GST and TDS on Automotive Dealer Incentives

How automotive dealer incentives are taxed — credit-note choice under GST and Section 194R TDS on trips, gifts and benefits-in-kind given to dealers.

Automotive dealer incentives raise two tax questions at once, and they are easy to conflate. The first is how the incentive is settled under GST — as a Section 34 tax credit note, a financial/commercial credit note, or a straight payout. The second is whether Section 194R TDS applies, which it can where the reward is a benefit or perquisite given in kind: the foreign trips, gold coins and gifts that auto schemes so often use. Both answers turn on the same underlying fact — how the benefit is actually given, not what the scheme is called. This piece sits under the broader automotive channel claims and rebates in India guide, which frames where dealer incentives fit alongside warranty and settlement flows.

GST on a dealer incentive: which document?

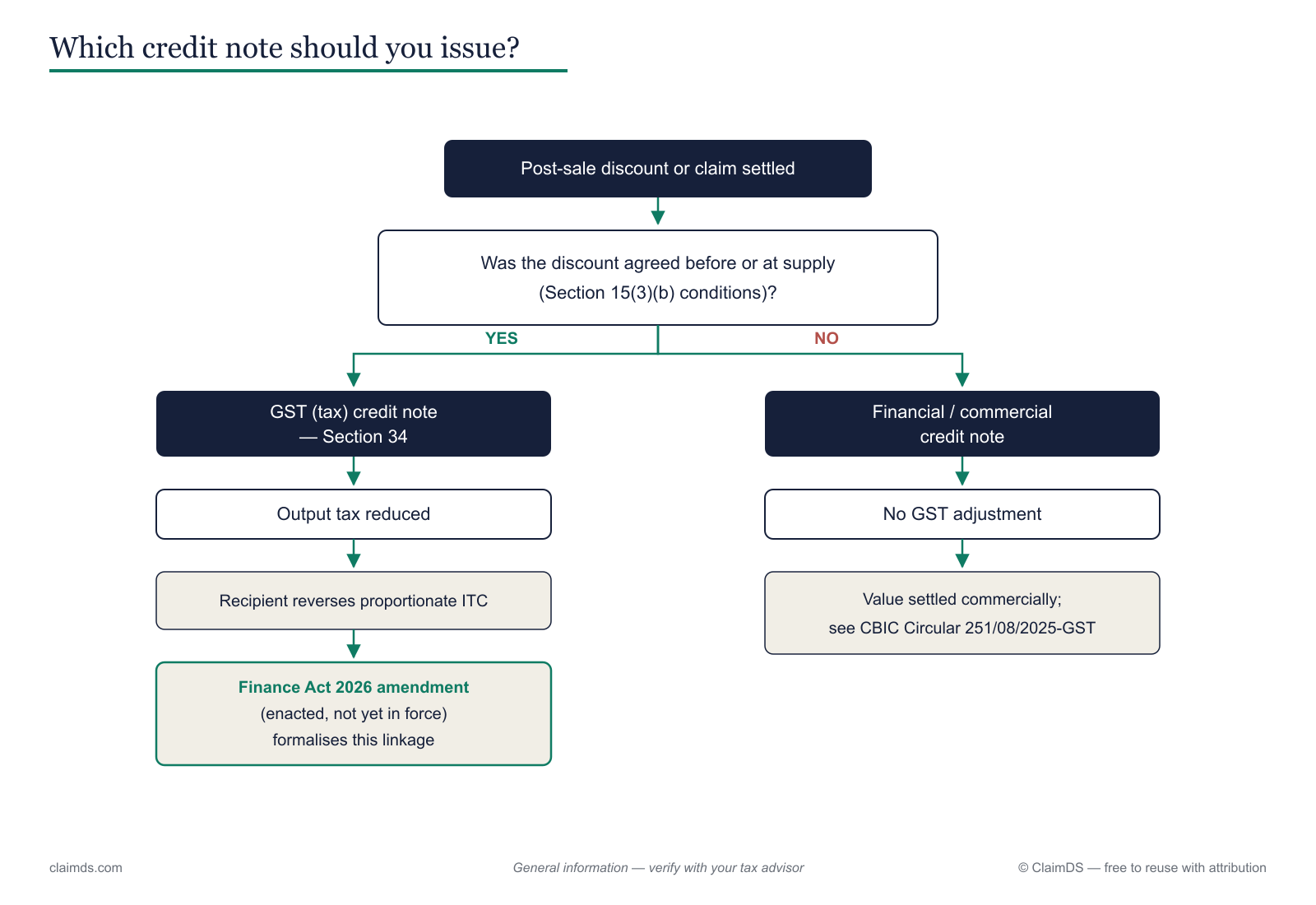

The document that settles a dealer incentive is not a formality. It decides whether tax moves at all, and who has to adjust their books. There are three routes, and an automotive scheme designer has to pick one deliberately.

The first route is a Section 34 tax credit note. This reduces the supplier's output tax on the original supply — but it is only available where the post-supply discount satisfies Section 15(3)(b) of the CGST Act: the discount must have been established in an agreement entered into before or at the time of supply, be linked to specific invoices, and the recipient must reverse the proportionate input tax credit attributable to it. That ITC reversal on the dealer's side flows from Section 17(5)(h) read with Rule 37. If any one of those conditions fails, the tax credit note is simply not the right instrument. <!-- TODO VERIFY AT PUBLISH + CA REVIEW -->

