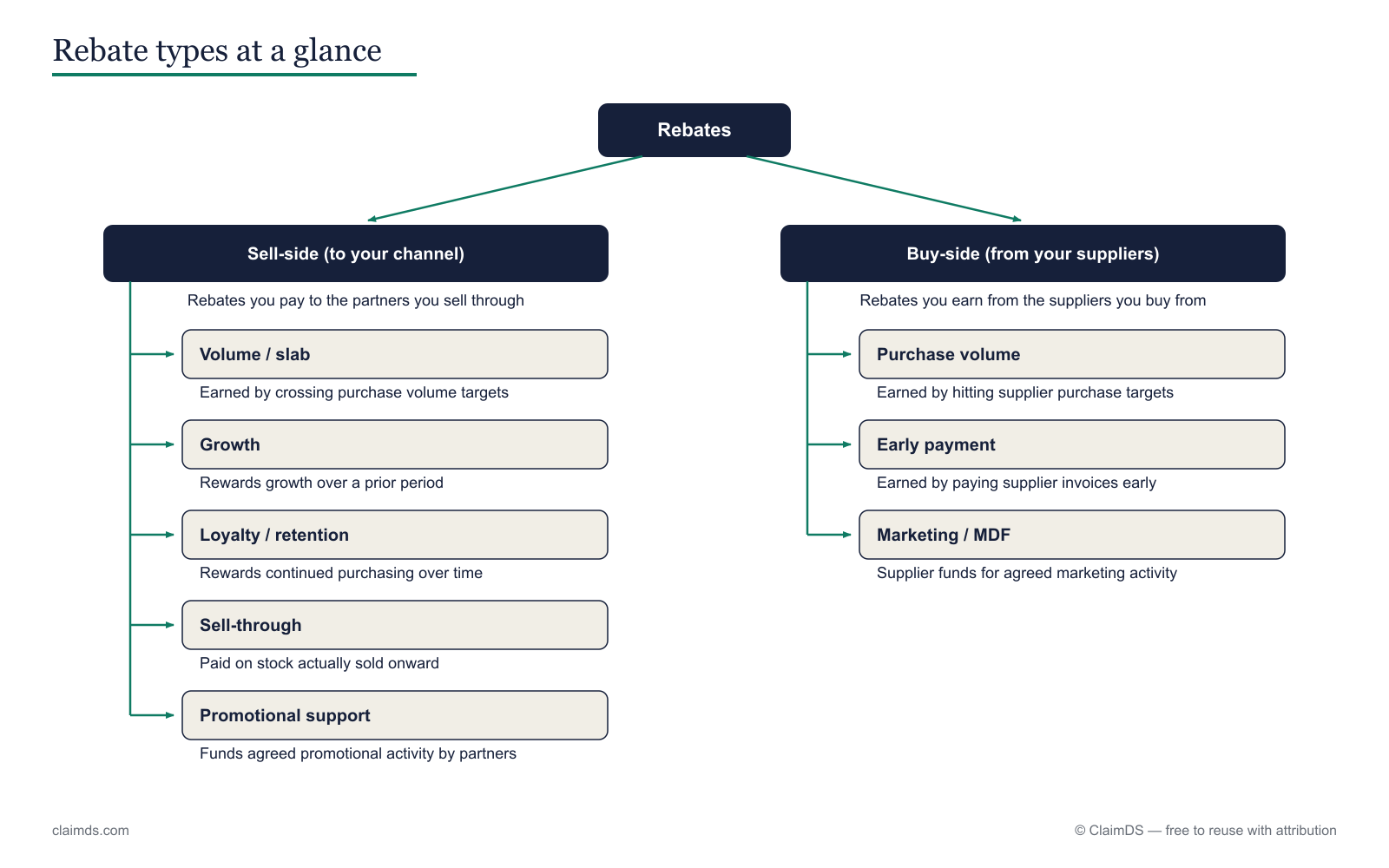

An Indian FMCG maker does not only pay its channel — it also receives money from the suppliers it buys from: raw-material vendors, packaging converters and co-packers who reward volume, prompt payment and annual targets. Every tier does the same, earning something from the tier above it. That money received is the buy-side mirror of the schemes a company pays down its channel. But its accounting and GST treatment differ sharply from money paid — because a rebate you earn reduces what your stock cost you, not what you sold.

What do Indian buyers actually call supplier rebates?

