Channel Partner and Sales-Agent Commission in India: A Practical Guide

How to pay commission to external channel partners and sales agents in India — the agreement, the invoice, the payout and the tax split from an employee incentive.

A channel-partner or sales-agent commission is a fee paid to someone outside your payroll for a service — usually bringing you business. Unlike an incentive to your own employee, the partner is a service supplier: the payment flows through an agreement, an invoice, a payout (with TDS on the base), and a tax treatment that differs from salary. Get the relationship right first; everything else follows from it.

The partner commission flow

| Step | What happens |

|---|---|

| 1. Agreement | Scope, rate/slab, qualifying conditions, payment terms |

| 2. Partner delivers | Books the business, or refers the lead |

| 3. Partner invoices | Commission and GST shown separately |

| 4. You pay | TDS deducted on the base commission, not the GST |

| 5. Reconcile | Match the payout to your records |

Source: ClaimDS — free to reuse with a link back to this article.

Who is a channel partner or sales agent?

The defining fact is that the partner is not your employee. Beyond that, the role varies:

- A sales or commission agent who procures orders on your behalf.

- A referral partner who introduces leads or customers.

- A channel partner who sells alongside you into a segment.

- A carrying-and-forwarding (C&F) agent who stocks and forwards your goods — explained in what a C&F agent is.

- A direct-selling agent (DSA) who sources business, common in lending.

Each is paid for a service they render to you — which is what separates them from an employee, and from a distributor who buys and resells on their own account.

How partner commission works end to end

The mechanics are the five steps above, but two of them carry most of the risk. The agreement decides how commission is earned — scope, rate, qualifying conditions — and prevents most disputes; how to structure one is covered in the commission agent agreement. The invoice decides how much you actually pay and deduct, because the base and the GST must be shown correctly; what a clean invoice must contain is set out in the commission invoice format.

Underneath both, the same calculation runs as for any incentive: a target or event, an achievement, a rate, an approval, a payout — and a clawback if the sale reverses. It is the same engine that runs an employee incentive plan or a channel rebate; only the payee, and therefore the tax, changes.

Partner commission vs employee incentive vs channel discount

Three payouts look similar and are taxed differently, and the whole of getting this right is telling them apart:

- Employee incentive — paid to your own staff; part of salary.

- Partner commission — paid to an external party for a service; a fee, invoiced and taxed as a service.

- Channel discount — paid to someone who buys and resells on their own account; a price reduction, not a fee.

The referral and channel-partner programs that many businesses run sit in the middle case, and the C&F and DSA partners sit there too.

What about the tax?

An external partner's commission carries TDS and GST obligations that differ from an employee incentive — and the exact sections, rates and thresholds matter. This article deliberately does not state them; the detail lives in the dedicated tax articles, which are written to be reviewed by a chartered accountant before you rely on them. Confirm the tax treatment of your own arrangement with a professional.

<!-- TODO: link "TDS on commission and incentive: employee vs agent" (the tax pillar, #151), "TDS on the GST component of commission" (#153) and "Discount or commission? The Section 194H line" (#152) once they are out of draft. -->Read next

- How to structure a commission agent agreement — the contract that prevents disputes.

- Commission invoice format — what a partner's invoice must show.

- Referral and channel-partner commission programs and C&F and DSA partner commissions.

- What a C&F agent is, distributor vs dealer vs super-stockist and channel loyalty programs.

- Incentive management software — the engine that runs it.

- How to design a sales-incentive plan — the employee-side sibling to this partner pillar.