The second route is a financial or commercial credit note. This is used when the discount cannot meet the Section 15(3)(b) conditions — most commonly because it was decided after supply, or cannot be tied invoice-by-invoice. Here the original taxable value and output tax stay unchanged, the supplier books the payment as a commercial settlement, and the recipient-ITC consequence is the key point of relief: the dealer is not required to reverse ITC on a purely financial credit note. CBIC Circular 251/08/2025-GST speaks to this dealer-incentive question at a pointer level — treat its precise scope as something to confirm before you rely on it. <!-- TODO VERIFY AT PUBLISH + CA REVIEW -->

The third route is simply a payout — the manufacturer pays the dealer, with no credit note against a supply at all. This is common where the payment is not a discount on the dealer's purchases but a reward for something else, which is exactly where the in-kind and TDS questions below come in.

The recipient-ITC consequence is what separates the first two routes in practice: a tax credit note forces the dealer to give back ITC; a financial credit note does not. Getting the instrument wrong therefore does not just misstate the supplier's output tax — it can wrongly strip or preserve the dealer's credit. The distinction is unpacked further in the difference between financial and tax credit notes under GST and in when Section 15(3)(b) lets a post-supply discount reduce taxable value.

The document that settles a dealer incentive decides whether it carries tax.

The document that settles a dealer incentive decides whether it carries tax.

For the mechanics of the ITC reversal that a tax credit note triggers on the dealer's side, see ITC reversal on post-sale discounts and credit notes. For how these instruments land when a whole channel is being reconciled, see GST adjustments in channel settlements. The circular itself is summarised in what CBIC Circular 251 says about post-sale discounts.

