Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.

Crop-protection stock has a shelf life, and agri-input schemes are season-bound, so unsold product comes back up the channel as a return. It arrives in three shapes — near-expiry stock approaching the end of its shelf life, season-end stock left unliquidated when a crop cycle closes, and damaged or leaking stock that can no longer be sold. Each one is declared by the dealer, verified against an agreed claim window, and settled either by replacement with fresh product or by a credit note. This is the operations guide to running that return side.

Returns are not an edge case in agri-inputs — they are a high-volume, recurring claim type that sits alongside the scheme claims on the agrochem channel-claims pillar. If you handle the front half of the cycle well but treat returns as an afterthought, the return side is where revenue leaks out and where distributor claims quietly pile up unreconciled.

Near-expiry and expiry returns

Every crop-protection product carries a manufacturing and expiry date, and that shelf life is the clock the whole return runs on. As a batch approaches expiry, the stock still sitting with a dealer or super stockist becomes a near-expiry return — product that has not sold and now needs to come back before it is unsaleable.

Most companies define a near-expiry window — say, stock within a set number of months of its expiry date — as the point at which a return becomes eligible. Inside that window the stock is usually still saleable, so it can be pulled back, redistributed to a market with live demand, or swapped for a fresh-dated batch. That is the cheaper outcome for everyone: the product still has value.

