Channel Claims and Rebates in Building Materials

How schemes, claims and rebates work across the Indian building-materials channel — volume slabs, dealer boards, rate difference and breakage claims.

Building-materials brands — cement, tiles, sanitaryware, plywood, adhesives, pipes — sell through a deep dealer, sub-dealer and retailer channel, with a parallel project-sales route to contractors and builders. Money flows back up that channel as volume-slab schemes, dealer-board and branding support, and rate difference when prices revise on held stock, almost always settled by credit note. Running alongside are breakage and damage claims — the fragile-goods problem that makes tiles and sanitaryware distinct. Together these define what a building-materials company reconciles every month.

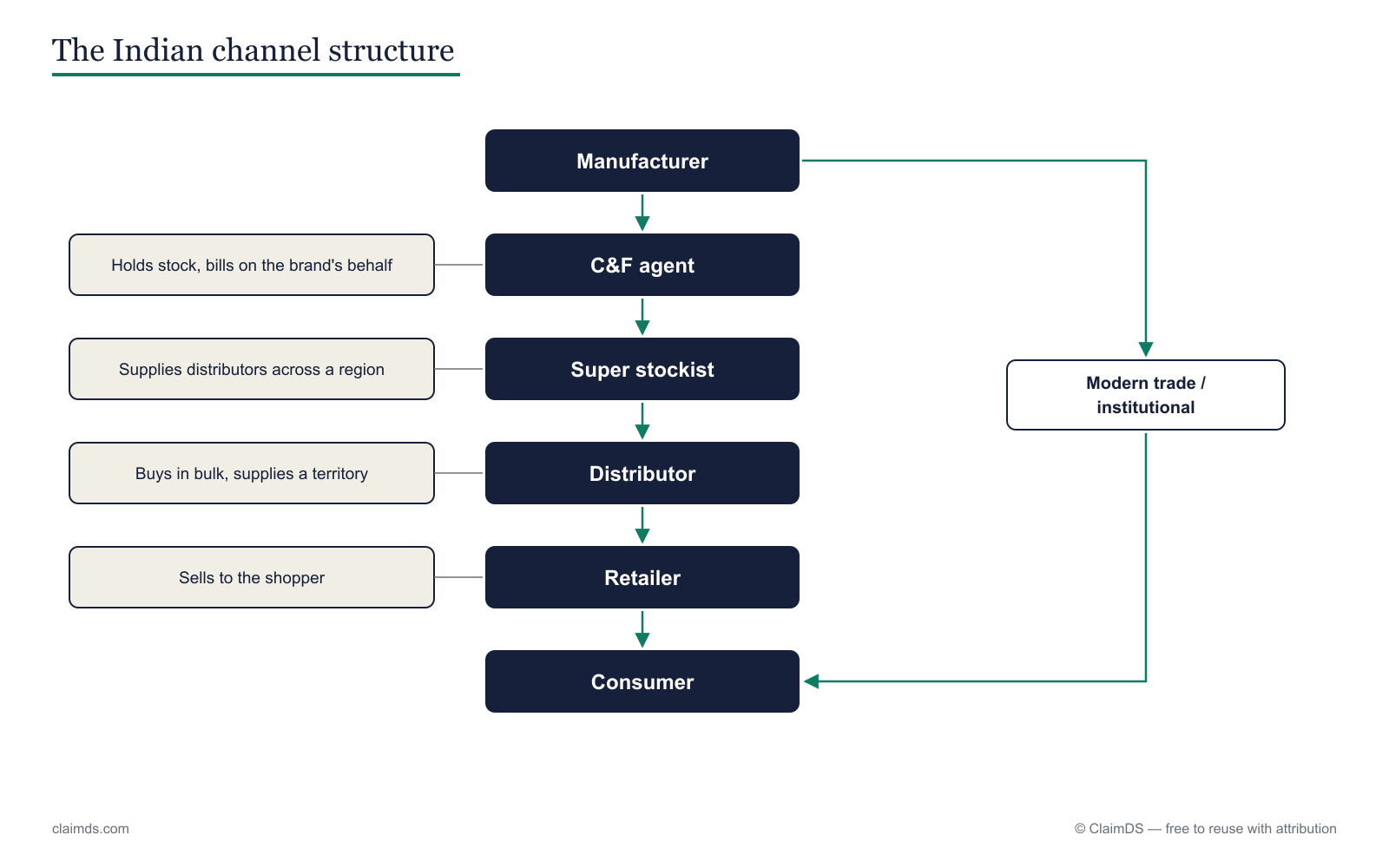

The building-materials channel, tier by tier

Building materials run on a long distribution spine with a second route bolted on: while most stock reaches the market through a conventional dealer chain, a large share of demand is booked as project sales to contractors and builders who buy in bulk for a site. Mapping both routes is the prerequisite for knowing which claim comes from whom, because a project order and a counter sale earn benefits on entirely different terms.

At the top, the manufacturer owns the products, runs the plants, publishes the price list, and declares every scheme. It rarely ships direct to the trade; instead it moves stock to a C&F or depot — a carrying-and-forwarding agent or regional warehouse that holds inventory and invoices on the company's behalf. From there, stock reaches the distributor or stockist, the partner who carries working capital and breaks bulk for a territory. Below sits the dealer and sub-dealer — the trade counters that hold local stock and execute the company's schemes — and then the retailer selling to walk-in customers and small builders.

Running parallel is the project or contractor route: large orders negotiated for a specific construction site, often at a special project price, sometimes shipped direct from depot. At the base is the end user — the household or builder whose wall, floor or bathroom the material finally becomes.

Building materials run a deep dealer channel, with a parallel project-sales route.

Building materials run a deep dealer channel, with a parallel project-sales route.

| Tier | What it does | What it claims or earns | From whom |