Section 194R: TDS on benefits and perquisites

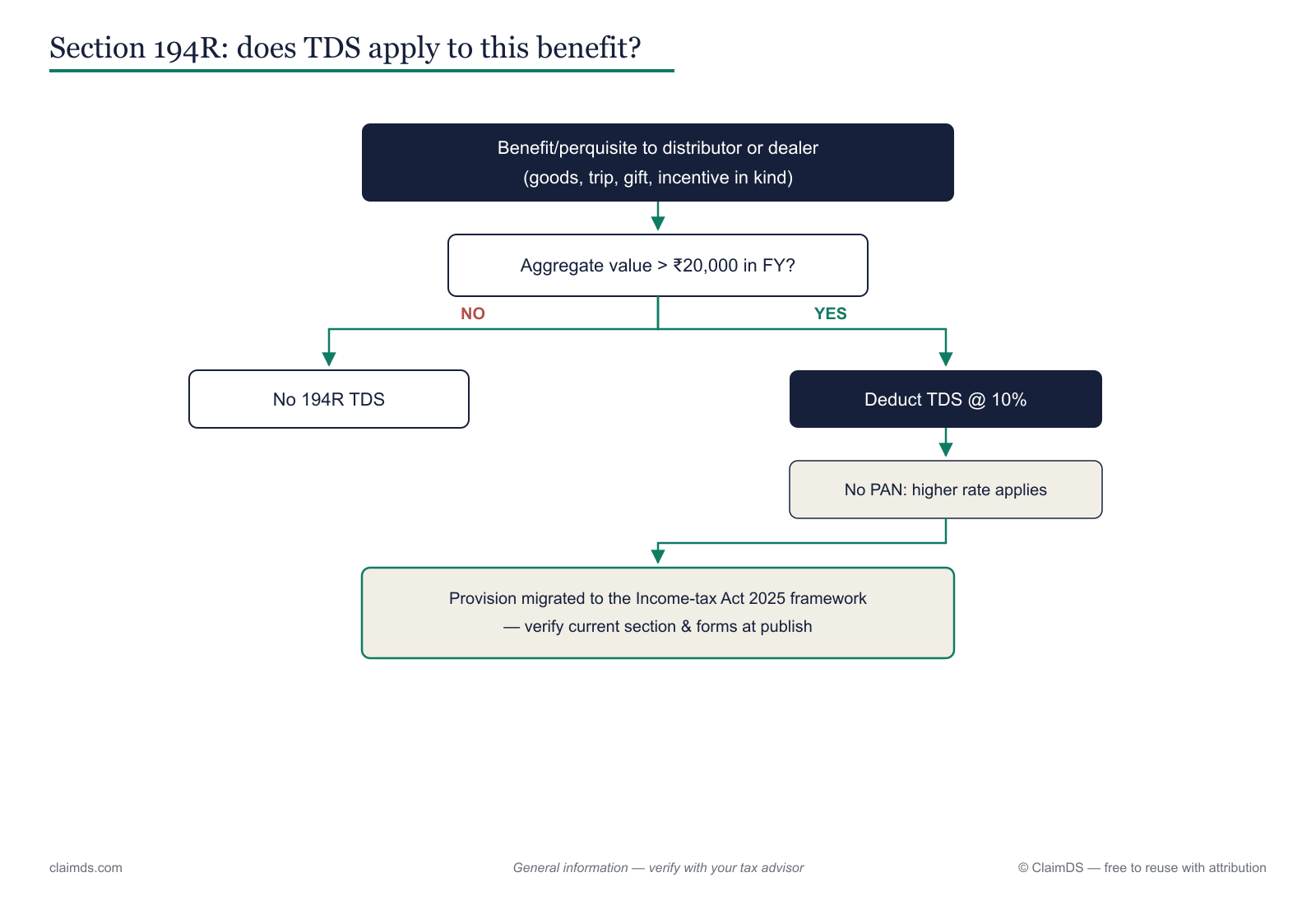

This is the part of automotive dealer incentives that catches finance teams out. Auto schemes are unusually rich in benefits given in kind — foreign trips for hitting a target, gold coins at year-end, gifts, sponsored events — and it is precisely these in-kind rewards that Section 194R is written to reach.

The provision operates on benefits or perquisites, whether convertible into money or not, arising from a business or profession, provided to a resident. Where such a benefit is given to a resident dealer, the payer is required to deduct TDS at 10% of the value of the benefit, once the aggregate value of benefits provided to that dealer exceeds ₹20,000 in a financial year. Where the dealer has not furnished a PAN, a higher rate can apply under the general TDS machinery. <!-- TODO VERIFY AT PUBLISH: 194R rate, threshold, section mapping -->

A benefit in kind to a dealer above the annual threshold attracts Section 194R TDS — the value, not the cash, is what triggers it.

A benefit in kind to a dealer above the annual threshold attracts Section 194R TDS — the value, not the cash, is what triggers it.

