Seasonal Schemes and Liquidation in Agri-Inputs

How seasonal schemes and liquidation claims work in Indian agri-inputs — schemes timed to Kharif and Rabi, sell-through targets and season-end settlement.

Agri-input schemes are timed to the crop season, and the defining one is the liquidation scheme. A liquidation scheme rewards the dealer or distributor for actually selling stock through to the farmer — sell-through — before the season ends or the product nears expiry, not merely for buying it from the company. The crop calendar sets the window and the product's shelf life sets the deadline. Together they make liquidation the industry's signature claim, with no clean equivalent in verticals where stock does not expire on a season.

All numbers below are illustrative, not benchmarks. Your scheme circular always governs.

Why do agri-input schemes follow the crop calendar?

Nothing in agri-inputs sells on a flat monthly curve. Demand is dictated by sowing, and sowing follows the crop calendar. India runs three broad cropping seasons, and a crop-protection or fertilizer company plans its entire scheme year around them.

Kharif is the monsoon-sown season — the crop goes in with the rains from around June and is harvested after the monsoon. It is the largest window for many inputs, and the one most exposed to a late or failed monsoon. Rabi is the winter-sown season, planted from around October on residual moisture and irrigation, harvested in spring. Zaid is the short summer season between the two, smaller and irrigation-dependent. Each has its own crop mix, its own pest and nutrient profile, and therefore its own product demand.

Because the farmer buys only in a narrow sowing window, the channel has to be stocked before that window opens. So the scheme year runs ahead of the crop. Pre-season stocking schemes place product into distributors and dealers weeks before sowing, so material is on the shelf when the farmer walks in. Advance-booking and early-bird schemes reward the channel for committing and lifting stock early, giving the company production visibility and a funded pipeline. Then, as sowing peaks, the incentive shifts from stocking to moving that stock out.

The consequence is that a scheme's live window is short and calendar-locked. Miss the sowing window and the demand is simply gone until the next season — you cannot recover Kharif volume in the off-season. This is why agri-input scheme design is unusually disciplined about dates, and why the claim window after each scheme is treated as strictly as the scheme itself. For the wider taxonomy of scheme structures this sits inside, see types of trade schemes in India.

What is a liquidation scheme?

