GST and TDS on Paints Dealer and Painter Rewards

How paints dealer schemes and painter loyalty rewards are taxed — GST credit-note choice and Section 194R TDS on rewards in kind to dealers and painters.

Paints incentives raise two separate tax questions. First, how a dealer scheme is settled under GST — a tax credit note under Section 34, a financial or commercial credit note, or a straight payout — because each route lands the input-tax credit differently. Second, whether Section 194R TDS bites on painter and contractor loyalty rewards given in kind: gifts, gold, foreign tours. Both answers turn on how the benefit is given, not on what it is called. Every figure below is illustrative and must be verified with a qualified professional before you rely on it.

GST and tax note: This article is general information, not tax or legal advice. Every statutory reference, rate, threshold, and date below must be re-verified at publish time with a qualified professional.

GST on a dealer scheme: which document?

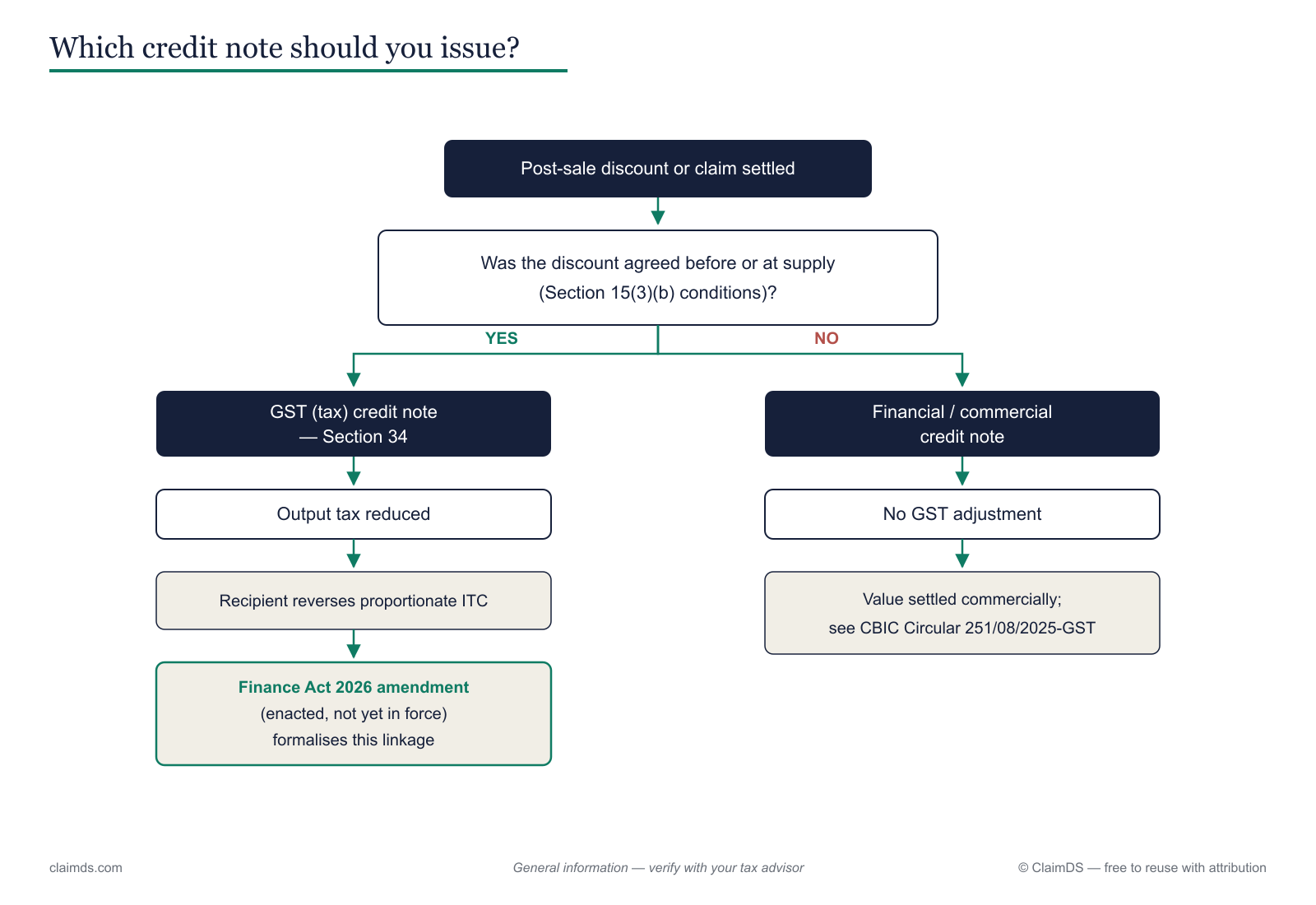

A dealer scheme can be settled in more than one way, and the document you choose decides whether the settlement carries tax.

