GST Treatment of FMCG Claims, Schemes and Returns

How FMCG scheme settlements are taxed — Section 34 tax vs financial credit notes, ITC on damaged stock, free goods and Section 194R on incentives.

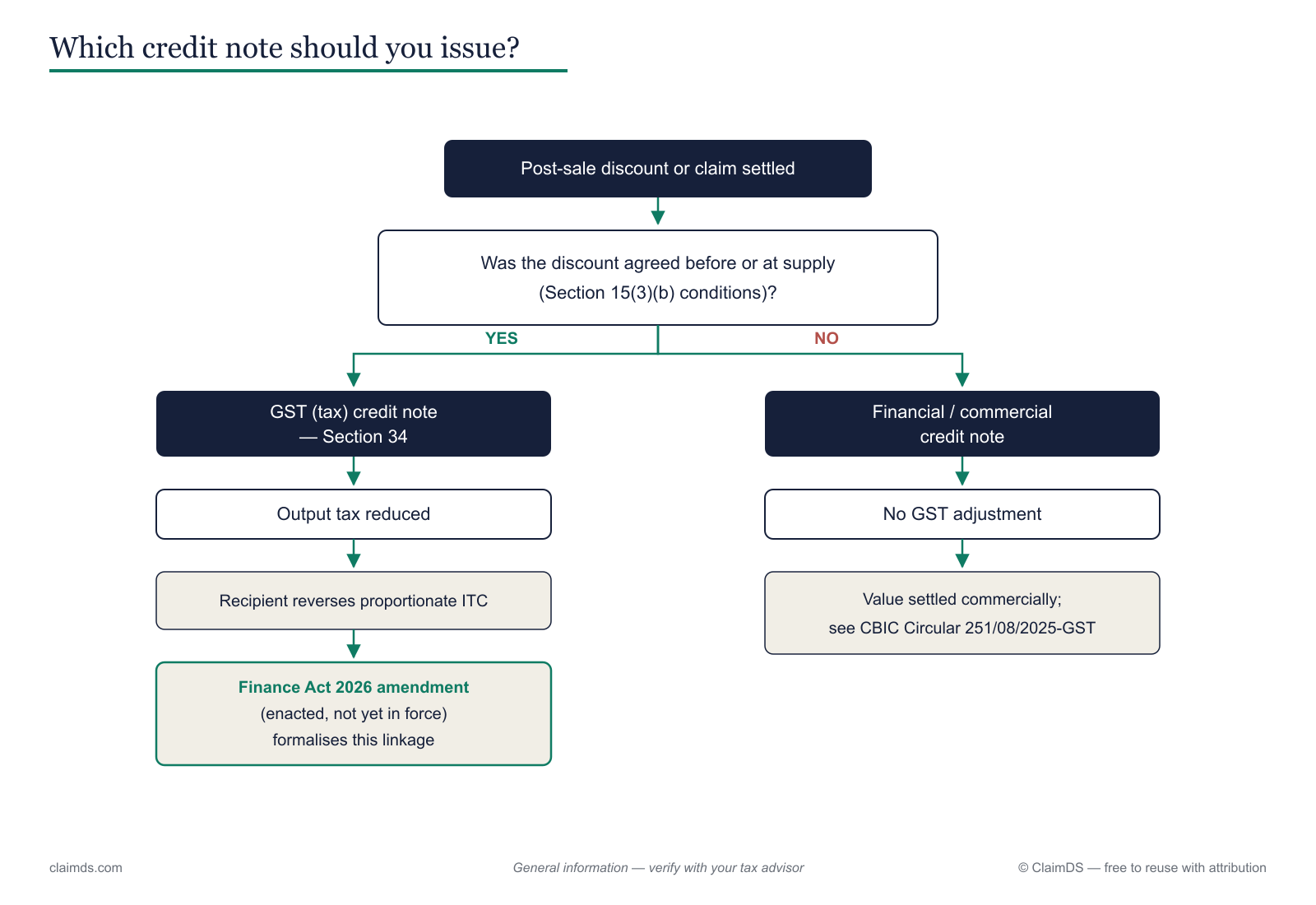

In FMCG, the GST outcome of a scheme settlement depends on the document you raise, not the name of the scheme. A Section 34 tax credit note adjusts both value and tax, and obliges the recipient to reverse proportionate ITC. A financial or commercial credit note carries no GST adjustment at all — value, output tax and the recipient's credit stay untouched. Which one you may use depends on how the discount was agreed with the channel partner in the first place.

Secondary scheme settlement: which credit note?

Which credit note applies to a scheme settlement depends on whether the discount met the Section 15(3)(b) conditions agreed before supply.

