Automotive Warranty Claims: Process and GST

How automotive warranty claims work and are taxed — the claim and reimbursement process, and the GST treatment of warranty replacements under Circular 216.

An automotive warranty claim is where a dealer replaces a defective part for the customer at no charge during the warranty period and then recovers the cost from the vehicle maker (OEM). The customer pays nothing; the burden moves up the channel. The GST treatment turns on one question — whether any separate consideration is charged. Circular 216/10/2024-GST sets out how warranty replacements and dealer reimbursements are handled, and an extended warranty sold for a fee is treated as a separate supply. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Circular 216/10/2024 warranty-replacement and reimbursement positions -->

How does an automotive warranty claim work?

A warranty claim runs through a fixed sequence, and each stage leaves a record the OEM will later validate.

Defect reported. The customer brings the vehicle in, or a service touchpoint flags a covered fault. The service advisor opens a job card capturing the symptom, the odometer reading and the vehicle identity.

Dealer replaces the part under warranty. The technician diagnoses the fault, fits the replacement part free of charge to the customer, and records the work against the job card, the VIN/chassis number and the part number of the component replaced. The defective part is set aside for return or scrap, because the OEM will want proof of it.

Dealer files the claim with the OEM. The dealer assembles the claim — job card, VIN, part number, labour, and the defective-part evidence — and submits it through the OEM's warranty portal or dealer-management system. This is a channel claim like any other; the mechanics mirror the wider dealer claim settlement process and the general claim process.

Validation. The OEM checks warranty-period compliance, matches the part number to the approved bill of materials, confirms the VIN is genuinely under coverage, and reviews the defective-part return or scrap proof. Claims that fail any check are rejected or short-paid.

Reimbursement or credit note. Approved claims are settled — either as a payment against the claim or through a credit note adjusting the dealer's running account. This is where the settlement and the GST characterisation meet, and where the wider automotive channel claims picture connects.

Status flow: Reported → Replaced → Filed → Under validation → Approved (or Rejected) → Settled. Tracking each claim against these states is what stops warranty recoveries from ageing quietly — the same discipline behind any dealer claims management system, and the reason reversals and re-submissions need their own returns and reversals handling.

What evidence does a warranty claim need?

An OEM will only reimburse a claim it can defend on audit, so the evidence set is strict. Each item below answers a specific validation question, and a missing item is the most common cause of rejection or short-payment.

| Evidence | What it proves | Why the OEM needs it |

|---|---|---|

| Job card | The defect reported, diagnosis and work done | Establishes a genuine covered fault, not wear-and-tear or misuse |

| VIN / chassis number | The exact vehicle serviced | Confirms the vehicle is under coverage and not double-claimed |

| Part number | The component replaced | Matches the approved bill of materials and the reimbursement rate |

| Defective-part return / scrap proof | The old part was surrendered or destroyed | Prevents claiming for parts never actually replaced |

| Warranty-period compliance | Failure fell inside the coverage window | The single hardest eligibility gate — date and odometer bound |

Well-run dealers treat this set as a checklist captured at the point of service, not reconstructed later. The stronger the linkage between job card, VIN, part number and defective-part proof, the faster validation clears — and the fewer claims age into disputes. This is the same claim-integrity principle covered across claims management software: a claim is only as good as the evidence chain it can produce on demand.

How does GST treat warranty replacements under Circular 216/10/2024?

This is the core of the tax question, and the safe reading is a conservative one.

A warranty replacement made without separate consideration is treated differently from a return or a written-off part — the GST outcome depends on the arrangement.