A tax credit note under Section 34 of the CGST Act reduces the supplier's original output tax. It is available only where the post-supply discount meets the Section 15(3)(b) conditions: the discount is established in an agreement entered into before or at the time of supply, it is linked to specific invoices, and the recipient reverses the input-tax credit attributable to it. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Section 15(3)(b) conditions and Section 34 tax-credit-note mechanics --> Where those conditions are met and a tax credit note is raised, the dealer must reverse the matching ITC. We unpack those conditions line by line in Section 15(3)(b) and post-supply discounts under GST.

A financial or commercial credit note does the opposite. It settles the scheme as a pure accounting adjustment, leaves the original transaction value and output tax untouched, and — at the pointer level of CBIC Circular 251/08/2025-GST — carries no requirement for the dealer to reverse ITC. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: CBIC Circular 251/08/2025-GST treatment of financial credit notes --> A straight payout or a debit-note-driven claim sits in the same family: the tax already charged on the original supply does not move. The full contrast between the two documents is in financial vs. tax credit notes under GST, and the reversal side is walked through in ITC reversal on post-sale discounts and credit notes.

The practical consequence is the recipient's ITC. A tax credit note pulls credit out of the dealer's books; a financial credit note leaves it in place. A separate reversal trigger under Rule 37 can apply where the dealer has not paid the supplier within the prescribed time — a different mechanism entirely, not to be confused with the credit-note choice. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Rule 37 non-payment reversal pointer --> For channel finance teams, the discipline is to fix the route at design time and keep the audit trail, exactly as we describe for GST adjustments in channel settlements and in the CBIC Circular 251 practical guide. The same logic drives rebate accounting on GST credit notes.

The document that settles a dealer scheme decides whether it carries tax.

The document that settles a dealer scheme decides whether it carries tax.

