Managing Rebates, Schemes and Claims When You Run Tally

How Indian distributors and manufacturers on Tally handle rebates, trade schemes and claims — where the ledger ends and the claims workflow begins.

If you run your books on Tally, your transactions are already in good hands — the invoice, the credit note, the ledger entry all live there cleanly. Trade schemes and distributor claims are a different job. They are about the rules around those transactions: what was promised, on what base, backed by what evidence, and within which settlement window. That rules work rarely fits inside an accounting entry, which is why most teams end up running it in spreadsheets beside their books.

What does Tally handle well?

Tally (TallyPrime) is a capable accounting system, and this article is not an argument for moving off it. For a large share of Indian distributors and manufacturers it is the right system of record, and nothing here suggests otherwise.

At its core, Tally records transactions and produces the books: sales and purchase vouchers, ledgers, credit and debit notes, and stock. Teams also use it in their GST return workflow. These are the things an accounting system is meant to do, and Tally does the job that keeps the books correct and auditable.

Because feature sets differ across configurations and editions, treat any specific capability as something to confirm rather than assume. If you are wondering whether your particular version supports a given report, export format, or scheme-related field, check whether your version supports it directly in your own setup — that is more reliable than a general claim in an article.

The point of this piece is not what Tally lacks. It is that scheme and claim management is a different kind of task from bookkeeping — a rules problem that sits beside the ledger rather than inside it. Understanding that distinction is what keeps both jobs clean: the accounting system stays the trusted record, and the scheme logic gets a home built for rules. For a broader view of how claims tools and accounting systems fit together, see our guide to ERP integration for claims and rebate software.

Where does scheme and claim work end up outside the ledger?

Walk through a typical scheme and you find the work leaking out of the books for structural reasons, not because of any product shortcoming.