|---|---|---|---|

| Manufacturer | Owns products, declares schemes and prices | Nothing (settles claims) | — |

| C&F / depot | Stocks regionally, invoices the trade | Handling margin, no claims | Manufacturer |

| Distributor / stockist | Carries capital, breaks bulk | Volume slabs, rate difference | Manufacturer |

| Dealer / sub-dealer | Holds local stock, runs schemes | Volume slabs, dealer boards, breakage returns | Company / distributor |

| Retailer | Sells to walk-ins and small builders | Display support, small-volume benefit | Dealer / company |

| Project / contractor | Buys in bulk for a site | Project price, project-specific benefit | Manufacturer (direct) |

| End user | Uses the finished material | Nothing | — |

If the line between a distributor, a dealer and a super stockist blurs in your own network, the difference between a distributor, dealer and super stockist explainer untangles it, and India's multi-tier channel claim map shows how these tiers connect across industries. The split between primary, secondary and tertiary movement — company to trade, trade to retail, retail to end user — is covered in primary, secondary and tertiary sales.

What claims does a building-materials company handle?

A building-materials company pays its channel through several distinct claim types, and folding them into one bucket is the first mistake a manual process makes. Each carries its own evidence, its own validation rule, and its own settlement path.

Volume and slab schemes are the core trade reward: buy or sell a defined quantity over a month or quarter, cross a value slab, and a per-unit or percentage benefit applies. These sit inside the wider family of trade schemes in India.

Dealer boards and branding support reimburse the dealer for carrying the company's brand — a signboard, a painted storefront, a product display. This is market-development spend, mirroring the pattern in market-development-fund and co-op claims.

Rate-difference claims compensate the dealer when prices revise on stock already bought, the same protection logic as price protection and rate-difference credit notes under GST.

Breakage and damage returns cover fragile stock — tiles, sanitaryware — that arrives or turns broken, following the discipline in credit notes for expired and damaged goods returns.

Display and counter schemes reward the retailer for shelf space and point-of-sale presence — an evidence-and-reimbursement claim rather than a performance one.