The mechanism matters. Because a foreign trip or a gold coin is not cash, there is nothing for the payer to withhold from — so the payer has to ensure the tax on the benefit's value is paid before the benefit is released, or gross it up. This is why in-kind auto schemes are operationally heavier than a plain cash rebate: the value of the benefit, not a cash flow, is what pulls the transaction over the threshold and fixes the deduction. A single dealer receiving several small gifts across a year can cross ₹20,000 in aggregate even if no single item would. <!-- TODO VERIFY AT PUBLISH: 194R rate, threshold, section mapping -->

A further structural point to confirm at publish: the provision now sits within the Income-tax Act 2025 framework, which is stated to take effect from 1 April 2026. The substance carried over from the earlier Section 194R, but the section mapping and cross-references should be re-checked against the 2025 Act rather than assumed. <!-- TODO VERIFY AT PUBLISH: 194R rate, threshold, section mapping -->

The full treatment specific to dealer and distributor rewards — including who deducts, timing, and the gross-up mechanics — is covered in Section 194R TDS on dealer and distributor incentives, and the operational side is set out in the product docs on TDS on incentives. How these benefit-heavy schemes fit the wider reward landscape is discussed in tax on rebates, chargebacks, billbacks and buybacks in India.

Cash discount vs benefit in kind

The same commercial reward — say, a ₹50,000 value for hitting an annual target — can sit in completely different tax boxes depending on how it is handed over, and this is the single most useful distinction for a scheme designer to internalise.

Given as a cash or credit-note incentive, the reward is a price or financial adjustment. The GST question is which credit note applies (tax vs financial, per the section above), and the direct-tax question is whether ordinary TDS on a payment is engaged. It is a movement of money, and it is documented as one.

Given as a benefit in kind — the trip, the gold, the gift — the reward is not a price adjustment at all. There is no supply to discount and no cash to net against; it is a perquisite whose fair value is tested for Section 194R. The GST side may also differ, because in-kind rewards can raise supplier-side ITC questions on gifts under Section 17(5) rather than discount treatment.

The practical structuring consequence is simply this, at a pointer level and not as advice: the form of the reward changes the tax and compliance load, not just its cost. A cash rebate and an equivalent-value foreign trip are not interchangeable from a tax standpoint, and a scheme built on in-kind benefits carries a Section 194R obligation that a cash scheme may not. How the reward is designed upstream is discussed in channel loyalty programs, and the GST-side treatment of discounts and incentives in GST on trade discounts and dealer incentives. The instrument-level walkthrough lives in the credit note documentation.

The Finance Act 2026 note

There is one moving piece to flag rather than rely on. Amendments touching Section 15(3)(b) and Section 34 of the CGST Act were enacted through the Finance Act 2026, which received assent on 30 March 2026. As of this writing those amendments are enacted but NOT yet notified — meaning the relevant provisions have not been brought into force by notification. Until they are notified, the pre-amendment position continues to govern. State this exactly to any reader: enacted, pending notification. Do not apply the amended text as current law until the notification is confirmed. <!-- TODO VERIFY AT PUBLISH -->

Related reading

For the wider automotive channel picture and the sibling topics that dealer incentives connect to:

- Automotive channel claims and rebates in India — the pillar guide to how the auto channel's claims, rebates and incentives fit together.

- Automotive warranty claims — how warranty recoveries are handled alongside incentive schemes.

- The automotive dealer claim settlement process — end-to-end settlement of dealer claims once incentives are agreed.

- Section 194R TDS on dealer and distributor incentives — the deeper TDS walkthrough for in-kind rewards.

- Financial vs. tax credit notes under GST — which instrument settles the incentive and whether tax moves.

- ITC reversal on post-sale discounts and credit notes — the dealer-side credit consequence of a tax credit note.

- Section 15(3)(b) and post-supply discounts and CBIC Circular 251 on post-sale discounts — the two sources that govern the GST document choice.