Section 194R: TDS on painter and contractor rewards

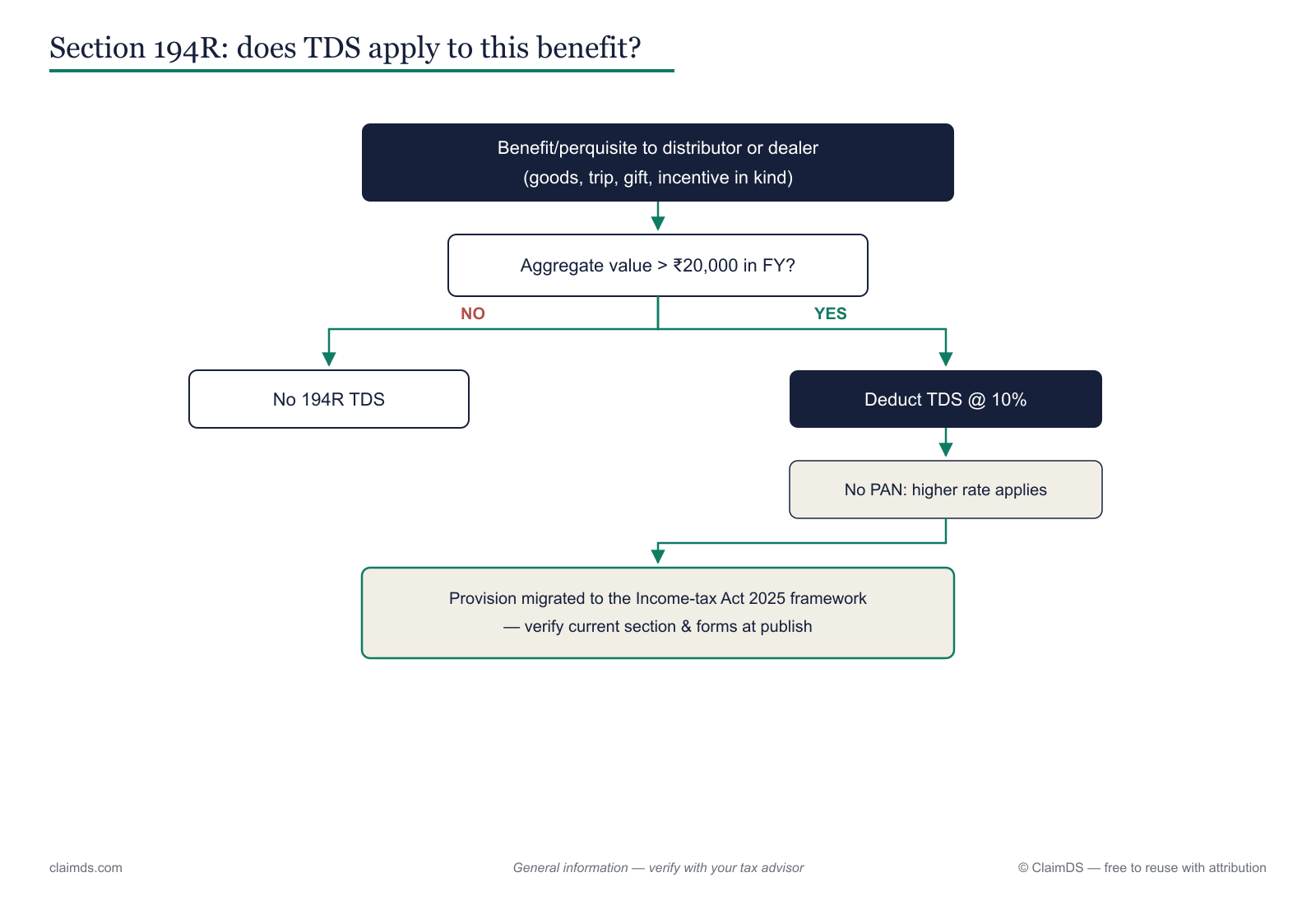

This is the part unique to paints. Beyond the dealer, brands run loyalty programs for the painters and contractors who actually apply the product — and those programs frequently reward in kind: gift articles, gold coins, tool kits, and sponsored domestic or foreign tours.

A reward in kind to a painter above the annual threshold can attract Section 194R — the value, not the cash, is what triggers it.

A reward in kind to a painter above the annual threshold can attract Section 194R — the value, not the cash, is what triggers it.

Where a resident painter or contractor is carrying on a business or profession, a reward that is a benefit or perquisite arising from that activity can attract TDS under Section 194R at 10% of the value, once the aggregate value provided to that person exceeds ₹20,000 in a financial year. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: 194R rate (10%), threshold (₹20,000), and section mapping --> Where the recipient does not furnish a PAN, a higher rate applies. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: no-PAN higher-rate treatment --> Because a reward in kind carries no cash from which to withhold, the provider has to arrange for the tax before or alongside releasing the reward — the value of the benefit, not any payment, is what the deduction is computed on.

Two cautions matter here. First, the provision now sits within the Income-tax Act 2025 framework, effective 1 April 2026, so the section reference you cite should be confirmed against the current law rather than assumed. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Income-tax Act 2025 framework, effective 1 April 2026, and section renumbering --> Second — and this is the important one — the application of Section 194R to a specific loyalty-program structure is fact-specific. Whether a given reward is a covered benefit, who the recipient is, and how the program is documented all change the answer. Do not read this as a blanket position that every painter reward attracts TDS; take a qualified opinion on your own scheme. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: application of 194R to loyalty-program rewards is fact-specific — no blanket assertion -->

The mechanics of in-kind valuation and collection for channel partners are covered in our Section 194R guide for dealer and distributor incentives, the automotive parallel on GST and TDS for dealer incentives, and the broader design of channel loyalty programs. For the painter-specific program design, see painter and contractor loyalty programs.

How does a cash incentive differ from a benefit in kind?

The reason the two paths diverge is structural. A cash or credit-note incentive that reduces the price is, in substance, a price adjustment — it flows through the GST credit-note machinery above and is generally analysed as a lesser realisation of the sale, not as a separate benefit. A reward in kind — a gift, gold, or a tour — is a benefit or perquisite whose value is what the Section 194R analysis turns on.

There is also a GST-side wrinkle for goods given away. Input-tax credit can be blocked under Section 17(5)(h) on goods disposed of by way of gift or free samples, which is a separate question from the TDS on the recipient's side. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Section 17(5)(h) ITC block on gifts and free samples --> The two taxes look at the same reward from opposite ends: GST asks whether the giver can claim credit on what was given away; Section 194R asks whether the giver must deduct tax on the value received by the painter.

The practical structuring consequence — at the pointer level, and not as advice — is that a brand deciding between a price-linked incentive and an in-kind reward is also, implicitly, choosing between two tax regimes. That choice is worth making deliberately, with a professional, at scheme-design time rather than at settlement. The wider taxonomy of these instruments is mapped in tax on rebates, chargebacks, billbacks and buybacks in India and GST on trade discounts and dealer incentives.

Is the Finance Act 2026 change in force yet?

Not as far as this article can confirm. The Finance Act 2026 carries amendments touching Section 15(3)(b) and Section 34 of the CGST Act. They were enacted — assent 30 March 2026 — but they are not yet notified into force. <!-- TODO VERIFY AT PUBLISH: Finance Act 2026 amendments to Section 15(3)(b)/34, assented 30 March 2026, notification status --> Until notification, the operative position is the existing Section 34 read with CBIC Circular 251/08/2025-GST. State the notification status as at your publish date, because it can change without much notice.