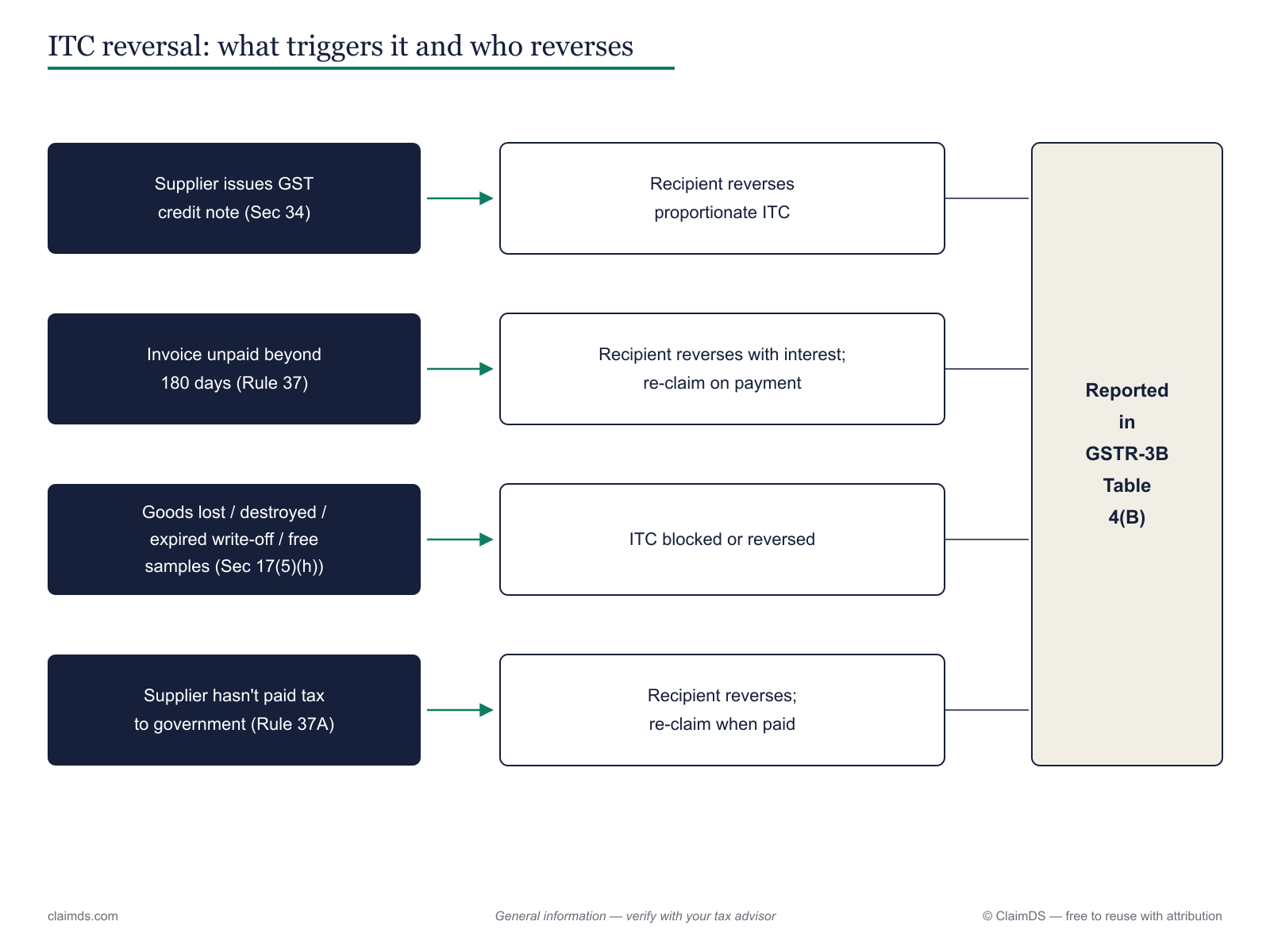

Where a part is replaced under warranty with no separate consideration charged to the customer, the conservative position is that no GST is charged on that replacement — because the value of the warranty was already built into, and taxed as part of, the original supply of the vehicle or part. On the same reasoning, the input tax credit on the replaced part need not be reversed, since its value sat inside that original taxable supply rather than being a fresh, standalone free supply. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Circular 216/10/2024 warranty-replacement and reimbursement positions -->

Circular 216/10/2024-GST addresses the arrangement in more than one shape, and the treatment can differ by who does the replacing and how they are made whole: <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Circular 216/10/2024 warranty-replacement and reimbursement positions -->

- Replacement by the OEM directly — the maker supplies the replacement part or goods to the customer under warranty.