Indian trade has its own words for money received from a supplier, and none of them is supplier rebate. The dominant term is the turnover discount (TOD) — a rebate credited on your total purchase turnover from a vendor over a quarter or a year, settled in arrears once a slab is crossed. Next is the cash discount (CD), earned for paying an invoice early or within stated terms. A target purchase incentive — often just called a scheme — rewards hitting an agreed volume or value of purchases in a window. When the money is finally released, the paperwork is a claim the buyer raises and a credit note the supplier issues against it.

Name the English equivalents once, for anyone searching in English: a TOD is a purchase volume rebate or supplier rebate, a target purchase incentive is a vendor incentive, and the whole family is buy-side rebates. From here on this article uses the Indian words, because those are the words on the actual claim form, the ledger narration and the vendor agreement. If you formalise these terms with your vendors, the structure of a supplier rebate agreement is the place to start.

Who claims what from whom?

Buy-side rebates are earned from the suppliers you buy from — the mirror of the sell-side schemes you pay your channel.

Every tier in the Indian channel both pays rebates downward and earns them upward, and the direction decides the treatment. A retailer earns secondary-scheme benefit, display money and turnover discounts from the distributor it buys from. The distributor, in turn, claims trade schemes, price-drop protection and TOD from the company or its C&F agent. The company — the tier everyone else claims from — is not only a payer: it buys raw material, packaging and contract-manufacturing (co-packing) services, and it earns TOD, CD and target purchase incentives from those suppliers. Even a super stockist earns margin from the company while paying schemes to the distributors below it. The full channel tier map sets out the sell-side view in depth; this article is its buy-side mirror, and what a supplier rebate is at its core holds whichever tier earns it.

The single rule to hold on to: the same rupee is a cost reduction to whoever earns it and a trade-spend expense to whoever pays it — which is why where a partner sits in the channel decides which side of the ledger a claim lands on.

| Tier | Earns from upstream (buy-side) | Pays downstream (sell-side) |

|---|---|---|

| FMCG company | TOD, CD, target purchase incentive from material, packaging and co-packing suppliers | Trade schemes, L&D, price-drop to the channel |

| Super stockist | Margin, QPS from the company | Secondary schemes to distributors |

| Distributor | Trade schemes, TOD, price-drop from company / C&F | Secondary-scheme discount to retailers |

| Retailer / kirana | Secondary benefit, display, TOD from the distributor | — (sells to shopper) |

How are rebates received treated in the accounts?

<!-- TODO CA REVIEW: Ind AS 2 treatment — reviewer to confirm and cite the MCA-notified standard text; do not publish this section unreviewed -->Here is where money received parts company from money paid. Under Ind AS 2, the standard on inventories, the cost of purchase is measured net of trade discounts and rebates received — they are deducted in arriving at what the inventory cost you. A turnover discount or target purchase incentive earned on the raw material and packaging you buy is therefore, as a general rule, not other income. It reduces the carrying cost of that inventory, and it flows through to cost of goods sold as the stock is consumed and sold.

The practical consequences are easy to underestimate. First, closing-stock valuation: rebates attributable to stock still on hand at period-end must be carried against that stock, not swept to the P&L, or closing inventory is overstated. Second, margin optics: booking supplier rebates as other income flatters the revenue line and understates gross margin, which misleads anyone reading the accounts. Third, matching: a TOD accrued but not yet credited still reduces cost in the period the purchases fall, so the accrual has to be estimated and carried — the same discipline set out in how rebate accruals work, calculating supplier rebate accruals and the wider rebate accrual management playbook.

Because the standard's exact wording and its edge cases — a volume rebate spanning stock that is partly sold and partly on hand — drive real audit adjustments, this section is marked for chartered-accountant review before publication. Treat the principle above as general guidance, not a substitute for applying the MCA-notified text to your own facts.

What does the buyer do with a supplier credit note under GST?

<!-- TODO VERIFY AT PUBLISH + CA REVIEW -->When a supplier releases a TOD, CD or target incentive, it does so through a credit note — and the type of credit note decides whether GST moves at all. A Section 34 tax credit note, issued by the supplier to reduce the taxable value and the GST originally charged, obliges the buyer to make a proportionate ITC reversal: because the effective price of the purchase has fallen, the input tax credit taken on the original invoice is now excess and must be given back. This only works where the discount was known and linked as required — the conditions in Section 15(3)(b) for a post-supply discount to reduce taxable value.