- GST adjustments in channel settlements, GST on trade discounts and dealer incentives, and tax on rebates, chargebacks, billbacks and buybacks — the wider treatment of channel rewards.

- Product docs: credit note and TDS on incentives.

Disclaimer

This article is general information on the GST and income-tax treatment of automotive dealer incentives in India as understood at the date of writing. It is not tax, legal or accounting advice, and it does not create an adviser-client relationship. Tax law changes, and several points above are expressly marked for verification before publication. Every rate, threshold, section reference and date in this article must be confirmed against the current bare Acts, rules, and CBIC circulars, and reviewed by a qualified Chartered Accountant or Cost Accountant, before you act on any of it. Any 18% or ₹ figure used to illustrate a mechanism is illustrative only. Consult your own adviser for your specific facts.

Ready to see how ClaimDS keeps the credit-note choice and the 194R benefit register straight across an automotive channel? Book a demo.

Frequently asked questions

Is GST applicable on dealer incentives?

It depends on what the incentive really pays for. A routine post-sale discount to a dealer trading on a principal-to-principal basis is not consideration for a supply by the dealer, so no GST arises in the dealer's hands. GST applies only where a specific agreement obliges the dealer to perform defined promotional activities for a defined consideration — verify current treatment against CBIC Circular 251/08/2025-GST at publish.

Which credit note is used for a dealer scheme?

Either a Section 34 tax credit note or a financial/commercial credit note — the choice decides whether tax moves. A Section 34 tax credit note reduces the supplier's output tax and requires the dealer to reverse proportionate ITC under Section 17(5)(h) read with Rule 37, but only where the Section 15(3)(b) conditions are met. If they are not, a financial credit note settles the money with no GST change.

Is TDS applicable on dealer incentives?

Yes, in many auto schemes. Where a benefit or perquisite arising from a business relationship is provided to a resident dealer, Section 194R can require the payer to deduct TDS at 10% once the aggregate value crosses the annual threshold. This is separate from the GST question — verify the rate, threshold and current section mapping under the Income-tax Act 2025 framework at publish.

Is a foreign trip given to a dealer taxable?

A foreign trip is a benefit in kind, and Section 194R is written to capture benefits and perquisites given in kind, not only cash. Where the trip arises from the dealer's business relationship with the payer and the annual aggregate threshold is crossed, TDS provisions can apply on the value of the trip. Confirm the exact treatment and valuation approach with a qualified adviser at publish.

What is the 194R threshold?

Section 194R is drafted so that TDS applies where the aggregate value of benefits or perquisites provided to a resident in a financial year exceeds ₹20,000, with deduction at 10% of the value. Where the recipient has not furnished a PAN, a higher rate can apply. Treat these figures as verify-at-publish — the section now sits within the Income-tax Act 2025 framework.

Does the value or the cash trigger 194R?

The value does. Section 194R is designed to capture benefits and perquisites in kind — gold coins, gifts, sponsored trips — precisely because no cash changes hands for the payer to deduct from. It is the fair value of the benefit that is tested against the annual threshold, which is why in-kind auto schemes so often bring the provision into play. Verify the valuation basis at publish.

How is a cash discount taxed differently from an in-kind benefit?

A cash or credit-note incentive is settled as a GST price adjustment or a financial settlement, and the TDS question turns on the payment's nature. An in-kind benefit — a trip, gold, a gift — is not a price adjustment at all; it is a perquisite whose value can attract Section 194R TDS. The same reward can therefore sit in very different tax boxes depending on how it is given.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Automotive Warranty Claims: Process and GST

How automotive warranty claims work and are taxed — the claim and reimbursement process, and the GST treatment of warranty replacements under Circular 216.

GST and TDS on Paints Dealer and Painter Rewards

How paints dealer schemes and painter loyalty rewards are taxed — GST credit-note choice and Section 194R TDS on rewards in kind to dealers and painters.

GST on Agri-Input Claims and Schemes

How agri-input dealer schemes, liquidation claims and near-expiry returns are treated under GST — credit-note choice, ITC reversal and mixed input rates.