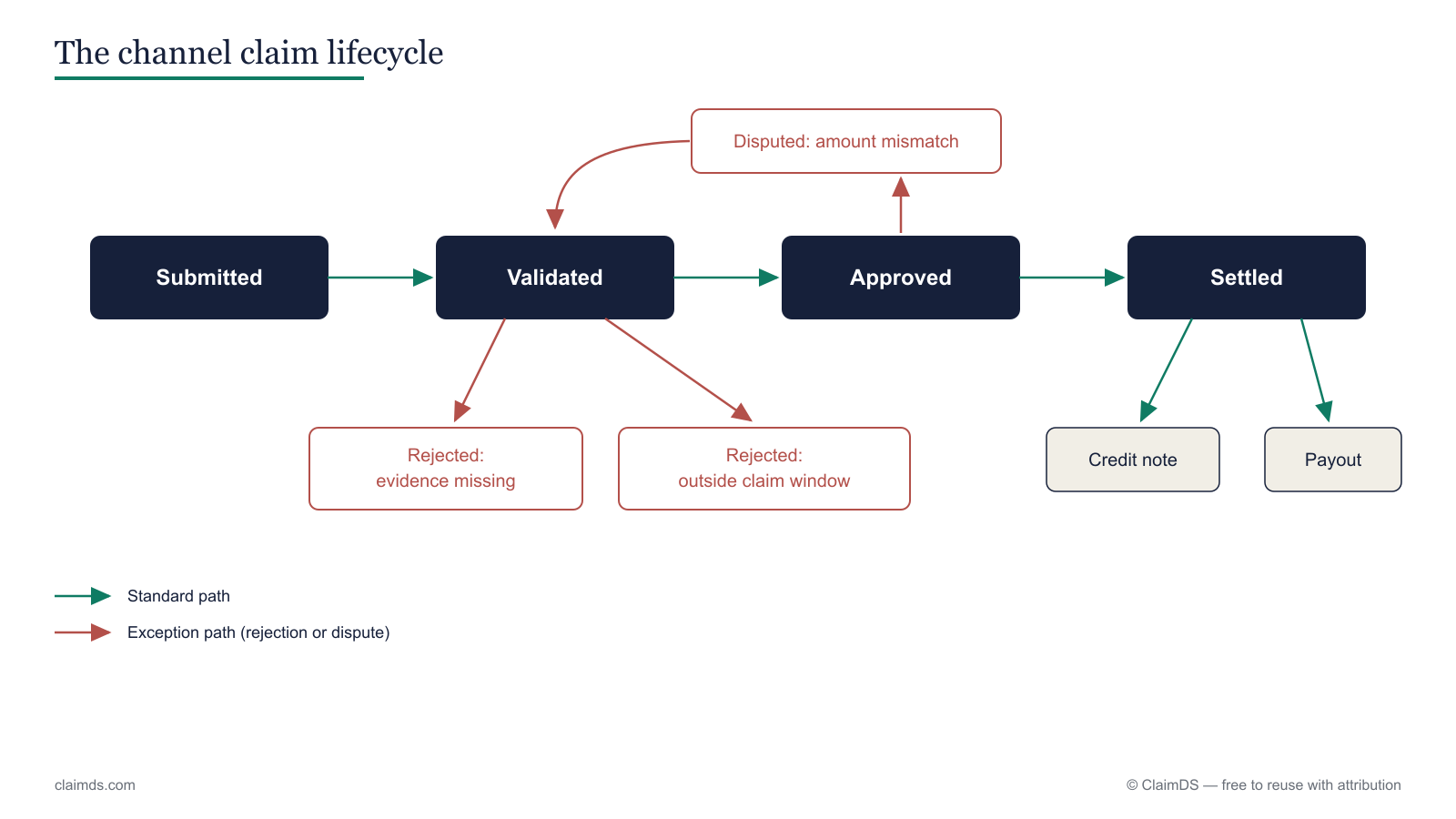

The scheme circular has no home in the ledger. A quarterly scheme — say a slab on volume, or a rate difference on a price drop — starts as a circular or an email. Its terms (the base, the tiers, the eligible SKUs, the window) are rules, not transactions, so there is no natural voucher to store them in. They end up in a spreadsheet or an inbox.

Secondary sales sit in the distributor's books, not yours. Many trade schemes pay on sell-through — what the distributor sold onward — but that data lives in the distributor's system or a DMS, not your ledger. You are computing an entitlement against numbers your accounting system never sees. This is the heart of secondary scheme settlement and a common source of revenue leakage.

Claims arrive as evidence, not entries. A distributor claim comes in as a statement, a photo of a display, a stock-return note — proof that something happened. Evidence has to be checked against the scheme terms before any entry is justified, and that validation step has no place in a voucher.

Validation is a rules problem across four data sources. To approve one claim correctly you reconcile the scheme terms, primary sales, secondary sales, and the submitted evidence. Getting those four to agree is distributor claims management, and it is inherently a cross-source exercise the ledger was never meant to run.

The accrual has to be computed. Between the promise and the settlement, you owe an amount you should be carrying as a liability. Computing and tracking that accrual — see calculating FMCG distributor claims — is ongoing rules work, not a one-time posting.

None of this is a complaint about accounting software. It is simply a different job — a claims management and rebate management problem — that belongs in a place built for rules, with a clean approval workflow and deduction discipline. ClaimDS is built for exactly this rules layer. <!-- TODO: confirm capability wording with founder -->

The credit note is the join

Here is the practical way the two jobs meet. You do not need the claims logic and the accounting logic to be one system. You need them to agree on one document: the credit note.

Think of it as a division of labour. The claims system decides what is owed and why — it holds the scheme terms, validates the claim against primary and secondary sales and evidence, and computes the settlement. The accounting system issues and posts the credit-note document — the GST-correct voucher that moves the money in the books. The credit-note number is the thread that ties the two records together: one settlement in the claims system, one credit note in the ledger, same reference on both.

That principle keeps each system doing what it is good at. The claims workflow owns the rules and the audit trail behind the number; the accounting system owns the posting and the statutory record. Neither has to absorb the other's job.

