The Indian Multi-Tier Channel: Who Claims What

The Indian channel runs brand to C&F to super stockist to distributor to retailer — and claims flow back up it. Who claims what from whom, tier by tier.

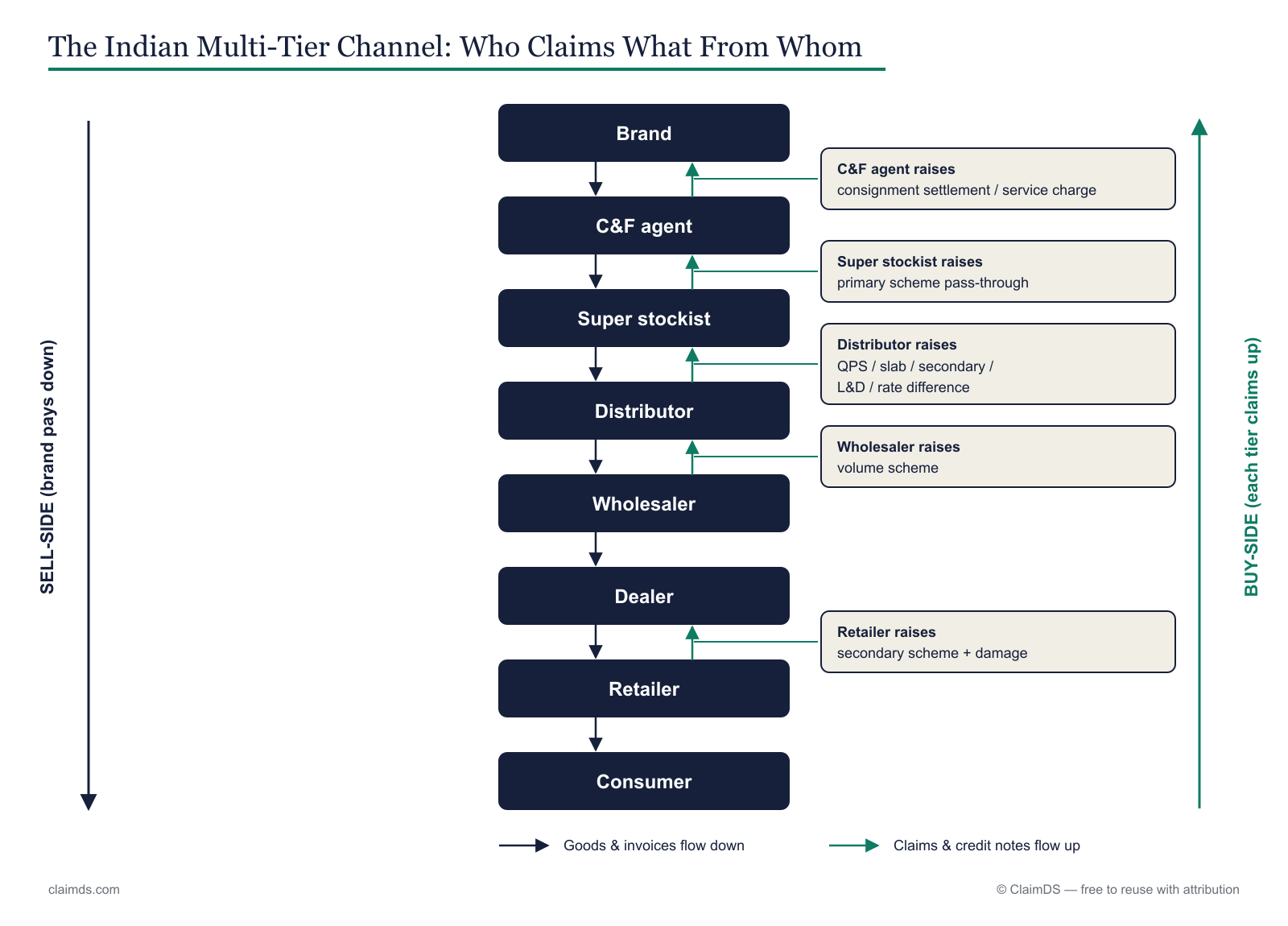

The Indian channel runs brand → C&F agent → super stockist → distributor → wholesaler → dealer → retailer, and goods flow down it. Claims flow the other way — up the same ladder, tier by tier, back toward the brand that funds the schemes. Each tier claims a specific mix from the tier above it, against evidence only it holds. This map shows who claims what from whom.