A financial or commercial credit note, by contrast, carries no GST adjustment. The supplier does not reduce its output tax, the buyer does not touch its ITC, and the credit is purely a settlement of account. The distinction between the two instruments is the whole subject of financial vs. tax credit notes under GST, and it echoes downstream in GST adjustments on channel settlements.

The buyer's obligation on a tax credit note received is the mirror of the seller's obligation on one issued, so the mechanics — what to reverse, when, and how to report it — are set out in full in the ITC reversal on post-sale discounts and credit notes guide, which reflects Circular 251/08/2025-GST on post-sale discounts (summarised in the CBIC Circular 251 explainer). One caveat sits alongside all of this: where a rebate settles against goods written off or destroyed, Section 17(5)(h) blocks the credit entirely — a different route from the proportionate reversal above. Given how often these positions shift, treat this section as subject to publish-time verification and CA review.

Where should you go next?

- GST treatment of FMCG claims and schemes — the sell-side companion, covering how schemes, discounts and claims are taxed.

- GST credit notes for rebates under Rule 53(1A) — the documentation rule behind every rebate credit note.

- Credit notes for expired, damaged and returned goods — where the Section 17(5)(h) write-off question bites hardest.

- FMCG trade schemes explained and calculating FMCG distributor claims — the sell-side schemes this buy-side view mirrors.

- Vendor rebate management software — how buy-side rebates are tracked, accrued and reconciled in one place, and how it differs from a billback.

- Product basics: the rebate concept in the ClaimDS docs.

<!-- TODO CA REVIEW before publish: confirm Ind AS 2 section and all GST citations (Section 34, 15(3)(b), 17(5)(h), Circular 251/08/2025-GST) -->GST and accounting note: This article is general information, not tax, accounting or legal advice. The Ind AS 2 treatment and the GST credit-note positions above must be re-verified at publish time and reviewed by a qualified chartered accountant before any of it is relied on.

Seeing buy-side TOD, CD and target incentives accrue and settle against the right supplier — with the credit-note type and inventory treatment handled — is what turns a year-end reconciliation scramble into a controlled flow. To see it working on your own vendor agreements and claim volumes, book a demo.

Frequently asked questions

What is a turnover discount?

A turnover discount (TOD) is a rebate a supplier credits on your total purchase turnover over a quarter or a year, released in arrears once an agreed volume or value slab is crossed. In Indian trade it is the dominant term for what English sources call a supplier or purchase volume rebate, and it is settled by credit note against the buyer's account.

What is a cash discount in FMCG?

A cash discount (CD) is a reduction a supplier gives for paying an invoice early or within stated payment terms — a reward for prompt settlement rather than for volume. It is earned on the primary purchase, so it is simple to validate against the invoice date. FMCG buyers treat it as a reduction in the cost of the goods purchased, not as separate income.

Is a purchase rebate income or a reduction in cost?

Under Ind AS 2 a rebate received on goods bought is generally a reduction in the cost of purchase, not other income. It is deducted in measuring what the inventory cost you and flows through to cost of goods sold as the stock is consumed. Booking it as income overstates revenue and understates gross margin, so the classification matters to the accounts.

Does a supplier credit note require ITC reversal?

Only if it is a Section 34 tax credit note that reduces the GST originally charged — then the buyer must reverse input tax credit proportionately, because the effective price has fallen. A financial or commercial credit note carries no GST adjustment, so no ITC is touched. The buyer must therefore classify every supplier credit note by type before acting on it.

What is the difference between a sales rebate and a purchase rebate?

A sales rebate is money you pay down your channel to earn a sale — a trade-spend expense. A purchase rebate is money you earn from a supplier you buy from — a reduction in the cost of your inventory. The same rupee is an expense to the payer and a cost reduction to the earner, and the two sit on opposite sides of the ledger with different GST treatment.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Supplier and Purchase Rebates in Agri-Inputs

How Indian agri-input makers treat money from raw-material and packaging suppliers — turnover and cash discounts under Ind AS 2 and GST credit notes.

Supplier and Purchase Rebates in Automotive

How Indian automotive treats money received from component and material suppliers — turnover and cash discounts under Ind AS 2 and GST credit notes.

Supplier and Purchase Rebates in Indian Paints

How Indian paints treats money received from raw-material and packaging suppliers — turnover and cash discounts under Ind AS 2 and GST credit notes.