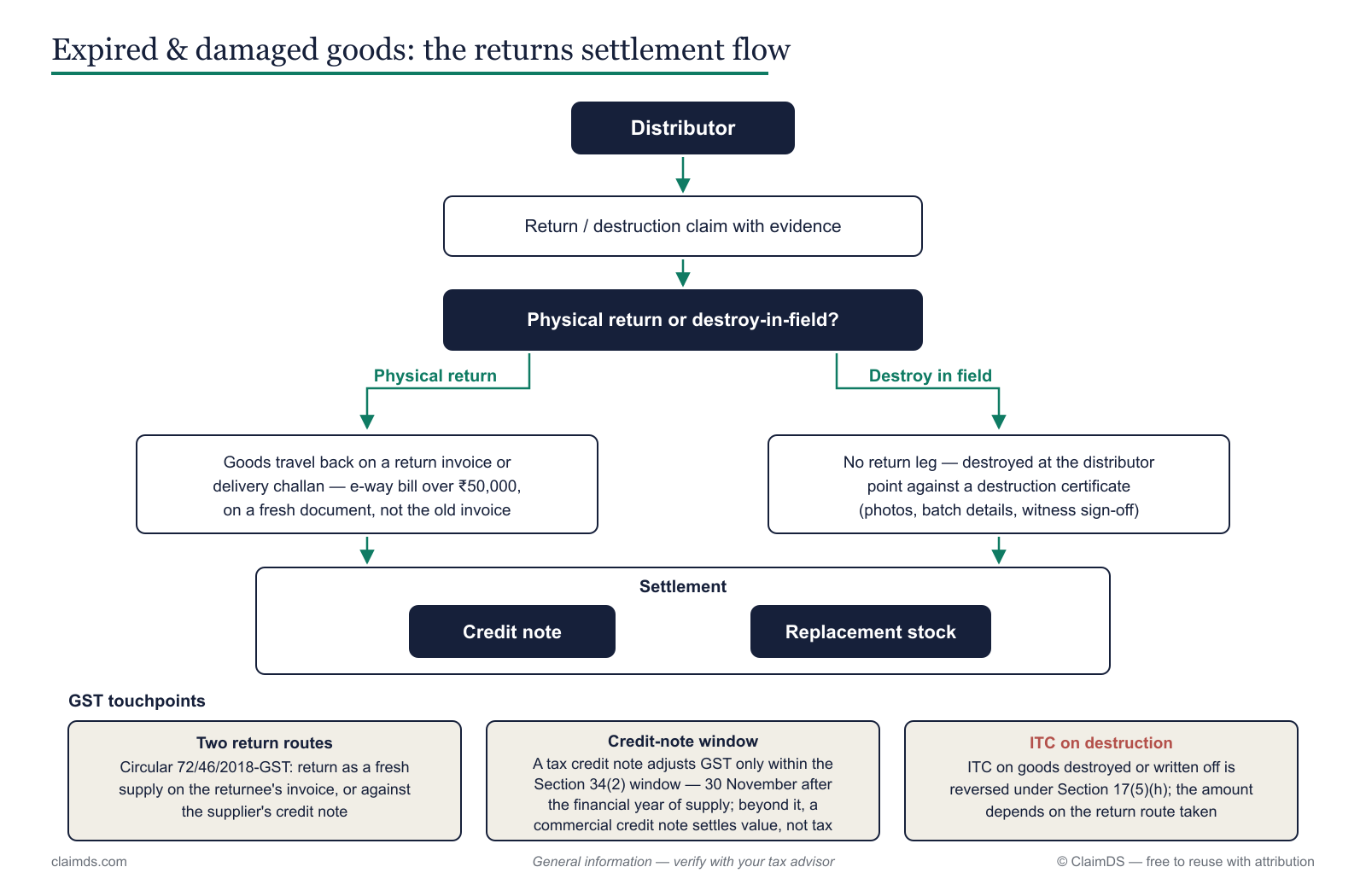

Near-expiry and damaged agri-input stock flows back up the channel as a return claim.

Once a batch crosses its expiry date it becomes an expiry return — non-saleable stock that cannot re-enter inventory under any circumstances. Selling expired crop-protection chemicals is not an option, so this stock is destroyed under a documented process rather than redistributed. That single distinction — saleable versus non-saleable — decides how the return settles.

A saleable near-expiry return settles by replacement: fresh stock goes out, the returned batch comes back, and stock records move on both sides. A non-saleable expiry return settles by credit note, because there is no fresh product to swap for destroyed goods — the company simply adjusts the original sale value. Getting this classification right at the point the return is declared is what keeps the physical, financial and tax trails aligned later. The glossary entry on returns terms is a quick reference when the language gets slippery between teams.

Season-end and unliquidated-stock returns

When a crop season closes, whatever has not sold becomes unliquidated stock — and because agri-input demand is seasonal, that stock may have no immediate buyer. A herbicide dispatched for the kharif season has a narrow demand window; if it does not move before the season ends, it sits in the channel until the next relevant cycle, which may be a full year away.

This is where the return side links directly to liquidation schemes. Those schemes exist precisely to push stock out of the channel before season-end so it does not become a return in the first place. When they fall short, the residue becomes a season-end return — the dealer declares the closing stock at the cut-off date, and the company decides whether to take it back, carry it forward, or fold it into a fresh scheme for the next season.

Accurate stock declaration at the cut-off is the load-bearing step here. The whole settlement rests on the dealer's declared closing stock being true, because that number is what the return is verified against. If it is wrong, every downstream figure is wrong. This is also where the fraud risk concentrates: an inflated return — declaring more unsold stock than physically exists, or claiming stock that was actually sold — is one of the easier ways to extract undue credit. That is why the declared quantity is reconciled against dispatch records, prior claims and sell-through data before anything settles, and why season-end returns typically carry a higher approval bar than a routine replacement. Treating the declaration as a claim to be verified — not a number to be accepted — is the core control. The same discipline that governs returns and reversals across channel claims applies with extra force at season-end, when volumes spike and pressure to clear the channel is highest.

Damage and leakage returns

Liquid crop-protection formulations travel in bottles and cans, and they break, leak and spoil in transit and storage — so damage returns run alongside the expiry and season-end streams the whole year. A carton crushed in a warehouse, a can that corrodes and leaks, a seal that fails — all of it turns saleable stock into a return that has nothing to do with shelf life or season.

The distinguishing feature of a damage return is that it turns on evidence of the damage itself, not on a date. The dealer has to show what came back and why it is unsaleable: photographs of the broken or leaking stock, the batch numbers involved, the quantity, and often a note on where in the chain the damage occurred, since that can determine who bears the cost. Damage caught at the point of delivery is treated differently from damage discovered in the dealer's own storage weeks later.

Settlement follows the same fork as expiry returns. If the damage is partial and some stock is still saleable, that portion may settle by replacement — fresh stock for the damaged units. Where the stock is a total loss and must be written off, it settles by credit note against the original sale value, and the damaged goods are destroyed under the same documented process used for expired stock. Because damage returns are easy to overstate, the evidence bar sits high: a claim without batch data and proof of the physical damage is a claim the company cannot verify, and unverifiable damage claims are exactly the kind of deduction that best-practice teams learn to challenge.

How returns settle under GST

Every one of these returns is, in tax terms, a credit-note event — but the operations team should treat the GST mechanics as a pointer, not a task to work out here. When a return settles by credit note rather than replacement, that credit note is the document that adjusts the original sale, and whether it is a purely financial credit note or a tax credit note changes what actually happens to the tax already charged.