Source: ClaimDS — free to reuse with a link back to this article.

This is the structural reason Indian channel finance is hard: the channel claims and rebates that run through Indian FMCG cross more tier boundaries than any Western model, and each boundary is a handover where evidence can go missing. For the full economics of how money moves along it, see channel rebates in India. For the terminology, the glossary and what is a counterparty explain the roles below.

Brand / manufacturer

The brand makes the product, sets the MRP, and funds every scheme in the chain. It does not raise claims — it receives them and pays them out, usually as GST credit notes travelling back down the ladder. Its job is verification: confirming that the quantity, rate and period on each inbound claim match the agreement before money leaves. The evidence it must produce is the scheme circular itself — the signed terms that define what qualifies. When that document is loose, disputes multiply, and value leaks; the pattern is unpacked in revenue leakage in rebate programs. Everything downstream is the brand's obligation flowing outward and the claim flowing back.

C&F agent

The carrying-and-forwarding agent is the brand's logistics and billing arm inside a state. It warehouses stock and invoices super stockists or distributors on the brand's behalf, earning a handling fee or commission — it never owns the goods. Because the sale it bills is still the brand's own primary sale, the C&F rarely raises trade claims; at most it seeks reimbursement of agreed expenses like freight or godown handling. The evidence it produces is operational, not commercial: dispatch records, stock registers, and freight bills. The difference between a distributor, dealer and super stockist turns on exactly this — who carries inventory risk — and the C&F is the one tier that does not.

Super stockist

The super stockist is Indian FMCG's answer to geography. It buys in bulk from the brand or C&F, takes title, and redistributes to many small-town distributors the brand could not economically bill directly. It earns a thin trading margin plus schemes — and because it owns what it sells, it raises real claims: slab and quantity-purchase-scheme (QPS) claims, rate-difference claims when the brand cuts prices, and stock compensation on inventory it holds when prices fall. It claims from the brand. The evidence it must produce is its purchase record from the brand and its onward sales to each distributor — and because it inserts a whole tier, it widens the gap between primary, secondary and tertiary sales.

Distributor

The distributor is the workhorse tier: it buys in bulk, runs the delivery beat, extends retail credit, and executes schemes on the ground in an appointed territory. It raises the widest mix of claims in the channel — scheme and slab claims, secondary scheme settlements on its retailer-wise sales, damage and expiry credit, price-difference and rate-difference claims, and stock compensation on price drops. It claims from the brand (or via the super stockist). The evidence it must produce is the richest of any tier: purchase records, retailer-wise secondary sales from its billing software or DMS, and closing-stock statements. Worked arithmetic is in how to calculate FMCG distributor claims; the full lifecycle in distributor claims management.

Wholesaler

The wholesaler is the channel's opportunist — an unappointed bulk reseller who buys where stock is cheap and sells onward to smaller trade at a trading margin. It usually holds no territory, runs no structured beat, and carries no formal scheme obligations, which is exactly what separates it from a distributor. Its claims are correspondingly thin: it may pass on a QPS or slab benefit it earned on volume, and it may seek damage credit, but it rarely participates in retailer-wise secondary schemes because it does not report that data. It claims from whoever billed it — often a super stockist or distributor. The evidence it produces is purchase and sales quantity, little more; the broader scheme landscape sits in types of trade schemes in India.

Dealer

The dealer sits closest to the end customer, and in sectors like automotive, electricals and durables it sells and services the product. Its claim mix is distinctive: warranty and installation reimbursements barely exist higher up the chain, alongside incentive and target claims and price protection — which matters most here because dealers hold priced stock closest to a falling market. It claims from the brand or its distributor. The evidence it must produce is end-customer invoices, service and installation records, and local stock statements. The dealer's warranty claims and the retailer's display claims are the two clearest examples of tier-specific claim types that make a one-size template fail; dealer claims management covers the mix.

