Channel Claims and Rebates in Indian Pharma

How claims, schemes and returns work in Indian pharma distribution — the CFA and stockist channel, expiry and breakage returns, schemes and settlement.

In Indian pharma the company sells through a C&F agent (carrying and forwarding agent) to super stockists and stockists, who sell on to chemists and pharmacies. The money that flows back up the channel is dominated by expiry and breakage returns, alongside trade schemes. Unlike most sectors, every claim here is tied to a batch number and an expiry date — and managing that batch, expiry and credit-note trail is exactly where pharma channel money quietly leaks.

What is the Indian pharma distribution channel, tier by tier?

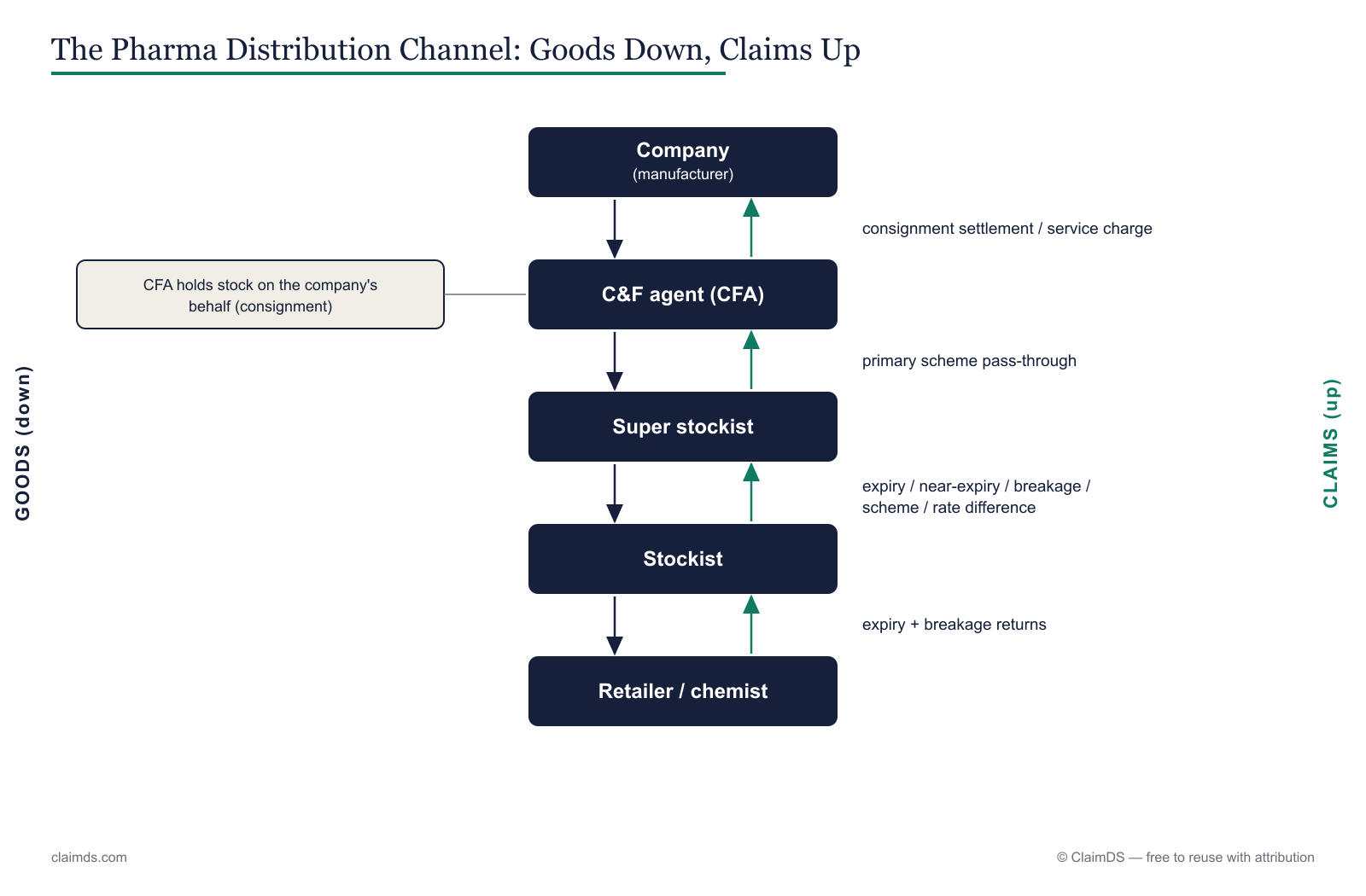

Pharma rarely moves in a straight line from plant to patient. It passes through a licensed, batch-tracked distribution channel, and each tier earns something different and claims it from someone different. Knowing who sits where is the prerequisite for reading every claim that follows.

At the top, the company (the manufacturer or marketing company) owns the brands, prints the MRP, declares the schemes, and carries the ultimate liability for every claim. It almost never ships directly. Instead it appoints a C&F agent in each state — a logistics partner who holds stock in a depot on the company's behalf and dispatches against orders.

The C&F runs on a consignment model, and this is the detail that trips up newcomers: the goods sitting in the C&F depot still belong to the company. The C&F has not bought them. It holds them, insures them, and dispatches them, earning a handling and freight fee rather than a trading margin. Ownership — and the tax point — passes only when stock is billed onward to a stockist. That is why a claim tied to depot stock is the company's exposure, not the C&F's.

Below the C&F, a super stockist buys stock and redistributes it to smaller stockists across a wide or hard-to-service geography. The stockist (also called the distributor) is the workhorse: it buys from the company or super stockist, holds batch-wise inventory, services a beat of chemists, and funds most schemes at the counter. At the base sits the retailer — the neighbourhood chemist or pharmacy that dispenses to the patient.

Running alongside is the hospital and institutional channel — hospital pharmacies, government tenders and large buyers — which is often supplied on separate rate contracts and claims through chargebacks rather than trade schemes, a mechanic covered in chargebacks in pharma distribution.

