What Is a Carrying and Forwarding (C and F) Agent?

A C&F agent (carrying and forwarding) holds and dispatches a company's stock on consignment and bills on its behalf — what a CFA does and how it is paid.

A carrying and forwarding (C and F) agent — a CFA — holds and dispatches a manufacturer's stock on consignment and invoices customers on the company's behalf, without ever taking ownership of the goods. It is paid a service charge or commission for warehousing, dispatch and billing, not a trading margin on a resale. The term is strongest in pharma, but the same arrangement runs across FMCG too.

That one distinction — consignment versus purchase — is what sets a CFA apart from every other tier in the Indian channel structure, and it changes how the agent is paid and what it can claim.

What does a C and F agent do?

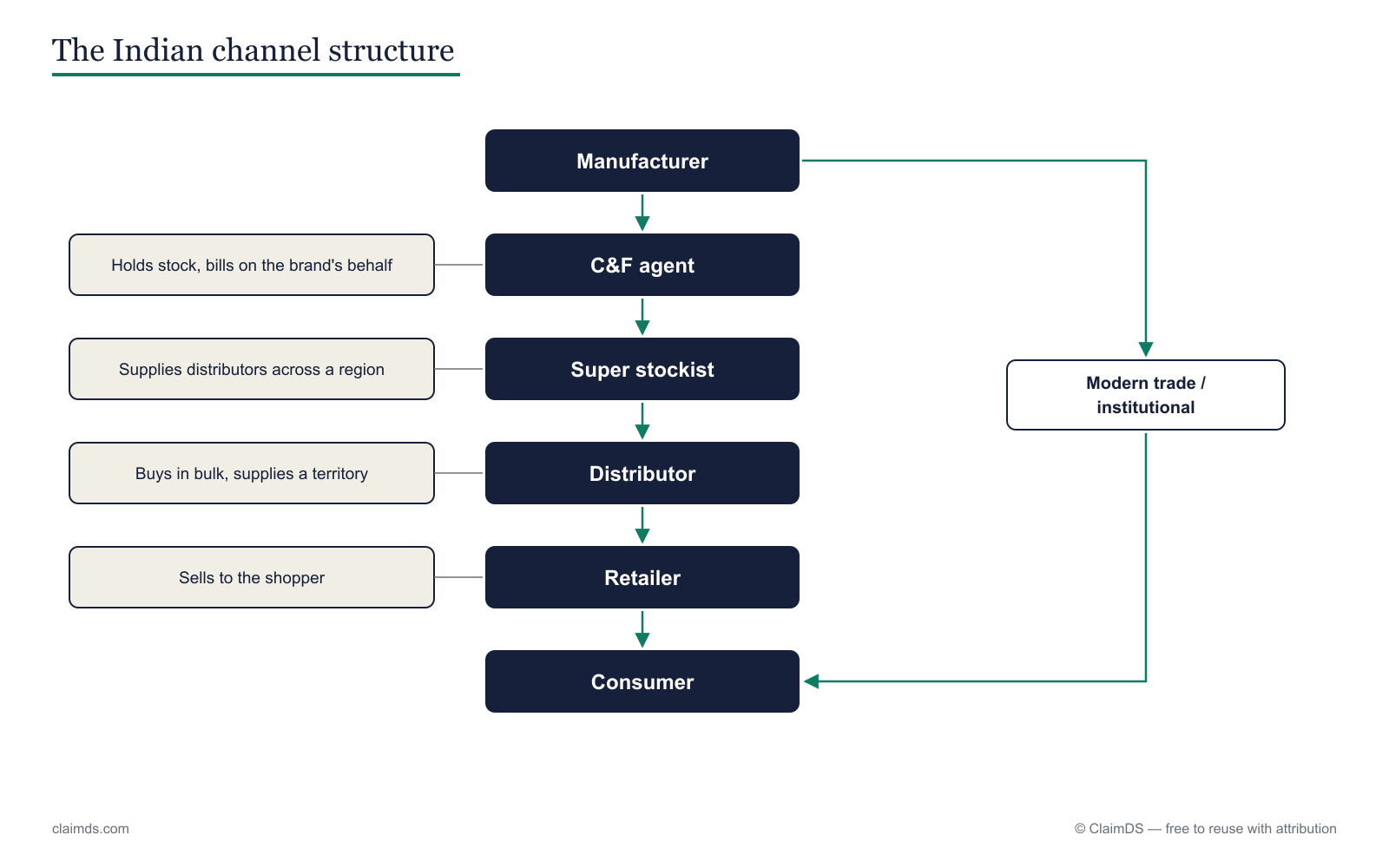

A C and F agent is the manufacturer's stocking and billing arm inside a state or region. It runs four core functions on the brand's behalf.