- Replacement by the distributor or dealer, who is then reimbursed — the dealer replaces the part and recovers from the OEM, whether by a credit note or otherwise; how that reimbursement is documented affects the GST characterisation. <!-- TODO VERIFY AT PUBLISH + CA REVIEW: Circular 216/10/2024 dealer reimbursement position -->

- Extended warranty as a distinct supply of service — treated separately from the free in-warranty replacement (see the next section).

Two adjacent reversal triggers are worth separating out, because teams conflate them with warranty replacement:

- If a defective part that is taken back is written off or destroyed rather than repaired, the input tax credit attributable to those goods falls under Section 17(5)(h) and must be reversed by whoever availed it. <!-- TODO VERIFY AT PUBLISH: Section 17(5)(h) blocked/reversed ITC on destroyed or written-off goods -->

- Separately, where consideration for an inward supply is not paid within the prescribed period, Rule 37 requires the recipient to reverse the proportionate credit — a non-payment trigger, unrelated to warranty. <!-- TODO VERIFY AT PUBLISH: Rule 37 non-payment ITC reversal mechanics and timeline -->

Neither of those is the same event as a free warranty replacement, which is precisely why the diagram above maps the triggers apart. Where a reimbursement is instead structured as a discount or price adjustment, the credit-note rules under Section 34 and the pre-agreement conditions in Section 15(3)(b) come into play — the financial versus tax credit note distinction and the ITC-reversal-on-credit-notes rules govern that path. <!-- TODO VERIFY AT PUBLISH: Section 34 and Section 15(3)(b) credit-note treatment where reimbursement is a discount --> For the OEM-side warranty circular framing specifically, see the existing GST on warranty replacements in the channel article, and for how any resulting credit note sits inside a settlement, GST adjustments to channel settlements and credit-note time limits and reporting.

How is extended warranty or an AMC taxed?

An extended warranty or an annual maintenance contract (AMC) is a different animal from a free in-warranty part swap. It is bought for a separate charge, and the conservative reading is that it is a distinct supply of service, taxed on its own consideration when sold. <!-- TODO VERIFY AT PUBLISH: extended warranty / AMC as separate supply of service and its time and value of supply -->

That distinction matters because the two are easy to bundle and mis-map. A free replacement under the base warranty carries no fresh GST on the part; an extended warranty sold at the point of vehicle purchase, or later as a standalone product, is its own taxable service supply. Whether the extended-warranty charge is invoiced upfront, embedded in a package, or billed separately changes the time and value of supply — so the characterisation has to be read against the actual contract, not assumed. <!-- TODO VERIFY AT PUBLISH: time and value of supply for bundled versus standalone extended warranty -->

Because these are service supplies tied to dealer offers, they also interact with how dealer incentives and margins are taxed — treated at a pointer level here, with the mechanics in GST on distributor margin and commission incentives, GST on trade discounts and dealer incentives, and the automotive-specific GST and TDS on dealer incentives. Where a claim spans warranty parts and a serviced AMC, the sector treatments in GST on FMCG claims and schemes and GST on pharma claims and returns show how differently a "claim" can be characterised across industries — automotive dealers, distributors and super-stockists each sit at a different point in that chain. This section is a pointer, not a determination — confirm the specifics with a professional.

What does the Finance Act 2026 change?

The Finance Act 2026 carries amendments touching provisions including Section 15(3)(b) and Section 34 of the CGST Act. It received assent on 30 March 2026 — but, as of the date of writing, those provisions had not been notified into force. <!-- TODO VERIFY AT PUBLISH: Finance Act 2026 assent date 30 March 2026 and notification status of the Section 15(3)(b) and Section 34 amendments -->

Stated exactly: the amendments are enacted but pending notification. Until the government issues a commencement notification bringing them into effect, the existing position continues to apply, and nothing in this article should be read as reflecting the amended text. Related instruments — such as the rule-based credit-note conditions for rebates and the broader tax treatment of channel instruments — may also move once notified, so treat the current guidance as provisional on that front. <!-- TODO VERIFY AT PUBLISH: notification status before publish -->