| Tier | What it does | What it claims | From whom |

|---|---|---|---|

| Company | Owns brands, sets MRP, declares schemes | Nothing (settles claims) | — |

| C&F agent | Holds and dispatches consignment stock | Handling and freight fees | Company |

| Super stockist | Redistributes across geography | Margin, schemes, returns | Company |

| Stockist / distributor | Services chemist beat, funds schemes | Expiry, breakage, schemes, rate difference | Company / super stockist |

| Chemist / pharmacy | Dispenses to patient | Scheme benefit, near-expiry return | Stockist |

| Hospital / institution | Bulk dispensing, tenders | Chargeback vs contract price | Company / stockist |

If these roles blur together in your own network, the difference between a distributor, dealer and super stockist unpacks them in full, and the India multi-tier channel claim map shows how claims route across the tiers.

What do pharma companies settle with their channel?

Pharma companies settle several distinct claim types with their channel, and lumping them together is the first mistake most manual processes make. Each has its own evidence, its own validation rule, and its own settlement path — so the useful move is a clean taxonomy that routes each one to the right place.

Expiry and near-expiry returns are the largest bucket by value. Stock that reaches, or approaches, its printed expiry date unsold is sent back up the channel for credit or replacement. Because it dominates pharma channel money and follows a strict batch-level route, it gets its own deep dive in pharma expiry and breakage returns.

Breakage and damage covers stock that arrived or became broken, leaked or crushed — a reimbursement for a loss the channel absorbed, not a performance reward. Evidence is physical: photographs, batch numbers, and often a destruction certificate.

Saleable versus non-saleable returns is the split that decides what happens to the goods. A saleable return comes back in resaleable condition and can re-enter inventory; a non-saleable return is expired or damaged and must be destroyed and written off. The credit notes for expired and damaged goods returns piece walks through the paperwork on both.

Trade schemes are the performance bucket — quantity offers, bonus stock and target incentives that reward buying or selling more. The broader family is catalogued in types of trade schemes in India, and the hardest counter-funded variant in secondary scheme settlement.