A building-materials channel claim is a dealer's request to collect a promised benefit — a volume slab, board support, a rate difference or breakage credit — validated against scheme terms and settled by credit note.

| Term | What it means in building materials |

|---|---|

| Volume slab | A quantity or value band that unlocks a stepped incentive rate |

| Dealer board | Branded signage the company funds at the dealer's shop |

| Rate difference | Credit for the price gap on held stock after a revision |

| Breakage claim | Credit for tiles or sanitaryware that arrive or turn broken |

| Damage return | Stock returned as unsaleable within policy terms |

| Project price | A special negotiated rate for a bulk site order |

| Secondary scheme | An incentive on trade-to-retail movement, not primary purchase |

| Display scheme | Reimbursement for shop display or counter presence |

| Credit note | The instrument that settles most claims against the ledger |

| Offtake | The purchase or sales volume a slab claim is measured against |

The glossary carries the wider vocabulary, and distributor claims management frames how these claim types are handled end to end.

Volume slabs and dealer boards

Two schemes define the building-materials channel more than any other: the volume slab and the dealer board. They reward opposite things — one rewards throughput, the other rewards visibility — and they are claimed and validated in completely different ways.

A volume-slab scheme pays a benefit that steps up as offtake crosses defined bands. A dealer buying within a lower band earns a modest per-bag or per-box benefit; crossing into the next slab lifts the rate on the qualifying volume for the period. The claim is filed after the period closes, and validation is arithmetic: the company matches the dealer's offtake against the slab table and computes the earned amount. Where the benefit rides on secondary movement rather than primary purchase, it follows the pattern in secondary scheme settlement. Getting the slab boundaries and the qualifying volume right is where most disputes start, which is why claim and rebate approval workflows matter as much as the scheme design.

A dealer-board or branding claim works nothing like a slab. There is no volume to measure — the dealer has spent money making the shop carry the brand, and files for reimbursement against evidence: photographs of the installed board, the fabricator's invoice, the site location. This is market-development spend, and it is governed the same way as market-development-fund and co-op claims: a budget, an approval, and proof of execution before a rupee is settled. Treating a board claim like a volume claim — or vice versa — is a common source of revenue leakage in rebate programs, because the wrong validation rule lets the wrong claims through.

Breakage, damage and rate-difference claims

Two problems make building materials harder to settle than a typical FMCG channel: fragile goods and frequently moving prices.

Breakage and damage dominate the tiles and sanitaryware segments. A pallet of tiles or a consignment of ceramic sanitaryware can arrive with cracked, chipped or shattered pieces, and more can break in the dealer's godown before sale. The dealer records the damaged quantity with photographic evidence, returns or scraps the stock per the company's policy, and files for credit on the accepted value. Because the loss is physical and the evidence is visual, validation leans on documented proof rather than a performance table — the same discipline set out in credit notes for expired and damaged goods returns.

Rate difference is the pricing problem. Building-materials prices move with input and freight costs, and a company may revise its price list several times a year. When a price is cut, dealers holding stock bought at the old rate would lose money purely because of the revision — so the company compensates the gap on unsold stock. The claim is reconciled against the dealer's held-stock position at the revision date, and settled by credit note. The mechanics and the paperwork are detailed in price protection and rate-difference credit notes under GST.

How building-materials schemes settle in India

Almost every building-materials claim settles the same way: by credit note against the dealer's purchase account. Rather than moving cash, the company reduces what the dealer owes on future orders by the earned amount — a settlement that keeps the trade relationship on a running ledger.

There is a distinction that matters at settlement. A financial credit note adjusts the commercial ledger between the two parties, while a tax credit note additionally changes the GST position on the original supply. Which one applies depends on the scheme type and the supporting paperwork, and the difference is explained in financial versus tax credit notes under GST. The broader mechanics of adjusting GST across channel settlements sit in GST adjustments in channel settlements, and the tax treatment of rebates, chargebacks and buybacks more generally in tax on rebates, chargebacks, billbacks and buybacks in India.