Warehousing. The CFA receives bulk stock from the factory and stores it in its own godown, but the goods remain the manufacturer's property. It manages batch, expiry and cold-chain discipline (critical in pharma) without ever buying the inventory.

Dispatch. When a stockist or distributor orders, the CFA picks, packs and forwards the consignment. It handles logistics — freight, transport and last-mile forwarding to the buyer — which is the "carrying and forwarding" the name describes.

Invoicing on the principal's behalf. The CFA raises the invoice to the buyer in the manufacturer's name. That sale is still the brand's own primary sale — the money conventionally settles to the manufacturer, and the CFA is not a party to the margin. Understanding where that first sale sits is the whole point of primary, secondary and tertiary sales.

Scheme pass-through and returns. The CFA applies the manufacturer's primary schemes at the point of billing and processes inbound returns — expiries, damages and near-dated stock coming back from stockists. It is the physical checkpoint through which most expired and damaged goods credit-note flows pass on their way back to the brand.

In short, a CFA does everything a stocking distributor does except own the goods and earn a trading margin — because it is an extension of the manufacturer, not an independent buyer.

C and F agent vs distributor vs super stockist

This is where most confusion lives, and the fix is a single question: who owns the stock?

A C and F agent does not buy the goods. It holds them on consignment and earns a service charge or commission. A super stockist and a distributor both do buy — they take title, carry the working-capital and credit risk, and resell on a trading margin. That difference in ownership drives everything else: how they earn, whose sale is billed, and which claims they can raise.

| C and F agent | Super stockist | Distributor | |

|---|---|---|---|

| Owns the stock? | No — holds on consignment | Yes — buys and resells | Yes — buys and resells |

| How it earns | Service charge / commission | Trading margin + schemes | Trading margin + schemes |

| Whose sale is billed | The manufacturer's (primary) | Its own, to distributors | Its own, to retailers |

| Carries inventory risk? | No | Yes | Yes |

| Typical claims | Service charge, reimbursements, damage-in-transit | Scheme, rate difference, stock compensation | Scheme, damage, expiry, price difference |

The super stockist and distributor differ from each other only in position — the super stockist sits above distributors and serves a wider region — but they are the same kind of party: buyers who resell. The CFA is a different kind of party altogether. For the full tier-by-tier breakdown, see distributor vs dealer vs super stockist, and for how each tier's claims travel back up the chain, how claims map across India's multi-tier channel.

The C and F agent sits between the manufacturer and the stockists, holding stock on consignment rather than buying it.

How is a C and F agent paid, and what does it claim?

Because a CFA never buys the goods, it cannot earn a trading margin — so it is compensated for a service, not for a resale.

Service charge or commission. The core payment is a handling charge, usually a percentage of dispatched primary-sale value or a fixed monthly fee. Illustratively, a CFA might earn ₹1.50–₹2.50 per case handled, or a small percentage of the primary billing routed through its godown. This is its revenue, and it is billed back to the manufacturer.

Reimbursements. On top of the service charge, the manufacturer typically reimburses pass-through costs the CFA incurs on its behalf — freight and transport, godown rent, insurance, and handling labour. These are cost recoveries, not margin.

The claims a CFA raises. Unlike a distributor, a CFA's claims are narrow and expense-shaped rather than scheme-shaped:

- Consignment settlement — reconciling stock received, dispatched and returned against the manufacturer's records, so that what is billed matches what physically moved.

- Service charge and reimbursement claims — the periodic handling fee plus freight, storage and insurance recoveries.

- Damage-in-transit and handling-loss claims — for stock damaged in the CFA's custody or in forwarding, settled against the manufacturer rather than a downstream buyer.