This is the core FMCG question. A secondary scheme is settled after the original invoice, so it is a post-supply discount — and post-supply discounts have a specific gate. Under Section 15(3)(b) of the CGST Act, a discount can be excluded from the taxable value only where three conditions are met: the discount was agreed before or at the time of supply, it is linked to the relevant invoices, and the recipient reverses the ITC attributable to it. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Circular 251 position and recipient-ITC treatment -->

If those conditions are satisfied, the company can raise a Section 34 tax credit note. That reduces the supplier's output tax, and in turn the distributor must reverse the proportionate credit — the two sides move together. We unpack that mechanism in financial vs. tax credit notes under GST and trace the reversal in ITC reversal on post-sale discounts and credit notes.

If the conditions were not met — most on-the-fly trade schemes are agreed after the goods have already shipped — the tax route is closed. The settlement then goes through a financial or commercial credit note. CBIC Circular 251/08/2025-GST, described conservatively here, clarifies that where a supplier passes a post-sale discount through a financial or commercial credit note, the recipient is not required to reverse ITC, because the original transaction value and the supplier's output tax are unchanged. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Circular 251 position and recipient-ITC treatment -->

The practical discipline is to decide the credit-note type at design time, document the pre-supply agreement, and keep the invoice linkage so the basis can be proved later. That governs how the settlement flows into GST adjustments on channel settlements and how the numbers reconcile in scheme credit notes against GSTR-2B and 3B. For the broader treatment of scheme discounts, see GST on trade discounts and dealer incentives and the Section 15(3)(b) conditions in detail. The full settlement discipline lives in the scheme settlement GST documentation playbook and in rebate accounting with GST credit notes.

Damage, expiry and destroyed stock

FMCG runs on short shelf lives, so a share of stock is always written off — expired biscuits, leaking sachets, damaged cartons. GST treats this differently from a discount. Under Section 17(5)(h) of the CGST Act, input tax credit is blocked on goods that are lost, stolen, destroyed or written off. Where a company or distributor has already claimed ITC on stock that is later destroyed on expiry or damage, that credit must be reversed. <!-- TODO VERIFY AT PUBLISH -->

The commercial question — who bears the loss — is separate from the tax question. In many FMCG schemes the company compensates the distributor for expired or damaged stock through a stock-compensation or expiry settlement. That compensation is a commercial arrangement set by the scheme terms; it does not change the fact that the credit on destroyed goods is blocked under Section 17(5)(h). If the company physically takes the stock back rather than merely funding a write-off, the flow becomes a return or reversal, which is documented and taxed on its own footing. <!-- TODO VERIFY AT PUBLISH -->

So the settlement design has two moving parts to keep straight: the credit-note that adjusts the money between company and distributor, and the ITC reversal the party holding the destroyed goods must make. Conflating them is a common source of channel-finance leakage. The distributor-side view of these claims sits in distributor claims management, and clawbacks on cancelled schemes are handled in rebate clawbacks and scheme cancellations.

Free goods, combo and BOGO schemes

Free-goods mechanics — buy-one-get-one, combo packs, extra-grammage, quantity bonuses — raise two GST questions at once: is there ITC to reverse on the goods given away, and is there a valuation adjustment on the bundle? The answers turn on how the offer is structured — whether the free item is genuinely free, priced into the combo, or a separately invoiced gift — and each structure lands differently.

Because the treatment is offer-specific and easy to get wrong, we keep the depth in a dedicated piece rather than compressing it here. Route through to GST on free goods and BOGO schemes for the ITC-and-valuation walkthrough, and see how the scheme itself is designed in FMCG trade schemes explained. The pointer to remember at settlement time: a "free" unit that has already carried input tax may sit inside Section 17(5) territory, so decide the ITC position before the scheme goes live, not after. <!-- TODO VERIFY --> The pricing and margin angle on distributor incentives is covered in GST on distributor margin, commission and incentives.

TDS under Section 194R on distributor incentives

Not every incentive is a discount. When a company gives a distributor a benefit or perquisite in kind — free goods beyond the invoice, a foreign trip, gifts, sponsored events — Section 194R brings TDS into play. The provision applies TDS at 10 percent on the value of such benefits, once the aggregate value to a single distributor crosses 20,000 rupees in a financial year. <!-- TODO VERIFY AT PUBLISH: rate, threshold, section mapping -->

The catch that surprises finance teams is that the benefit need not be cash — a benefit in kind still attracts the deduction, which means the company must arrange to recover or gross up the tax on a non-cash perk. That is why a foreign trip or a bulk gift scheme needs the 194R position worked out before it is announced, not at year-end.

Note the framework change: Section 194R and its cohort of TDS provisions are being consolidated into the Income-tax Act, 2025 framework, effective 1 April 2026 — so the section mapping and cross-references should be re-checked against the new Act rather than assumed from the older numbering. <!-- TODO VERIFY AT PUBLISH: rate, threshold, section mapping --> The full mechanics sit in Section 194R TDS on dealer and distributor incentives, and the wider tax map across settlement types is in tax on rebates, chargebacks, billbacks and buybacks in India.

