Managing Rebates, Schemes and Claims When You Run Busy

How Indian distributors and manufacturers on Busy handle rebates, trade schemes and claims — where the ledger ends and the claims workflow begins.

Busy records the transaction. When you raise an invoice, issue a credit note or post to a ledger, that entry is captured cleanly. But a rebate or trade scheme is not a transaction — it is a rule that sits around many transactions: who qualifies, on which sales, at what rate, and settled how. Busy holds the entries; the scheme logic and the distributor claim built on top usually live in spreadsheets beside your accounting software. This article is about where that line falls — and how to draw it cleanly.

What Busy handles well

Busy is a capable accounting and inventory system, and for a large share of Indian distributors and manufacturers it is the reliable spine of the business. It records the things a ledger is meant to record. Sales and purchase invoices are captured with the tax detail intact. Party ledgers carry running balances so you always know what a distributor owes or is owed. Stock and inventory move through the system, tying quantities to value. GST outputs are prepared from the same source data, which keeps returns grounded in the actual transactions rather than a parallel spreadsheet. And when a correction is needed, credit notes can be raised and posted against the right party so the books stay balanced.

None of this is in question, and nothing here argues that anyone should move off Busy. If Busy is your system of record, keep it as your system of record. What matters is knowing what job an accounting package is built to do — capture and report on transactions accurately — and not expecting it to also carry the scheme-and-claim logic that decides what those transactions should be. (Specific capabilities vary by edition and configuration, so check whether your version supports a particular feature before relying on it; the glossary is a useful reference for the terms below.) The point is not about the product. It is about the shape of the work.

Where scheme and claim work ends up outside the ledger

Follow a single trade scheme through a distributor business and you can watch it drift away from the ledger at every step.

It starts with a scheme circular — the announcement that a 2% quarterly rebate applies on a product group, or that a slab kicks in above a volume threshold. That circular has no home in an accounting system. It is a rule, not a transaction, so it lands in email, a WhatsApp forward, or a shared folder, and it is read by hand each time a claim is checked.

Then there is secondary sales. Many trade schemes are earned on what the distributor sells onward, not on what you billed them. Those sell-through numbers sit in the distributor's own books or a DMS, not in your Busy company. Without that feed you cannot confirm a secondary-scheme settlement is genuinely earned.

Claims arrive as evidence, not entries. A distributor sends a claim with a scheme reference, a sales statement, maybe photographs of a display or damaged stock. That is a document to be validated against a rule — it is not yet anything the ledger can post.