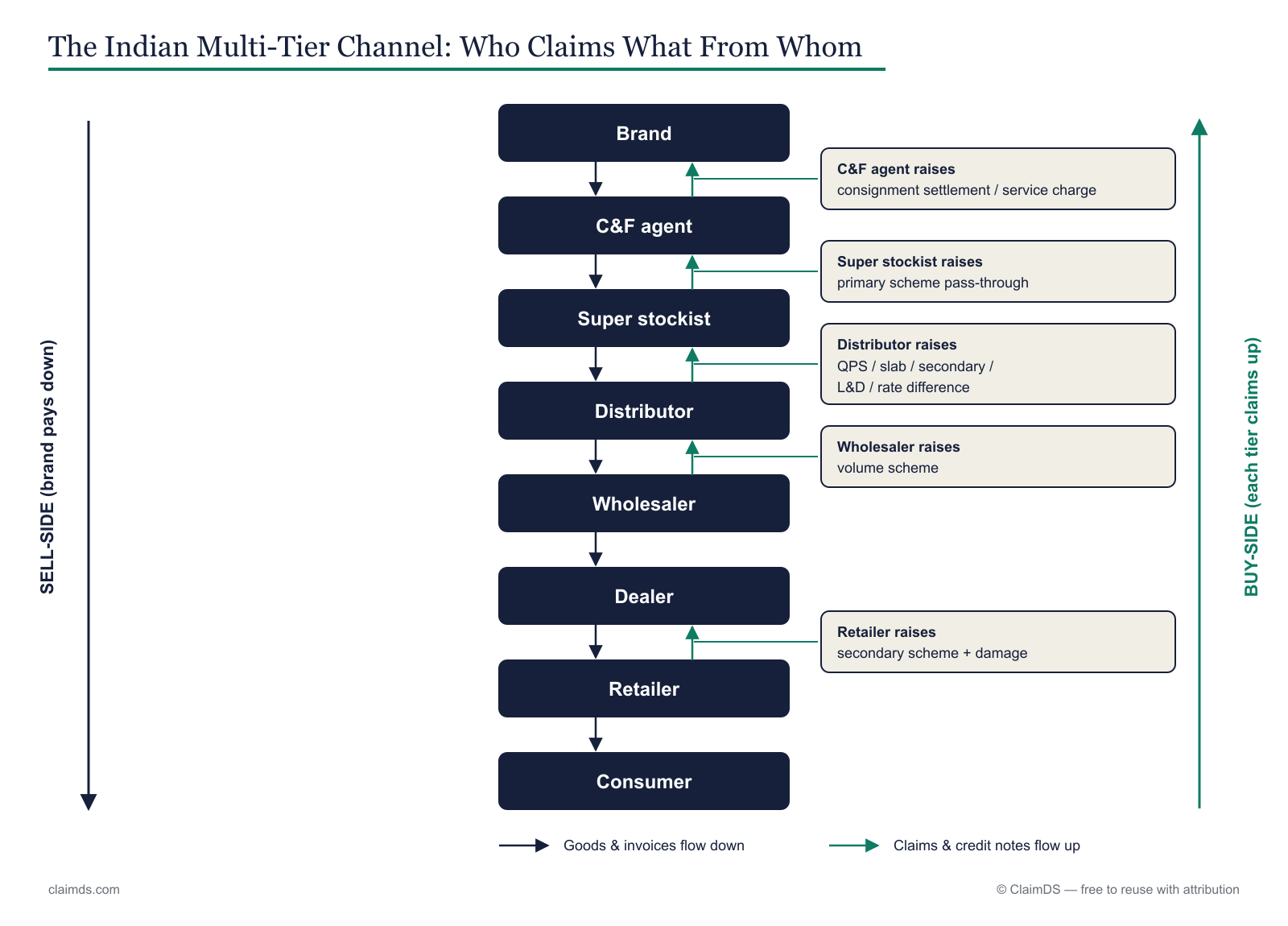

To see what liquidation means, separate the two layers of the route to market. The primary sale is the company selling to the distributor — stock leaves the plant or depot and enters the channel. That is the sale the company invoices, and a pure primary scheme (a slab or purchase scheme) pays the distributor for lifting it. The problem is that a primary sale only proves the distributor bought, not that anyone used.

The liquidation layer sits below that. Liquidation — also called the sell-through layer — is the movement of stock from the dealer or retailer onward to the farmer. A liquidation scheme pays for that onward movement: the reward is earned only when the product actually leaves the channel into the field. It is the tertiary sale, one step past the secondary sale from distributor to retailer.

Liquidation rewards the sell-through to the farmer — the layer below the primary sale.

Why does the company pay for liquidation at all, when it has already booked the primary sale? Two reasons, both specific to this industry. First, channel stuffing: if schemes reward only primary purchase, distributors over-lift to chase slabs, and stock piles up faster than the field consumes it. Second, shelf life: crop-protection stock that sits unsold does not wait forever — it moves toward expiry, and near-expiry stock comes back as returns the company has to absorb. Paying on liquidation solves both. It tells the company that demand is real, it drains the pipeline before expiry, and it stops the channel from booking volume it cannot sell.

Liquidation is claimed on evidence of sell-through rather than on a purchase invoice. The dealer or distributor reports what actually moved to farmers in the scheme window, the company validates it, and the benefit settles — typically through a credit note against the distributor's account rather than cash. Because the claim rests on downstream data the company does not directly own, liquidation is also the scheme most exposed to weak evidence, which is the next problem to design around. This full mechanic is covered in the agri-input channel claims and rebates pillar.

What sell-through evidence proves liquidation at the season cut-off?

A liquidation claim is only as good as its proof of sell-through. Since the company cannot see the farmer's purchase directly, it relies on downstream data and a stock reconciliation at the season cut-off — the date the scheme closes and unsold stock is counted.

The core evidence types:

| Evidence | What it proves | Watch-out |

|---|---|---|

| Retailer / farmer-level sales records | Stock reached the last mile, not just the distributor | Only as reliable as the retailer's record-keeping |

| Point-of-sale (PoS) data | Transaction-level movement out of the counter | Coverage gaps where dealers are not digitised |

| Stock declaration at cut-off | Opening stock + purchases − closing = liquidated | Closing count can be understated to inflate the claim |

| Batch / expiry references | Ties movement to specific lots and shelf life | Missing on manual claims; needed for the returns link |

The reconciliation is the anchor: opening stock plus purchases in the window, minus verified closing stock, equals what liquidated. Get an honest closing count and the claimable quantity falls out of it.

The fraud and channel-stuffing risk is real here. A distributor who wants to bank a liquidation payout can understate closing stock, or report farmer sales that did not happen, to make the pipeline look drained. That is exactly the stock that later returns as near-expiry — so the near-expiry link is not a side issue, it is the tell. A batch nearing its expiry date that is still physically in the godown, while the claim says it liquidated, is the contradiction a clean process is built to catch. Consistent, reconciled evidence closes that leak, which is why structured claim data collection matters more in agri-inputs than in most channels.

How does liquidation tie to returns and price protection?

Liquidation and returns are two ends of the same stock. Whatever does not liquidate by the season cut-off is the company's downstream problem — and in agri-inputs that problem has a deadline the calendar and the shelf life set together.

Unliquidated stock at season-end takes one of two routes. It comes back as a return — physically reversed out of the channel, often because it is damaged or approaching expiry — or it is compensated in place through price protection, where the company issues a rate-difference credit note so the distributor is not stuck holding stock bought at a price the next season will undercut. Both are claims in their own right, and both are downstream of a liquidation scheme that did not fully clear the pipeline.