Retailer / kirana

The retailer — the corner kirana in FMCG — sells to the shopper and sits at the foot of the ladder. It claims the least in absolute value but the most in volume of small transactions: display and visibility incentives, secondary scheme benefits passed down on its purchases, and damage or expiry credit on unsold stock. Crucially, it claims from the distributor, not the brand, because the distributor billed it — so the claim rides on the distributor's secondary invoices. The evidence a retailer produces is minimal and often informal: purchase bills from the distributor and a photograph of the display. That informality is why retailer-level claims are the hardest rung to verify, and why the FMCG claim settlement process leans on the distributor's records to anchor them.

General trade vs modern trade

The map above is general trade (GT) — the long, multi-tier route through distributors and kiranas. Modern trade (MT) — large-format retail and organised e-commerce — collapses it. A brand often sells direct, or through a single distributor, to the MT chain, so the super stockist, wholesaler and independent-retailer tiers disappear. The claim mechanics change too. In GT, the tier below raises a claim and waits for approval and a credit note. In MT, the buyer simply deducts — it short-pays the invoice for the scheme, listing fee, or shortage it believes it is owed, and leaves the supplier to prove otherwise. Those deductions are chargebacks in FMCG distribution: the money is taken first and reconciled later, which inverts the burden of proof. Handling them well is a discipline of its own — see the chargeback process and deduction management best practices. The through-line across GT and MT is the same: whoever holds the evidence controls the claim. GT stretches that evidence across seven tiers; MT concentrates it into a deduction line, but neither forgives a missing document — a point the FMCG trade schemes explainer returns to.

Where ClaimDS fits

ClaimDS models every tier of the Indian channel natively — because flattening a seven-rung ladder to two parties is exactly where claims get lost. It settles what each tier raises, GST-correctly, whether the claim flows up general trade or arrives as a modern-trade deduction. See the pillar channel claims and rebates in Indian FMCG and book a demo to map your own channel.

Frequently asked questions

What is a C&F agent?

A carrying-and-forwarding (C&F) agent warehouses a manufacturer's stock and invoices on the brand's behalf for a handling fee, never taking ownership of the goods. Because the sale it bills is still the brand's own primary sale, a C&F rarely raises trade claims — it seeks expense reimbursements, not scheme money.

What is a super stockist?

A super stockist sits between the brand (or its C&F) and distributors: it buys in bulk, takes title to the stock, and redistributes to many small-town distributors a brand cannot bill directly. It earns a thin margin plus schemes, and raises slab, rate-difference and stock-compensation claims of its own.

What does a distributor claim from the company?

A distributor claims scheme and slab incentives, secondary-scheme payouts on its retailer sales, damage and expiry credit, price-difference and rate-difference amounts, and stock compensation when prices fall on inventory it holds. Each settles against the distributor's own purchase, secondary-sales and closing-stock records — which is why evidence quality decides the claim.

What does a retailer claim from a distributor?

A retailer claims display and visibility incentives, secondary scheme benefits passed down on its purchases, and damage or expiry credit on unsold stock. It settles against the distributor rather than the brand, because the distributor billed it — so the claim rides on the distributor's secondary invoices, not the brand's ERP.

What is the difference between a distributor and a wholesaler?

A distributor holds an appointed territory, runs a delivery beat, and executes the brand's schemes on retailer-wise secondary sales. A wholesaler is an unappointed bulk reseller who buys opportunistically and sells to smaller trade at a trading margin, usually without a territory, a beat, or structured scheme obligations to fulfil.

How many tiers are in the Indian FMCG channel?

A full Indian FMCG channel can run seven roles: brand, C&F agent, super stockist, distributor, wholesaler, dealer and retailer. Few products pass through all seven — many skip the super stockist or wholesaler — but the maximal chain is what makes Indian route-to-market longer, and claim flows longer, than most Western models.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.