Rate-difference and price-revision claims protect the channel when a company changes its price. Stock already held at the old rate would otherwise lose margin overnight, so the company reimburses the difference on documented closing stock.

Display and visibility payments reward a chemist or stockist for executing merchandising — a branded shelf or counter unit — settled against dated proof of execution.

The buy-side mirror of all this — where the stockist claims a rebate or margin support from the company on its own purchases rather than passing a benefit down — is a channel of its own, and is covered in supplier and purchase rebates in Indian pharma.

What pharma vocabulary will you see on claim forms?

Pharma claim forms are dense with abbreviations, and a wrong reading of any one of them settles the wrong number. The table below is a clean, quotable reference for the terms that recur on almost every claim, invoice and credit note in the channel.

| Term | What it means |

|---|---|

| CFA / C&F | Carrying and forwarding agent — holds consignment stock in a depot and dispatches for the company on a fee. |

| Super stockist | Wholesaler who buys and redistributes to smaller stockists across a geography. |

| Stockist | Licensed distributor who supplies chemists in a territory and files most channel claims. |

| PTR | Price to retailer — the rate at which a stockist sells to a chemist. |

| PTS | Price to stockist — the rate at which the company or C&F sells to the stockist. |

| MRP | Maximum retail price — the printed ceiling price to the patient, set by the company. |

| Batch number | The manufacturing lot identifier; every claim is tied to it. |

| Expiry date | The date after which a batch cannot be sold; the trigger for expiry returns. |

| Saleable return | Stock returned in resaleable condition that can re-enter inventory. |

| Non-saleable return | Expired or damaged stock that must be destroyed and written off. |

| Near-expiry | Stock close to expiry, often returned early under a defined window. |

| Breakage | Physically broken, leaked or crushed stock claimed as damage. |

| CD | Cash discount — a deduction for early or prompt payment. |

| Margin | The difference between a tier's buy and sell price (for example PTS to PTR). |

Every one of these also appears in the product's own glossary, which stays in step with how ClaimDS labels each field on a claim.

Why are pharma claims harder than they look?

Pharma claims look like ordinary channel claims until you try to settle one at scale. Five structural features make them materially harder than FMCG or general distribution, and each carries a direct consequence.

Batch and expiry tracking is mandatory. Every unit is tied to a batch number and an expiry date, and a claim that cannot name the batch cannot be validated. The consequence: your claim data has to reconcile against batch-level dispatch records, not just product and quantity.

Expiry returns dominate the flow. Where other sectors are driven by performance schemes, pharma money runs backward through returns. The consequence: your largest single exposure is inventory you already sold, coming back for credit.

Schemes and margins sit inside a price-controlled market. PTR, PTS and MRP are printed, and some molecules fall under price control, so scheme design cannot freely move the headline price. The consequence: incentives get expressed as bonus stock and rate difference, which are fiddlier to validate than a flat discount.

Evidence is batch-level and paper-heavy. Expiry and breakage claims travel with photographs, batch lists, expiry dates and destruction certificates. The consequence: validation is a document-matching exercise before it is a finance one, and missing paper stalls settlement.

Settlement crosses a GST document decision. Whether a claim closes as a tax credit note or a financial credit note changes input tax credit for both sides. The consequence: the same rupee amount can be right or wrong depending on the instrument, so the tax call is part of the claim, not an afterthought — the reasoning is in financial versus tax credit notes under GST.

A claim moving through validation and approval before settlement.

Getting these five under control is a data-and-evidence discipline, and the same discipline underlies good deduction management practice across every channel.

How does settlement actually happen?

Once a claim is filed, the path is the same regardless of type: claim → validation → approval → credit note or replacement. The stockist (or super stockist) raises the claim with its supporting evidence — batch numbers, expiry dates, scheme reference or photographs. Validation checks the claim against the underlying records: the batch was really supplied, the scheme really applied, the return really qualifies. Approval applies the commercial sign-off and any caps. Only then does settlement issue.