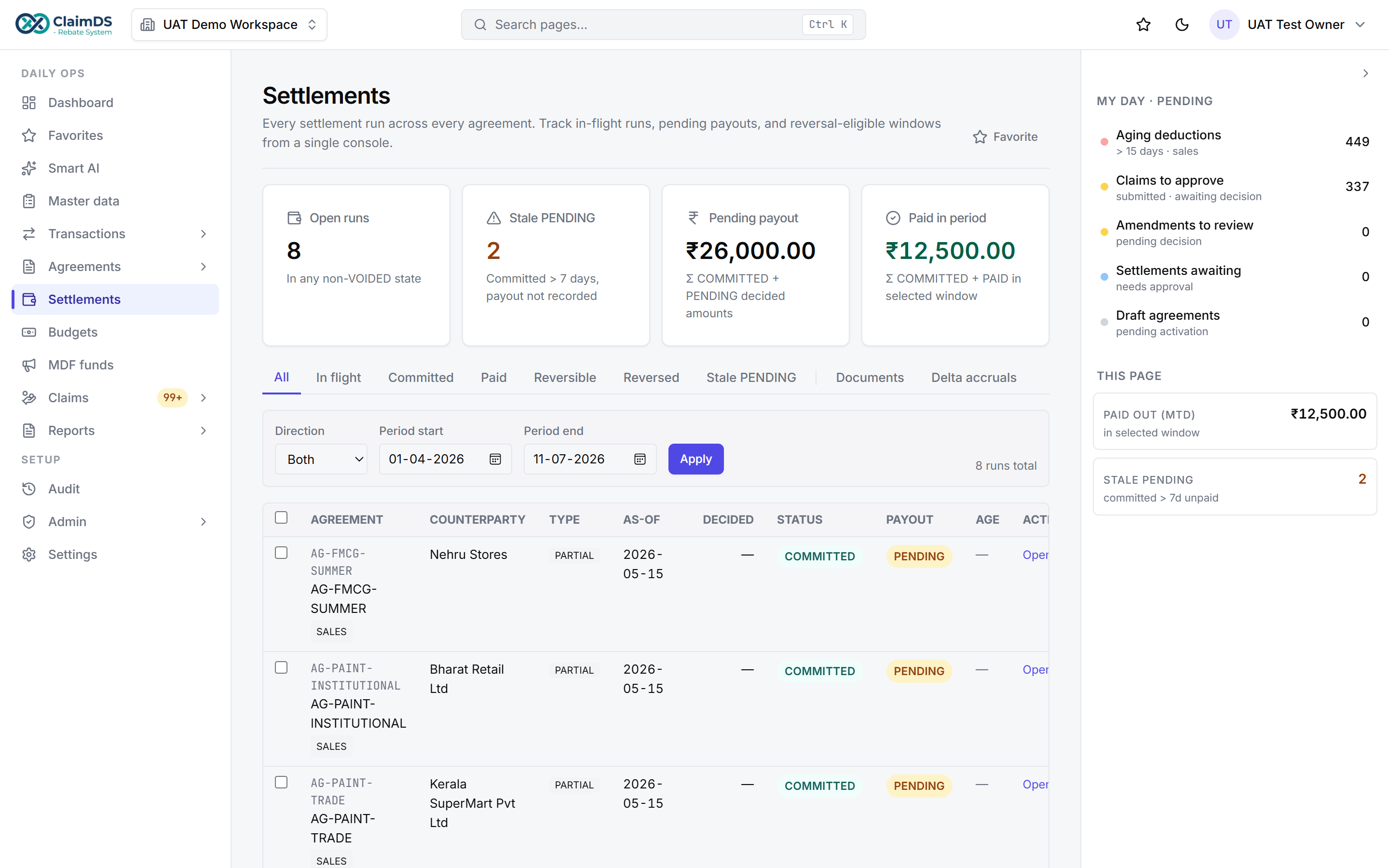

In ClaimDS specifically, this join is a file exchange: ClaimDS computes the settlements and exports them as an Excel or CSV file, which you then import or key into Tally as credit notes. It is a file-based export-import, not a native or live API connector — the two systems stay independent. <!-- TODO: confirm capability wording with founder -->

The claims system decides what is owed; the credit note posted in Tally is the join.