Disclaimer: This article is general information, not tax or legal advice. The GST positions above are drawn from CBIC Circular 216/10/2024-GST and the referenced CGST provisions — Section 34, Section 15(3)(b), Section 17(5)(h) and Rule 37 — and reflect a conservative reading as of the date of writing. The Finance Act 2026 amendments touching Sections 15(3)(b) and 34 are enacted (assent 30 March 2026) but were not notified into force as of writing. Any illustrative figure (for example, an 18% rate) is illustrative only. Verify the current provisions and notification status on cbic-gst.gov.in and with a qualified CA or CMA before acting.

Bringing the claim and the tax together

A warranty claim only settles cleanly when the operational trail and the tax trail agree — the job card, VIN, part number and defective-part proof on one side, and the correct GST characterisation of the replacement or reimbursement on the other. A platform like ClaimDS ties each warranty claim to its evidence, tracks it through the status flow, and keeps the reimbursement, credit note and reporting linkage auditable end to end — the reference mechanics live in how a credit note works and the ITC reversal lifecycle.

To see warranty and settlement claims running on your own dealer network, book a demo.

Frequently asked questions

What is a warranty claim in automotive?

A warranty claim is where a dealer replaces a defective part for the customer at no charge during the warranty period, then recovers the cost from the vehicle maker (OEM). The customer pays nothing for the covered part; the economic burden moves up the channel to the OEM through a validated claim and a reimbursement or credit note.

Is GST charged on a warranty replacement?

Conservatively, no — where a part is replaced under warranty with no separate consideration charged to the customer, no GST is charged on that replacement, because its value was already taxed in the original sale of the vehicle or part. GST applies only if separate consideration is charged. Confirm the current position and your fact pattern with a qualified professional before relying on it.

Does a warranty replacement need ITC reversal?

Conservatively, a free warranty replacement made without separate consideration does not by itself require the input tax credit on the replaced part to be reversed, because that value sat inside the original taxable supply. Separate reversal triggers — such as a written-off or destroyed defective part — are governed by their own provisions and should be assessed individually with a professional.

How is a dealer reimbursed for a warranty replacement?

The dealer files a validated claim with the OEM — job card, VIN, part number and defective-part return or scrap proof — and the OEM settles it. Reimbursement flows either as a payment against the claim or through a credit note adjusting the dealer account. The exact GST characterisation of that settlement depends on the arrangement and should be reviewed with a professional.

Is extended warranty taxed differently?

Yes. An extended warranty or annual maintenance contract sold for a separate charge is treated as a distinct supply of service, taxed on its own consideration — separate from a free in-warranty part replacement. Because facts vary widely across bundled and standalone offers, confirm the classification, timing and rate for your specific contracts with a qualified professional.

What evidence does an automotive warranty claim need?

A defensible claim links five things: the job card describing the defect and work done, the VIN or chassis number identifying the vehicle, the part number of the replaced component, proof the defective part was returned or scrapped, and confirmation the failure fell inside the warranty period. Missing any one of these is the most common reason an OEM rejects or short-pays a claim.

Does the Finance Act 2026 change warranty GST treatment?

The Finance Act 2026 carries amendments touching provisions such as Sections 15(3)(b) and 34, and received assent on 30 March 2026 — but those provisions had not been notified into force as of the date of writing. Until the government issues a commencement notification, the existing position continues. Verify the notification status before relying on any change.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

GST and TDS on Automotive Dealer Incentives

How automotive dealer incentives are taxed — credit-note choice under GST and Section 194R TDS on trips, gifts and benefits-in-kind given to dealers.

GST and TDS on Paints Dealer and Painter Rewards

How paints dealer schemes and painter loyalty rewards are taxed — GST credit-note choice and Section 194R TDS on rewards in kind to dealers and painters.

GST on Agri-Input Claims and Schemes

How agri-input dealer schemes, liquidation claims and near-expiry returns are treated under GST — credit-note choice, ITC reversal and mixed input rates.