The Finance Act 2026 change

There is one moving statutory piece to flag without over-reading it. The Finance Act 2026 enacted amendments touching Section 15(3)(b) and Section 34 of the CGST Act — the very provisions that govern post-supply discounts and credit notes. The Act received assent on 30 March 2026. <!-- TODO VERIFY AT PUBLISH: notification status -->

The critical point for compliance: the relevant provisions are not yet notified into force. Enactment and commencement are separate steps under Indian law, and until a commencement notification issues, the amended wording does not operate. Until then, the position above — existing Section 34 read with CBIC Circular 251/08/2025-GST — is what applies. Always confirm the current notification status before relying on the amended text. <!-- TODO VERIFY AT PUBLISH: notification status --> The credit-note timing and reporting mechanics, which the amendment touches, are covered in GST credit-note time limits and reporting.

GST note: This article is general information, not tax or legal advice. Every GST position here — the Section 15(3)(b) conditions, Section 34 tax credit notes, Section 17(5)(h) ITC blocking, Rule 37, Section 194R, CBIC Circular 251/08/2025-GST (which superseded the certificate mechanism of Circular 212/6/2024), and the Finance Act 2026 amendments assented but not yet notified into force — must be re-verified at publish time with a qualified professional. Any 18 percent figure used below is illustrative arithmetic only, not a rate assertion. <!-- TODO VERIFY AT PUBLISH -->

For a worked illustration: on a ₹1,00,000 invoice at an illustrative 18 percent GST, a tax credit note settling a 5 percent scheme reduces value by ₹5,000 and output tax by ₹900, and the distributor reverses ₹900 of ITC — whereas a financial credit note for the same ₹5,000 leaves the tax untouched. The reversal timing itself follows Rule 37 and the 180-day rule. <!-- TODO VERIFY AT PUBLISH --> The documentation stack sits in GST credit notes for rebate schemes.

Where this fits in the FMCG channel

Every settlement above — schemes, damage, free goods, incentives — is one strand of the same channel-finance problem: choosing the right document, proving the basis, and reversing credit where the law requires it. See the full picture in the pillar guide, channel claims and rebates in Indian FMCG, and the operational flow in the FMCG claim settlement process. For how ClaimDS enforces the credit-note decision and the reversal trail, see /docs/credit-note and the ITC reversal lifecycle.

Ready to make scheme settlement GST-clean by design? Book a demo to see how ClaimDS picks the right credit note, holds the pre-supply evidence, and keeps the reversal trail audit-ready.

Frequently asked questions

Is GST applicable on FMCG trade schemes?

It depends on the settlement document, not the scheme label: a trade scheme paid through a Section 34 tax credit note adjusts value and output tax, while a financial or commercial credit note carries no GST effect. Whether you may use the tax route turns on meeting the Section 15(3)(b) conditions agreed before supply.

Which credit note is used for a secondary scheme?

Either route is possible: a Section 34 tax credit note where the Section 15(3)(b) conditions were met, or a financial credit note where they were not. Most FMCG secondary schemes settle through a financial or commercial credit note, which leaves transaction value, output tax and the recipient ITC untouched.

Does a financial credit note require ITC reversal?

No: a financial or commercial credit note does not reduce the original transaction value or the supplier output tax, so there is nothing for the recipient to reverse. ITC reversal is triggered only by a Section 34 tax credit note that reduces output tax, per CBIC Circular 251/08/2025-GST described conservatively.

Is ITC reversal required on expired FMCG stock?

Where FMCG goods are written off or destroyed on expiry or damage, Section 17(5)(h) blocks input tax credit, so credit already taken on those goods must be reversed. Who bears that cost between company and distributor is a commercial matter set by the scheme terms, not by the statute.

Is TDS applicable on distributor incentives?

Yes: Section 194R applies TDS to benefits or perquisites given to a distributor, including benefits in kind such as goods, trips and gifts, at 10 percent once the aggregate crosses 20,000 rupees in a year. Confirm the rate, threshold and current section mapping with a professional before deducting.

What are the Section 15(3)(b) conditions for a scheme discount?

A post-supply discount leaves the taxable value under Section 15(3)(b) only where the discount was agreed before or at the time of supply, is linked to specific invoices, and the recipient reverses the ITC attributable to it. Miss any condition and the discount cannot ride a tax credit note.

Is the Finance Act 2026 change to GST credit notes in force?

Not yet: the Finance Act 2026 amendments touching Sections 15(3)(b) and 34 received assent on 30 March 2026, but the relevant provisions are not yet notified into force. Until a notification issues, the existing Section 34 read with CBIC Circular 251/08/2025-GST is the operative position.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Automotive Warranty Claims: Process and GST

How automotive warranty claims work and are taxed — the claim and reimbursement process, and the GST treatment of warranty replacements under Circular 216.

GST and TDS on Automotive Dealer Incentives

How automotive dealer incentives are taxed — credit-note choice under GST and Section 194R TDS on trips, gifts and benefits-in-kind given to dealers.

GST and TDS on Paints Dealer and Painter Rewards

How paints dealer schemes and painter loyalty rewards are taxed — GST credit-note choice and Section 194R TDS on rewards in kind to dealers and painters.