Automotive Spare Parts and Aftermarket Claims

How spare-parts, tyre and lubricant claims work in the automotive aftermarket — the distributor channel, schemes, rate-difference and damage claims.

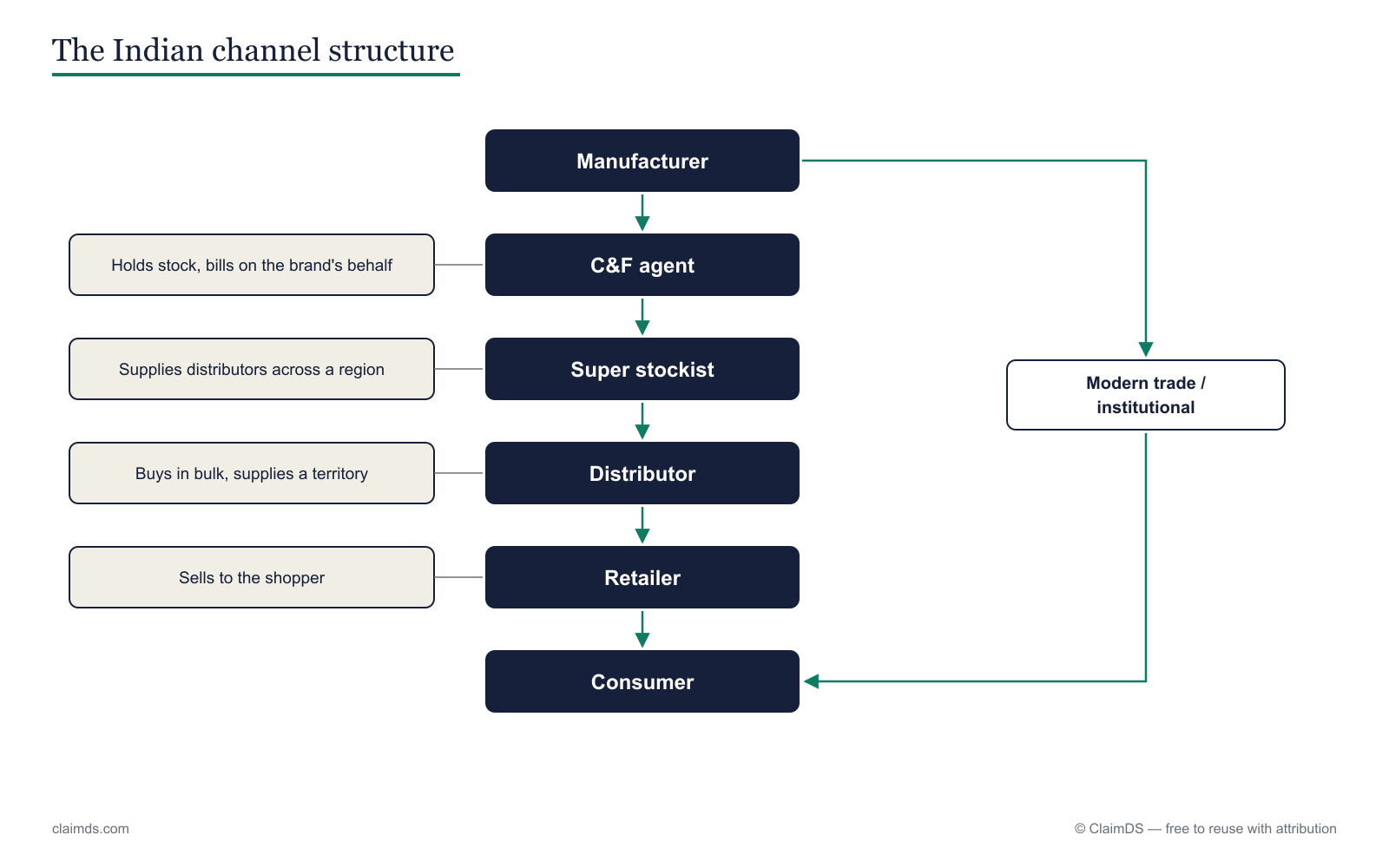

The automotive aftermarket — spare parts, tyres and lubricants — runs its own multi-tier distribution, separate from the OEM dealer channel. Goods flow from the parts manufacturer through a distributor to retailers, mechanics and garages, and finally to the vehicle owner. Along that chain the distributor raises volume and target scheme claims, rate-difference (price-revision) claims on stock it is holding when a price changes, and damage claims on unsaleable goods — nearly all of it settled not by cash but by credit note.