The claims system decides what is owed; the credit note posted in Tally is the join.

For the GST mechanics of that credit note, see financial versus tax credit notes, GST adjustments on channel settlements, and reconciling scheme credit notes with GSTR-2B/3B.

What does a practical setup look like?

You do not have to change how you keep your books. A clean arrangement keeps Tally as the system of record and adds a dedicated home for the rules:

- Manage schemes and claims in a claims system. Load the scheme circulars, the eligible partners and SKUs, and the tiers once. Let claims come in against those terms with their evidence attached, and validate them there — against channel rebate rules, primary sales and secondary sales — rather than in a spreadsheet.

- Compute the settlement and accrual in the same place. The claims system carries the running liability and produces the final amount owed per partner, per scheme, with the reasoning preserved for audit.

- Post settlements as credit notes in Tally. Each approved settlement becomes a credit note in your accounting system — the statutory document, issued and posted the way you already do it.

- Keep one reconciliation between the two. Export the settled amounts from ClaimDS as Excel or CSV and import or key them into Tally, then reconcile the two lists so every settlement maps to exactly one credit note. <!-- TODO: confirm capability wording with founder -->

That single reconciliation point — one file out of the claims system, one set of credit notes in Tally — is what keeps the books and the scheme records honest without merging the two systems. For the settlement and reconciliation surfaces themselves, see our solution pages on claims and deduction reconciliation, settlement and payout management, and GST credit-note reconciliation, plus the Tally integration overview. The glossary and the claim approval workflow walkthrough cover the terms and steps in more detail.

Settlements computed in ClaimDS, then posted as credit notes in your accounting system.

Settlements computed in ClaimDS, then posted as credit notes in your accounting system.

If you run a different accounting stack, the same principle applies — see the companion pieces for Busy users and Zoho users, and the broader view on running claims alongside your accounting system.

Keep Tally as your system of record. Give the rules — the schemes, the claims, the accruals — a home built for them, and let one clean credit-note reconciliation join the two. Book a demo to see how it fits your setup.

Frequently asked questions

Can Tally handle distributor claims and trade schemes?

The honest answer depends on your own setup, so check it directly. A claim or scheme needs four things tracked together: the promise, the base it applies to, the evidence behind it, and the settlement window. Confirm whether your configuration holds all four beside the ledger entry, or whether that logic currently lives in spreadsheets.

How do I record a scheme settlement as a credit note?

A scheme settlement usually posts as a credit note in your accounting system, but the GST treatment depends on the scheme type and documentation. We cover the mechanics separately — see our articles on financial versus tax credit notes and on GST adjustments for channel settlements, and confirm the specifics with your tax advisor.

Do I need separate software if I use Tally?

Not necessarily. Many teams run schemes and claims in spreadsheets beside Tally and cope fine at low volume. The question is whether the rules work — validation across scheme terms, primary sales, secondary sales and evidence — is getting slow or error-prone. If it is, a dedicated claims workflow feeding credit notes back into Tally is worth considering.

How does ClaimDS work with Tally?

At a file-exchange level. ClaimDS manages the scheme rules, claim validation and settlement computation, then exports the results as Excel or CSV, which you import or key into Tally as credit notes. It is a file-based exchange, not a live API connector, so the two systems stay independent and each keeps doing its own job.

Where does the claims workflow begin and the ledger end?

The ledger records what happened — the invoice, the credit note, the posting. The claims workflow governs the rules around it: what was promised, on what base, with what proof, within what window. The ledger stores the outcome; the claims workflow decides what the outcome should be before it is posted.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Scheme and Claim Management Beside Your Accounting System

What belongs in your accounting system and what belongs in a claims system beside it — schemes, claims, accruals and settlements, whatever ERP you run.

How to Move Rebate and Claim Work Off Spreadsheets

A practical guide to migrating rebate, scheme and claim work off spreadsheets — what to extract, how to map schemes, handle history, and cut over.

How Much Does Rebate and Claims Software Cost in India?

What Indian manufacturers actually pay for scheme and claims software — pricing models, what drives cost, the costs quotes leave out, and how to compare.