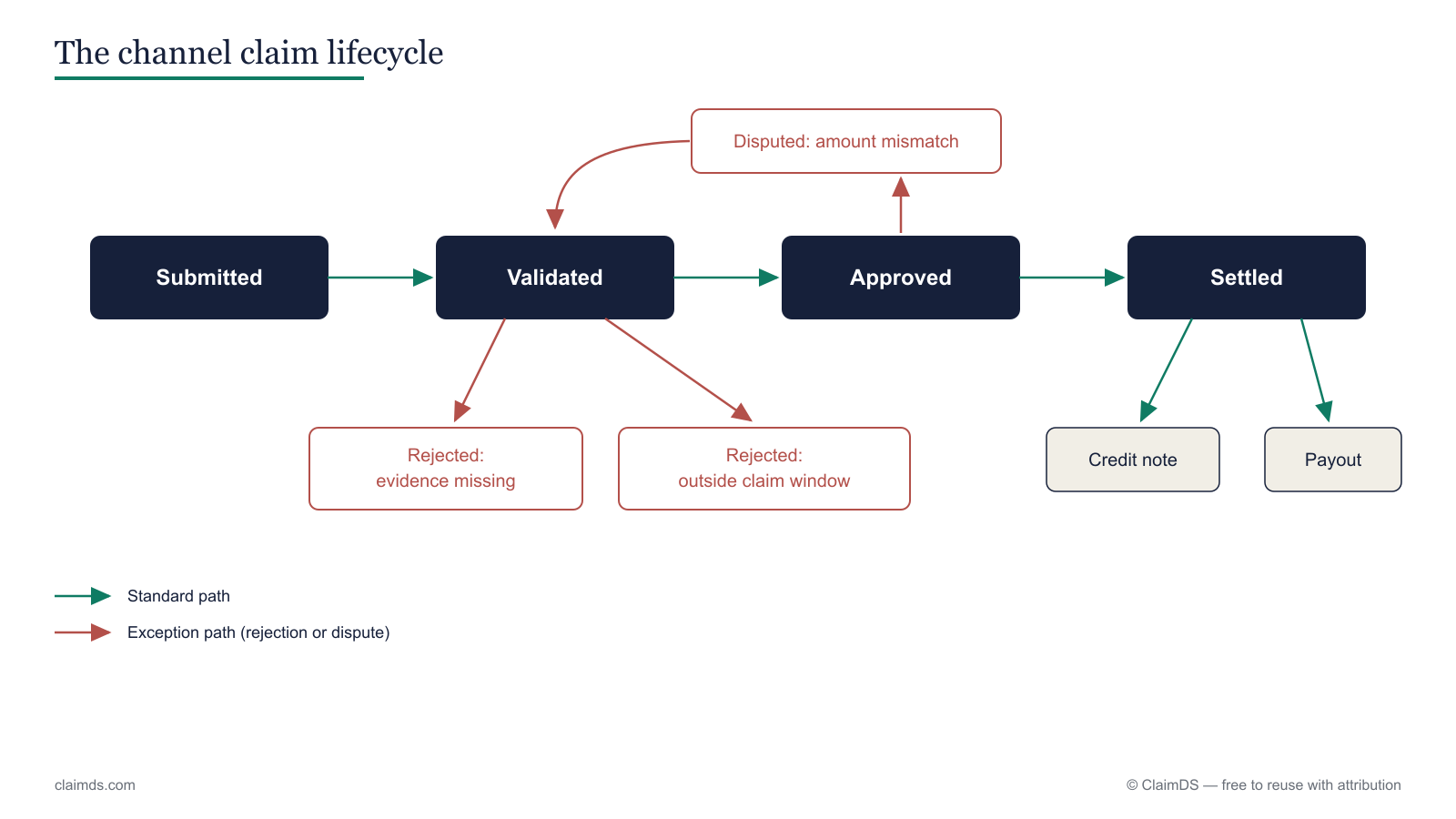

So validation happens across four separate data sources at once: the scheme rule, your primary invoices, the distributor's secondary sales, and the claim document. Reconciling those by hand is exactly where revenue leakage creeps in — a claim paid twice, a rate misread, an expired scheme still honoured.

And the accrual has to be computed, not looked up. You need to know what you owe across live schemes before anyone raises a credit note, so the number is right at month-end. For a worked view of that math see how distributor claims are calculated; for the reconciliation of the resulting notes against returns, see matching scheme credit notes to GSTR-2B/3B. This is the same pattern across channel rebates in India, and it is the reason ERP integration decides claims and rebate software success: the ledger and the scheme logic have to meet somewhere, and the meeting point needs to be deliberate. The Busy rebate-tracking overview walks through where that boundary usually sits.

The credit note is the join

Here is the clean way to think about it. Two systems, one handshake.

The claims system decides what is owed and why. It holds the scheme rules, checks the claim against primary and secondary sales, computes the accrual, and runs the approval so there is an auditable answer: this distributor is owed this amount, under this scheme, for this period.

Busy issues and posts the credit note for that settled amount against the distributor's ledger, so the books and the GST position reflect it. The GST treatment of the settlement — financial versus tax credit note — is decided here, and the GST credit-note reconciliation closes the loop.

The document number is the join. The claim carries the credit-note number; the credit note's narration carries the scheme or claim ID. Anyone auditing later can walk from a ledger entry back to the rule that produced it.

ClaimDS connects to Busy through Excel and CSV file exchange only — export the sales data in, import or key the approved settlements back out — never a native or live API connector. <!-- TODO: confirm capability wording with founder -->

The claims system decides what is owed; the credit note posted in Busy is the join.