What is the automotive aftermarket channel?

The aftermarket is the parts-and-consumables business for vehicles already on the road: replacement components, tyres, lubricants, batteries and accessories bought long after the vehicle left the showroom. It is a distributor-led channel, and it is structurally different from the OEM 3S dealer network (Sales, Service, Spares) that a vehicle brand runs for its own models.

In the OEM dealer channel, the vehicle manufacturer appoints authorised dealers who sell new vehicles, service them, and stock genuine spares for those specific models — a single-brand, franchise-style relationship. The aftermarket sits alongside it: independent parts makers and consumable brands reach a far wider base of mechanics, garages and retailers through distributors who carry many brands and serve every make of vehicle, not one. The two channels overlap on the shelf but run on different economics and different claim mechanics. (For the OEM side, see the automotive dealer claim settlement process; the two channels together are mapped in the pillar on automotive channel claims and rebates in India.)

| Feature | OEM 3S dealer channel | Aftermarket channel |

|---|---|---|

| Who sells | Authorised single-brand dealer | Multi-brand distributor and retailer |

| Products | Genuine spares for the brand's models | Parts, tyres, lubricants for all makes |

| End buyer | Owner servicing at the dealership | Owner via mechanic, garage, retailer |

| Relationship | Franchise, brand-controlled | Independent trade, distributor-led |

| Typical claims | Warranty, incentive, price-protection | Volume scheme, rate-difference, damage |

The mechanics rhyme with FMCG distribution — the distributor tier buys in bulk, earns a trading margin plus schemes, and raises claims that flow back up the channel while goods flow down.

The aftermarket runs a distributor-led channel separate from the OEM dealer network.

What claims do aftermarket distributors raise?

Four claim types dominate the aftermarket, and each has its own evidence.

Volume and target schemes. The most common. A manufacturer sets a purchase target — units, litres, or value over a month or quarter — and pays a per-unit or slab incentive when the distributor hits it. Slab structures step the rate up as volume rises, so the last units earned carry the richest rate. These are the same trade-scheme mechanics used across Indian distribution, and the slab logic is set out in rebate slabs and scales.

Rate-difference (price-revision) claims. When a price changes on stock the distributor is already holding, the difference is claimed. This is the aftermarket's version of price-drop protection, and it gets its own section below.

Damage and breakage. Parts arrive cracked, a lubricant pack leaks, a battery is dead on receipt. The distributor claims the value of goods that cannot be sold, supported by evidence of the damaged stock — mechanically the same discipline as credit notes for expired and damaged goods returns.

Display and visibility support. Payments for shelf space, retailer branding, or point-of-sale material at garages and parts shops — a secondary-tier support that reaches the retailer through the distributor, close in spirit to secondary scheme settlement.

Left unmanaged, these claims are a classic source of revenue leakage in rebate programs — over-claimed quantities, duplicate submissions and unreconciled deductions all hide in aftermarket volumes. Tight deduction-management practice is what keeps the channel honest.

How do tyre and lubricant schemes work?

Tyres and lubricants are the two highest-volume aftermarket categories, and each carries a mechanic worth naming.

Pro-rata tyre warranty is genuinely distinct. Unlike a flat replacement, a tyre replaced under pro-rata warranty is settled in proportion to the tread life already used. If a tyre rated for a given life fails part-way through — a manufacturing defect surfacing after real road use — the customer pays for the portion of tread already consumed and the manufacturer bears the balance. So the claim value turns on measured remaining tread, not a fixed amount, which makes a pro-rata warranty claim different from an ordinary damage claim where the whole unit is written off. Verifying the tread measurement and the failure basis is central to settling these fairly.

Lubricant schemes lean on volume and packaging. Distributors earn per-litre or slab incentives on qualifying offtake, and manufacturers layer pack-based and combo offers on top — a free unit with a case, a bundled promotion across grades, a festival or season scheme on specific SKUs. Because lubricants move in many pack sizes, the qualifying quantity has to be normalised (to litres, or to a defined base pack) before a scheme can be reconciled — a small step that, skipped, produces exactly the mismatches that stall settlement.

Both categories ultimately settle the same way the rest of the channel does in India: scheme quantity reconciled against sales evidence, then a credit note. Keeping brands generic here is deliberate — the mechanics hold whichever tyre or lubricant marque is on the invoice.

How do rate-difference claims arise when prices change?