This is why the three mechanics are best designed as one system rather than three unrelated forms. A liquidation scheme that works reduces the expiry, damage and season-end returns that follow, and reduces the price protection the company has to fund on stranded stock. The accounting for the reversals themselves runs through credit notes for expired, damaged and returned goods. And the GST treatment across schemes, returns and price protection has to be consistent — handled at pointer level in GST treatment of agri-input claims and schemes, not restated here. The settlement of the season's dealer claims sits in the agri-input dealer claim settlement process.

How do you design a clean seasonal scheme?

A seasonal scheme is clean when three things are unambiguous before the season opens.

A clear window. State the exact scheme period against the crop season — when it opens for stocking, when the cut-off falls, and the claim submission window after it. Because the crop, not the quarter, sets these dates, they must be fixed up front and communicated to every tier. A shared view of open windows is worth as much as the arithmetic.

A clear sell-through metric. Say precisely what is being rewarded — primary lift, secondary movement, or tertiary liquidation to the farmer — and on what base it is computed. Mixing the layers is where disputes start. If the scheme pays on liquidation, the base is verified sell-through, full stop.

Clear evidence. Name the proof each claim must carry, matched to the metric: farmer or retailer sales, PoS data, the cut-off stock declaration, batch references. When the evidence standard is set with the circular, most claim-time arguments never happen.

Fund the window against the scheme budget deliberately, route every claim through a defined approval workflow, and the season settles as a controlled flow. For the terminology across all of this, the product glossary defines each term in a line.

Bringing it together

Seasonal schemes and liquidation are the mechanic that makes agri-input claims their own discipline. The crop calendar sets a short, unrepeatable window; the product's shelf life sets a hard deadline; and liquidation — paying for genuine sell-through to the farmer — is what keeps the channel from stuffing a pipeline it cannot clear. Get the window, the metric and the evidence right, and the season's distributor claims settle cleanly instead of unwinding into returns and disputes.

This sits inside the broader picture of channel rebates in India and the agri-input channel claims pillar, and the distributor, dealer and super-stockist tiers each play a defined role in it. Running the whole season — scheme terms, sell-through evidence, liquidation claims and GST-ready settlement — in one place is what rebate management software is for, and it is how channel claim programs across FMCG and agri-inputs move from a season-end scramble to a controlled flow. If you are new to the vocabulary, what a rebate is covers the basics.

To see it working on your own crop calendar, scheme windows and liquidation claims, book a demo.

GST note: This article is general information, not tax or legal advice. Where settlement involves GST credit notes or price-protection adjustments, positions must be re-verified at publish time with a qualified professional.

Frequently asked questions

What is a liquidation scheme in agri-inputs?

A liquidation scheme rewards a dealer or distributor for selling stock through to the farmer before the season ends or the product nears expiry — not merely for buying it from the company. It targets sell-through, the movement out of the channel into the field, so the company pays for genuine demand rather than pipeline loading that returns later as unsold stock.

How are seasonal schemes timed to the crop calendar?

Indian agri-input demand follows three cropping seasons — Kharif from the monsoon sowing, Rabi in winter, and Zaid in summer. Schemes open before each season to place stock, then shift to liquidation as sowing peaks, and close at the season cut-off. The live window is short and fixed by the crop, not by the fiscal quarter.

What is sell-through in agri-inputs?

Sell-through is the volume that actually leaves the channel into the farmer's hands, measured at the retailer or farmer level rather than at the company's despatch. It is the tertiary sale, distinct from the primary sale into the distributor. Liquidation schemes pay on sell-through because it reflects real field consumption, not stock parked in a godown waiting for demand.

What evidence does a liquidation claim need?

A liquidation claim needs proof that stock reached the farmer — retailer or farmer-level sales records, point-of-sale data, and a stock declaration at the season cut-off reconciling opening stock, purchases, and closing balance. Batch and expiry references tie the movement to specific lots. Weak evidence invites channel-stuffing disputes and near-expiry returns that surface after the window closes.

How does liquidation relate to expiry and returns?

Crop-protection products and some fertilizer grades carry a shelf life, so stock that does not liquidate by season-end risks nearing expiry. Unsold stock then flows back as returns or is compensated through price protection. A working liquidation scheme reduces both, which is why companies increasingly fund the sell-through layer rather than the primary purchase alone.

What is channel stuffing and why does liquidation prevent it?

Channel stuffing is loading distributors with more stock than the market can absorb, to book primary sales and inflate short-term numbers. It strands near-expiry stock in the channel, which returns later as claims. Paying on liquidation — verified sell-through to the farmer — aligns the incentive with real demand and curbs the practice at its source.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

FMCG Trade Schemes Explained: QPS, Slab and Secondary

The trade schemes Indian FMCG companies actually run — QPS, slab, secondary, display and festive schemes — what each is calculated on and how it settles.

Types of Trade Schemes in India: The Complete Guide for Manufacturers and Channel Teams

Slab, QPS, target, display, visibility, tour, gift and secondary schemes — how each type is calculated, settled and taxed, with worked ₹ examples.

Channel Loyalty Programs for Dealers and Distributors: Design, Points and Settlement (India)

How channel loyalty programs work in the Indian route-to-market — earn rules, tiers, points economics, redemptions, and the settlement layer underneath.