This is a different claim profile from the trade-scheme and price-difference claims a distributor lives on — a contrast the distributor claims management and pharma stockist claim settlement process guides both unpack. For how scheme money settles among buyers, see secondary scheme settlement and types of trade schemes in India.

The GST view: consignment and the principal-agent question

The tax treatment of a CFA turns on that same ownership point — and it is genuinely arrangement-specific, so treat this as a pointer, not an answer.

Where an agent holds and supplies goods on the principal's behalf, a consignment or del credere arrangement can, through the principal-agent provisions, cause the agent to be treated as a supplier in its own right for GST purposes — even though it never took commercial ownership. Whether that applies depends on the exact terms: how the invoice is raised, whether the agent bills in its own name, and how title and payment actually flow. A pure carrying-and-forwarding role that only invoices in the manufacturer's name may sit differently from an agent that supplies under its own GSTIN.

<!-- TODO CA REVIEW: principal-agent / consignment GST treatment (Schedule I) — reviewer to confirm; do not assert -->Because the outcome hinges on the arrangement's specifics, do not read a single rule off a template. The tax mechanics of channel money — schemes, chargebacks and the credit notes that settle them — are worked through separately in tax on rebates, chargebacks, billbacks and buybacks in India, and the counterparty concept itself in the glossary and what is a counterparty. Confirm the GST position for any specific CFA arrangement with a qualified professional.

Where the CFA sits in the bigger claims picture

The CFA is one node in a longer chain, and the same consignment-versus-purchase logic that defines it shapes the channel rebates in India flowing past it. In pharma it is central to the route to market — see the pharma channel claims and rebates pillar and chargeback mechanics in pharma distribution — while FMCG has the same stocking-and-billing role inside its channel claims and rebates picture. The discipline is identical: get ownership right, and the claim types, the payment basis and the claim process all fall into place. New to the money terms? Start with what is a rebate.

ClaimDS models the CFA, the stockist and the distributor as distinct counterparties — so consignment settlements, service-charge claims and downstream scheme claims each settle on the right basis, GST-correctly, in one India-first product. See claims management software, the pillar rebate management software, and worked distributor arithmetic in how to calculate FMCG distributor claims. Book a demo to see it settle your channel's claims end to end.

Frequently asked questions

What is a C and F agent?

A carrying and forwarding agent, or CFA, warehouses a manufacturer's stock and dispatches and invoices it on the company's behalf. The CFA never takes ownership of the goods; it holds them on consignment and earns a service charge or commission rather than a trading margin, acting as an extension of the brand's own logistics and billing.

What is the difference between a C and F agent and a distributor?

A distributor buys goods from the manufacturer, takes ownership, and resells them to retailers on a trading margin. A C and F agent buys nothing; it holds the manufacturer's stock on consignment and bills the brand's own sales. The distributor carries inventory and credit risk, while the CFA earns a fee for warehousing and dispatch.

What is the difference between a C and F agent and a super stockist?

Both sit high in the channel, but a super stockist owns the stock it sells — it buys from the manufacturer, carries the working capital, and resells to distributors at a margin. A C and F agent owns nothing; it holds the brand's goods on consignment and is paid a service charge. The test is who carries the inventory risk.

How is a C and F agent paid?

A C and F agent is paid a service charge or commission for handling the manufacturer's stock, not a trading margin, because it never buys or resells the goods. The charge is usually a percentage of dispatched value or a fixed fee, often with reimbursements for freight, warehousing, and handling costs incurred on the brand's behalf.

Does a C and F agent take ownership of the goods?

No. A carrying and forwarding agent holds the manufacturer's stock on consignment and never takes title to it. Ownership stays with the principal company until the goods are sold, and the invoice the CFA raises is the manufacturer's own primary sale. This is the defining feature that separates a CFA from a distributor or stockist.

What is a consignment agent under GST?

A consignment agent holds and supplies goods on a principal's behalf without owning them. Under GST, a consignment or del credere arrangement can, through the principal and agent provisions, treat the agent as a supplier for tax purposes. The treatment is arrangement specific, so confirm the correct GST position with a qualified professional.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.