A building-materials claim validated against its scheme rules before a credit note is issued.

A building-materials claim validated against its scheme rules before a credit note is issued.

Before any of that, the claim has to pass validation and approval, the flow described in the claim approval workflow.

This is general information, not tax advice. GST treatment of a credit note depends on the scheme, the documentation and the timing — confirm the position with a qualified professional before you settle.

Bringing it together

Building materials pays its channel on four signatures: volume slabs that reward throughput, dealer boards that reward visibility, rate difference that protects held stock when prices move, and breakage claims that absorb the fragility of tiles and sanitaryware — all running against a deep dealer chain and a parallel project-sales route, and nearly all settled by credit note. The pattern rhymes with the paints channel and the wider story of channel rebates in India, but the fragile-goods and frequent-revision dimensions are its own. Handling them well takes purpose-built rebate management software and dealer claims management software rather than a spreadsheet per scheme.

<!-- TODO: confirm capability wording with founder -->ClaimDS is built to validate volume-slab, dealer-board, rate-difference and breakage claims against their scheme rules and settle them by credit note — with the dealer rebate software depth the building-materials channel needs. Book a demo to see it run on your schemes.

Frequently asked questions

What is a building-materials channel claim?

A building-materials channel claim is a request a dealer or distributor files to collect a benefit the manufacturer promised — a volume-slab incentive, dealer-board support, a rate-difference credit after a price revision, or credit for breakage and damage. The company validates it against scheme terms and stock records, then settles it, usually by issuing a credit note against the dealer's purchase account.

How do volume-slab schemes work?

A volume-slab scheme pays a benefit that steps up as purchases or sales cross defined quantity or value bands over a period. A dealer who buys within a lower slab earns a smaller per-unit benefit; crossing the next slab lifts the rate on the qualifying volume. The dealer files a claim, the company checks the offtake against the slab table, then settles the earned amount by credit note.

What is a dealer board or branding claim?

A dealer-board or branding claim reimburses a dealer for displaying the company's brand — a shop signboard, a painted storefront, a product display, or in-shop signage. It is a marketing-support claim, not a performance reward, so it settles against evidence such as photographs and invoices rather than against sales volume. It follows the same logic as market-development-fund and co-op claims.

How are breakage and damage claims handled?

Breakage and damage claims cover fragile stock — tiles and sanitaryware especially — that arrives cracked, chipped or broken, or is damaged in the dealer's godown within agreed terms. The dealer records the damaged quantity with evidence, returns or scraps it per policy, and files for credit. The company validates the claim against its returns policy, then issues a credit note for the accepted value.

What is a rate-difference claim in building materials?

A rate-difference claim arises when the company revises prices while a dealer still holds stock bought at the old rate. Building-materials prices move often with input costs, so on a price cut the company compensates the dealer for the gap between the old and new price on unsold stock, usually by credit note. It protects the dealer from a loss caused purely by the company's revision.

How do building-materials channel claims settle in India?

Most channel claims settle by credit note against the dealer's purchase account, offsetting future orders rather than moving cash. A financial credit note adjusts the commercial ledger, while a tax credit note additionally affects the GST position. Which applies depends on the scheme and the paperwork, so the tax treatment must be confirmed with a qualified professional at settlement time.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Channel Claims and Rebates in Indian Agri-Inputs

How schemes, claims and rebates work across the Indian agri-input channel — fertilizers, crop-protection and seeds, seasonal schemes and expiry returns.

How to Settle Agri-Input Dealer Claims

The step-by-step process to settle agri-input dealer and distributor claims in India — seasonal schemes, liquidation claims and near-expiry returns.

Expiry and Season-End Returns in Agri-Inputs

How near-expiry, damage and season-end returns work in Indian agri-inputs — declaring returnable stock, the claim window and how each return settles.