Settlement itself takes one of two forms. Most claims close by credit note against the stockist's account, offsetting future purchases rather than moving cash. Expiry and breakage claims are sometimes settled by replacement stock instead, especially where the company would rather keep the channel filled than push out a credit. A single claim can even split across both — part credited, part replaced — which is why the settlement record has to carry the instrument, the value and the batch trail together rather than a single lump sum. An illustrative expiry claim might book, say, ₹40,000 against returned batches: some of it reversed as a tax credit note, the rest issued as fresh stock.

The tax decision rides on top of that. Whether settlement uses a tax credit note (which reverses GST and adjusts input tax credit) or a financial credit note (a commercial adjustment outside the tax base) is a deliberate call with a batch-level GST trail — routed in full to the GST treatment of pharma claims and returns satellite. The end-to-end approval sequence is documented step by step in the claim approval workflow.

Source: ClaimDS — free to reuse with a link back to this article.

Where to go next

This pillar defines the channel and the vocabulary; the satellites below go deep on each moving part. Start wherever your leak is.

- Pharma stockist claim settlement process — the end-to-end claim journey from filing to credit note.

- Pharma expiry and breakage returns — how returns are documented, validated and settled at batch level.

- GST treatment of pharma claims and returns — the tax versus financial credit-note decision and its ITC impact.

- Supplier and purchase rebates in Indian pharma — the buy-side of the channel, where the stockist claims from the company.

- What is a CFA agent — the consignment model explained in depth.

For the wider picture, the channel rebates in India overview and the primary, secondary and tertiary sales primer set pharma in context against every other Indian distribution channel.

Bringing the batch trail under one roof

Pharma channel money leaks in the gap between what a batch was sold as and what it finally settles as — across expiry, breakage, schemes and the GST document that closes each one. ClaimDS is built to hold that trail in one place, from claim through validation and approval to the credit note.

<!-- TODO: confirm capability wording with founder -->Frequently asked questions

What is a C&F agent in pharma?

A C&F agent — carrying and forwarding agent — is the logistics partner a pharma company appoints to hold stock in a state depot and dispatch it against orders. The C&F holds goods on consignment, so the company still owns the inventory until it is billed to a stockist. The C&F earns a handling fee, not a trading margin.

What is a stockist?

A stockist is the licensed wholesaler who buys medicines from the company or its C&F agent and sells them onward to retail chemists in a defined territory. Also called a distributor in pharma, the stockist holds batch-tracked inventory, funds trade schemes at the counter, and files claims for expiry, breakage and scheme reimbursement back up the channel.

What is an expiry return?

An expiry return is stock a chemist or stockist sends back because it has passed, or is close to, its printed expiry date and can no longer be sold. In pharma these returns dominate the money flowing back up the channel. They are settled by credit note or replacement and follow a strict, batch-level GST route.

What is a saleable return?

A saleable return is stock sent back in resaleable condition — correct batch, intact packaging, well before expiry — usually after over-ordering or a range change. It can re-enter sellable inventory, unlike a non-saleable return, which is damaged or expired and must be destroyed. The distinction decides whether goods are restocked or written off.

Who settles pharma stockist claims?

The pharma company that supplied the stock settles the claim, through its commercial or finance team, after the claim clears validation and approval. Stockists and super stockists file claims upward against the company; a C&F agent may process the paperwork, but the liability and the credit note stay with the company that owns the brand.

What is PTR and PTS?

PTR is the price to retailer — the rate at which a stockist sells to a chemist. PTS is the price to stockist — the rate at which the company or C&F sells to the stockist. The gap between PTS and PTR is the stockist's margin, and both are printed reference points on most pharma claim and invoice documents.

How are pharma claims settled — credit note or replacement?

Most pharma channel claims settle by credit note against the stockist's account, offsetting future purchases rather than moving cash. Expiry and breakage claims are sometimes settled by physical replacement stock instead. Under GST the choice between a tax credit note and a financial credit note changes the input tax credit, so the instrument is a deliberate decision.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.