A rate-difference claim starts with a price revision. A manufacturer changes the list price of a part, a tyre or a lubricant; the distributor (and often the retailer below it) is still holding stock bought at the old price. When the price is cut, that stock is suddenly worth less than what was paid for it, and the channel would be left carrying the loss unless the manufacturer makes it good. The rate-difference claim covers exactly that gap, computed per unit of stock-in-hand at the moment of the revision.

The arithmetic is simple and illustrative: if a part bought at ₹480 is repriced to ₹450 and the distributor holds 200 units, the rate-difference claim is ₹30 × 200 = ₹6,000 on that line. The hard part is not the multiplication — it is establishing the stock position on the effective date. That is why a dated stock statement anchors every rate-difference claim, the same stock-compensation discipline used elsewhere in the channel.

The tax treatment of a rate-difference credit note is a separate question and a pointer only here: whether it can carry a GST adjustment or must be a commercial credit note depends on how the price reduction was agreed and documented. That is worked through in detail in price protection and rate-difference credit notes under GST — the operational takeaway is simply that the claim exists the moment the price moves on stock already sold into the channel.

How are aftermarket claims evidenced and settled?

Every aftermarket claim reduces to the same question: prove the quantity, then settle the amount. Three pieces of evidence do most of the work. A stock statement fixes what the distributor was holding on the effective date — essential for rate-difference and price-revision claims. A scheme reference ties the claim to the specific circular or agreement that authorised it, with its slab, rate and qualifying period. And sales or purchase data from the distributor's own records establishes the qualifying volume for scheme claims — secondary numbers that live in the distributor's system, not the manufacturer's ERP.

Claims run against a claim window — a defined period after the scheme or price event within which the distributor must submit. Miss it and the claim lapses, so a shared view of open windows matters as much as the arithmetic. This is the standard claim process applied to aftermarket volumes, and it settles the way distributor claims settle generally: the manufacturer verifies the quantity, approves the amount, and issues a credit note against the distributor's account rather than paying cash. For the terminology, the glossary defines each term in one line.

Where ClaimDS fits

ClaimDS models the aftermarket channel natively — distributor tiers, volume and slab schemes, rate-difference claims on stock-in-hand, and damage claims — and settles each by credit note with the evidence reconciled and the claim window tracked. It sits alongside the OEM side, so a business running both the dealer channel and the aftermarket manages them in one India-first product, GST-correctly (the GST and TDS treatment of automotive incentives is handled as its own concern). See how it settles the wider FMCG claim settlement process, and the pillar rebate management software.

Book a demo to see spare-parts, tyre and lubricant claims settled end to end.

Frequently asked questions

What is the automotive aftermarket?

The automotive aftermarket is the channel that supplies spare parts, tyres, lubricants, batteries and accessories after a vehicle is sold — separate from the manufacturer's own dealer network. It runs its own multi-tier distribution, from parts maker to distributor to retailer, mechanic and garage, and serves the vehicle already on the road.

What claims do spare-parts distributors raise?

Aftermarket distributors raise four main claim types: volume or target scheme claims on qualifying purchase quantities, rate-difference (price-revision) claims on stock held when a price changes, damage and breakage claims on unsaleable goods, and display or visibility support claims. Each settles against the distributor's own stock and sales records rather than the manufacturer's ERP.

How are tyre and lubricant schemes settled?

Tyre and lubricant schemes settle mostly on volume: qualifying units or litres over a period earn a per-unit or slab incentive, paid back to the distributor by credit note. Lubricants add pack-based and combo offers, while tyres add pro-rata warranty replacement. Both reconcile scheme quantity against sales evidence before the credit note issues.

What is a rate-difference claim?

A rate-difference claim (also called a price-revision claim) arises when a manufacturer changes the price of goods a distributor or retailer is already holding. If the price is cut, the channel claims the difference on unsold stock so it is not left carrying inventory bought at the old, higher price. It is settled per unit of stock-in-hand by credit note.

What is a pro-rata tyre warranty?

A pro-rata tyre warranty replaces a tyre in proportion to the tread life already used. If a tyre fails part-way through its rated life, the customer pays for the portion consumed and the manufacturer covers the rest — so the claim value depends on measured remaining tread, not a flat replacement. This makes tyre warranty claims distinct from ordinary damage claims.

How are aftermarket claims settled?

Aftermarket claims settle by credit note against the distributor's account, not by cash. The distributor submits a stock statement or sales data plus the scheme reference within a defined claim window; the manufacturer verifies quantities, approves the amount, and issues a credit note that reduces what the distributor owes on future purchases. The GST treatment of that credit note is a separate question.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.