Two threads matter enough to name and then route onward. First, the difference between a financial and a tax credit note determines whether the tax on the original sale is adjusted or left untouched — a distinction that also drives price-protection and rate-difference credit notes on the scheme side. Second, when stock is destroyed rather than returned for resale, there is an input-tax-credit consequence attached to that written-off inventory that the finance team has to handle correctly.

Neither belongs in the returns desk's day-to-day. The full mechanics live in the guide to credit notes for expired and damaged goods returns, and the agri-input-specific tax treatment sits in GST treatment of agrochem claims and schemes. The operations rule is simply this: know that a settled return will generate a credit-note event, capture the data that lets finance issue the right document, and route the tax question to the people who own it.

Evidence and audit trail

A returns claim stands or falls on its evidence, and the evidence needed differs by return type. The reversals-explained reference covers how a settled return is unwound if it later proves wrong; the table below is the checklist for getting the return right the first time.

| Return type | Core evidence | Claim window test | Typical settlement |

|---|---|---|---|

| Near-expiry (saleable) | Stock statement, batch and expiry data, sale reference | Within near-expiry window | Replacement |

| Expiry (non-saleable) | Stock statement, expiry proof, destruction certificate | Past expiry, inside return policy | Credit note |

| Season-end unliquidated | Declared closing stock, dispatch and sell-through records | At or before season cut-off | Credit note or carry-forward |

| Damage / leakage | Photographic proof, batch data, damage location | Within damage-claim window | Replacement or credit note |

Across all four, three things are non-negotiable: a stock statement that ties the return to a real, quantified batch; batch and expiry data that proves the goods actually qualify for the return type claimed; and, for anything destroyed, destruction proof — a certificate or dated photographs. The fourth control is the claim window itself: a genuine return declared after the window has closed becomes a commercial exception rather than an automatic claim. Keeping this evidence linked to the original sale is what separates a return that reconciles cleanly from one that surfaces months later as an unexplained gap — the same weakness that lets scheme and claim value leak when the trail is thin. This is also the discipline that a proper rebate-management platform is built to enforce, so the evidence lives with the claim instead of in someone's inbox.

Returns are not the tidy end of the agri-input claim cycle — they are where shelf life, seasonality and physical handling all collide, and where a thin audit trail costs real money. If you want to see how declaring, verifying and settling every return in one place closes that gap — including the handoff into dealer claim settlement — book a demo.

Frequently asked questions

What is a near-expiry return in agri-inputs?

A near-expiry return is crop-protection stock that has not sold and is close to the end of its shelf life — inside the window a company agrees to take it back before it expires. The dealer declares the batch, the company verifies expiry data against its claim window, and the stock settles by replacement with fresh product or a credit note.

What is a season-end return?

A season-end return is stock left unsold when a crop season closes — the unliquidated inventory sitting in the channel after demand ends. Because agri-input schemes are season-bound, this stock has no immediate buyer and may be returned or carried forward. The dealer declares the closing stock at the cut-off, and the company verifies it against sales and dispatch records before settling.

How is destroyed or expired stock settled?

Expired or unsaleable stock that cannot re-enter inventory is destroyed under a documented process, and the return settles by credit note rather than replacement — there is no fresh stock to swap. The dealer submits destruction proof and batch data, the company verifies the quantity against the claim window, and issues the credit note against the original sale value.

What evidence does a returns claim need?

A returns claim needs a stock statement showing the returnable quantity, batch and expiry data proving the goods qualify, the original sale reference, and — for destroyed stock — a destruction certificate or photographic proof. The claim must fall inside the agreed return window. Missing batch or expiry data is the most common reason a genuine return is held or rejected.

Why do agri-input companies cap the return window?

A capped return window stops open-ended liability. Without a cut-off, a dealer could send back stock long after a season on any pretext, and the company could never close its books. The window ties each return to a shelf-life or season-end date, so both sides know the deadline. Stock declared after the window closes generally settles as a commercial exception, not an automatic claim.

How is a saleable return different from an expiry return?

A saleable return is stock still fit for resale — undamaged, in date, in original packaging — so it re-enters inventory and the sale value simply adjusts. An expiry return is stock too close to or past its shelf life to resell, so it is destroyed and settles by credit note. The batch and expiry data decide which path a return takes.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Channel Claims and Rebates in Indian Automotive

How claims, incentives and warranty work in the Indian automotive channel — the OEM and dealer network, aftermarket parts, warranty claims and settlement.