A practical setup

You do not have to rebuild anything to get this right — the aim is simply to give each kind of work the place it belongs, and to make the boundary between them an explicit, documented handover rather than an accident of habit. A workable arrangement for a Busy-based distributor looks like this:

-

Keep every scheme and claim in a claims system, not in the accounting ledger. Load the scheme rules once, and let each claim be validated against primary and secondary sales rather than re-read from a circular by hand. A dedicated claims-management tool is built for this; a rebate-management system covers the accrual side.

-

Run claims through an explicit approval workflow so nothing is paid on a verbal yes. The claim and rebate approval workflow — and the approval-workflow reference — give you the states an amount passes through before it becomes a credit note. This is also where deduction-management best practice and the claims-and-deduction reconciliation belong.

-

Post settlements as credit notes in Busy. Once approved, the settled amount becomes a credit note against the distributor's ledger, tagged with the claim ID. Busy stays the system of record for the books; the claims system stays the system of record for the rules.

-

Reconcile once, from a single export. At month-end, take one Excel or CSV export of computed settlements from ClaimDS and reconcile it against the credit notes posted in Busy, so accrued and settled agree. <!-- TODO: confirm capability wording with founder --> The settlement and payout view is where those figures are computed before they cross into the ledger.

Settlements computed in ClaimDS, then posted as credit notes in your accounting system.

The same split applies whichever accounting package you run — see the companion pieces on managing claims alongside your accounting system, and the Tally and Zoho versions of this setup.

Busy is a good place for your transactions to live. Schemes and claims are a different job, and giving that job its own layer — with the credit note as the handshake back into Busy — is what keeps both clean.

Frequently asked questions

Can Busy handle distributor claims and trade schemes?

Busy records the underlying transactions — invoices, credit notes and ledger entries. Scheme and claim management is a different job, one that means reading the circular, validating secondary sales, computing accruals and approving payouts. Most teams run that logic in spreadsheets or a dedicated claims tool beside their accounting software, then post the agreed result back as a credit note.

How do I record a scheme settlement as a credit note?

Once the claim is approved and the amount agreed, you raise a credit note against the distributor's ledger for the settled value, referencing the scheme or claim ID in the narration. Apply the GST treatment your finance team has decided on — a financial versus a tax credit note changes whether output tax adjusts. The claim record and the credit-note number should always tie together.

Do I need separate software if I use Busy?

Not always. Many smaller distributors manage a handful of schemes in spreadsheets alongside Busy and cope fine. The case for a dedicated claims layer grows with volume — more schemes, more partners, more validation across primary and secondary sales, and heavier month-end reconciliation. When spreadsheets start breaking or claims slip through, a claims system beside your accounting software earns its place.

How does ClaimDS work with Busy?

Through file exchange, not a live connector. You export invoice and sales data to ClaimDS as Excel or CSV, ClaimDS computes the accruals, validates claims and produces the settlement figures, and you import or key the approved amounts back into Busy as credit notes. There is no native API integration — the two systems meet through spreadsheet files at defined points.

Where does the accounting ledger stop and the claims workflow start?

The ledger stops at the transaction — the invoice raised, the credit note issued, the balance carried. The claims workflow covers everything that decides those entries — eligibility rules, rate slabs, secondary-sales validation, accrual computation and approval. The credit note is the handover point where the claims decision becomes a posting in your books.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Scheme and Claim Management Beside Your Accounting System

What belongs in your accounting system and what belongs in a claims system beside it — schemes, claims, accruals and settlements, whatever ERP you run.

How to Move Rebate and Claim Work Off Spreadsheets

A practical guide to migrating rebate, scheme and claim work off spreadsheets — what to extract, how to map schemes, handle history, and cut over.

How Much Does Rebate and Claims Software Cost in India?

What Indian manufacturers actually pay for scheme and claims software — pricing models, what drives cost, the costs quotes leave out, and how to compare.