The GST and TDS disclaimer

This article is general information for finance and channel teams in the paints sector, not tax or legal advice. GST and income-tax positions — including Section 15(3)(b), Section 34, Section 17(5)(h), Rule 37, Section 194R, CBIC Circular 251/08/2025-GST, the Finance Act 2026 amendments, and the Income-tax Act 2025 framework — are subject to change and to fact-specific interpretation. Every rate, threshold, section reference, and date above must be re-verified at publish time and applied to your own facts by a qualified chartered accountant, cost accountant, or tax counsel before you act. For product-side references, see the ClaimDS credit-note documentation and TDS on incentives documentation.

Getting paints incentives settled cleanly

The paints channel runs two settlement engines at once — dealer schemes on one side, painter and contractor loyalty on the other — and they answer to different tax rules. Getting both right means fixing the credit-note route at design time, valuing in-kind rewards defensibly, and keeping an audit trail that a reviewer can follow. That is the settlement discipline our distributor claims management, secondary scheme settlement, and rebate management software are built for, alongside trade promotion management, the CFO playbook on claims and deductions, and the sector view in channel claims and rebates for Indian FMCG and credit notes for expired and damaged goods returns. It all ties back to the paints channel claims and rebates pillar and the paints dealer claim settlement process.

Want to see how ClaimDS settles paints dealer schemes and painter loyalty rewards with the tax trail attached? Book a demo.

Frequently asked questions

Is GST applicable on paints dealer schemes?

It depends on how the scheme is settled, not on what it is called. Passed through a financial or commercial credit note, a dealer scheme is a pure accounting adjustment that leaves the original transaction value and output tax untouched. Passed through a tax credit note under Section 34, it reduces the supplier output tax and the dealer reverses input-tax credit. Confirm the position with a qualified professional.

Which credit note is used for a dealer scheme?

Either can be used, and the choice is a design decision. A Section 34 tax credit note is available only where the Section 15(3)(b) conditions are met — a pre-supply agreement, invoice linkage, and recipient ITC reversal. A financial or commercial credit note carries no tax and needs no ITC reversal per CBIC Circular 251/08/2025-GST. Decide the route before you settle, and document the basis.

Is TDS applicable on painter loyalty rewards?

It can be. Where a resident painter or contractor carries on a business or profession, a reward that is a benefit or perquisite in kind can attract Section 194R TDS at 10% once the aggregate value crosses the annual threshold. The application to a specific loyalty program is fact-specific, so do not assume a blanket position — take a qualified opinion on your own scheme.

Is a gift or tour given to a painter taxable?

A gift, gold article, or sponsored foreign tour given to a painter who carries on business is a benefit in kind, and it is the value of that benefit — not any cash — that can trigger Section 194R. Because the reward is wholly in kind, the tax has to be arranged before or alongside the reward. The exact treatment for your program should be confirmed with a CA.

What is the 194R threshold?

Section 194R can apply where the aggregate value of benefits or perquisites provided to a recipient exceeds ₹20,000 in a financial year, with tax at 10% of the value. Where the recipient has no PAN, a higher rate applies. These figures and their application to loyalty rewards must be re-verified at publish time with a qualified professional before you rely on them.

Does a cash rebate to a painter differ from an in-kind reward?

In substance, yes — the two are taxed on different footings. A cash or credit-note incentive that reduces the price is treated as a price adjustment. A reward in kind — a gift, gold, or a tour — is a benefit or perquisite whose value is what the Section 194R analysis turns on. How you structure the reward therefore changes the tax question, so plan it deliberately and take advice.

Is the Finance Act 2026 credit-note amendment in force?

Not as far as this article can confirm. The Finance Act 2026 carries amendments touching Section 15(3)(b) and Section 34 of the CGST Act, assented on 30 March 2026, but they take effect only from a date to be notified. Until notification, the existing Section 34 read with CBIC Circular 251/08/2025-GST is the operative position. Always check the current notification status before relying on the amended wording.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Automotive Warranty Claims: Process and GST

How automotive warranty claims work and are taxed — the claim and reimbursement process, and the GST treatment of warranty replacements under Circular 216.

GST and TDS on Automotive Dealer Incentives

How automotive dealer incentives are taxed — credit-note choice under GST and Section 194R TDS on trips, gifts and benefits-in-kind given to dealers.

GST on Agri-Input Claims and Schemes

How agri-input dealer schemes, liquidation claims and near-expiry returns are treated under GST — credit-note choice, ITC reversal and mixed input rates.