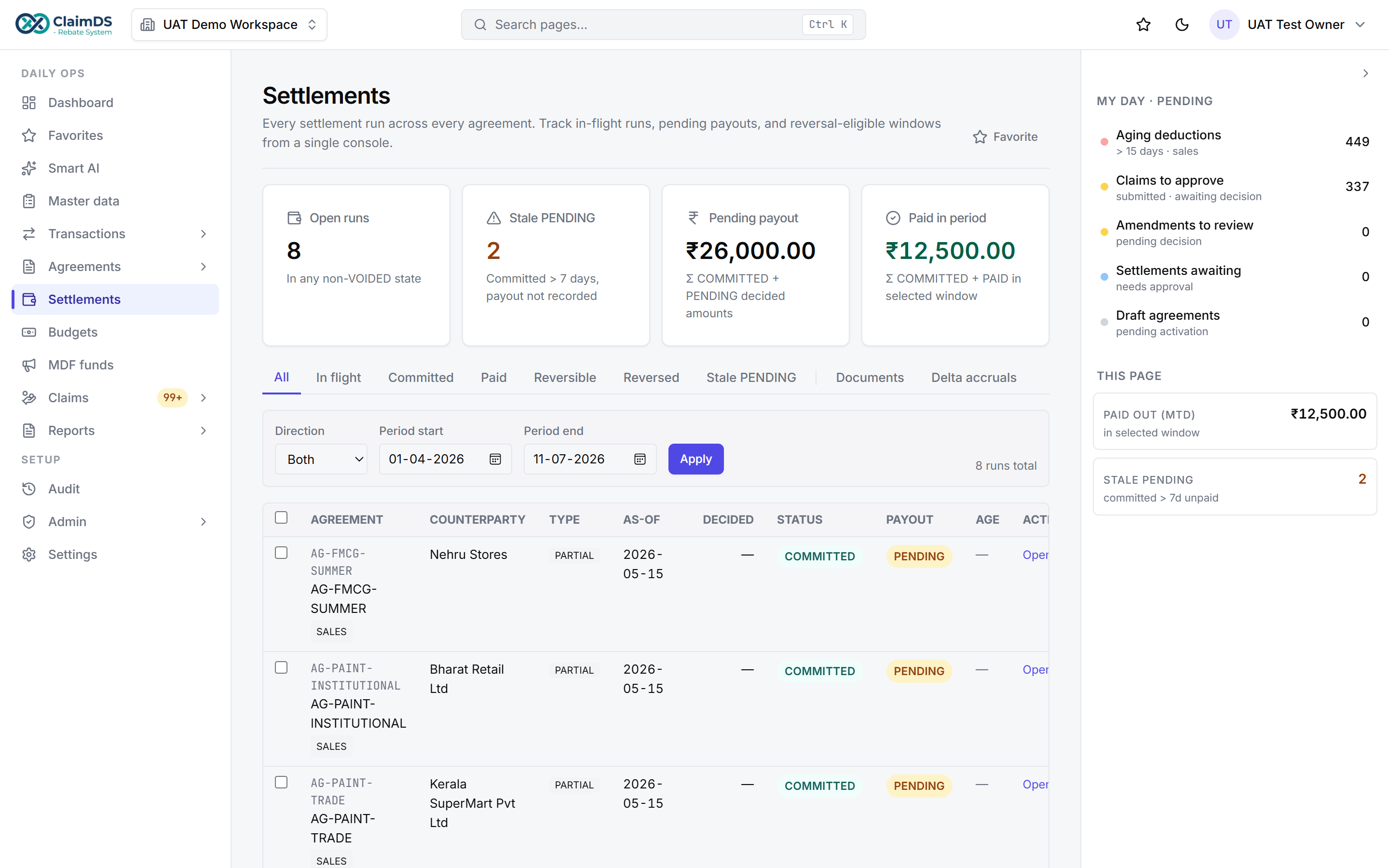

ClaimDS runs partner commission end to end — the agreement terms, the attributed achievement, the payout, the TDS on the base and the partner's GST — in one auditable place, alongside your channel rebates.

<!-- TODO: confirm capability wording with founder -->

The ClaimDS settlement view — payouts calculated, approved and settled in one place.

Book a demo to see how channel-partner and sales-agent commission is calculated and settled.

Frequently asked questions

What is a sales-agent or channel-partner commission?

It is a fee paid to someone outside your payroll — a sales agent, referral partner or channel partner — for a service they render to you, typically bringing you business. It differs from an incentive paid to your own employee: the partner is a service supplier, so the payment flows through an agreement, an invoice, and a different tax treatment.

How do you pay commission to a channel partner?

Agree the scope and rate in a commission agreement, let the partner deliver the business, receive their invoice showing the commission and GST separately, pay after deducting TDS on the base commission, and reconcile it to your records. Because the partner is an external service supplier, the payment is documented and taxed differently from an employee incentive.

What is the difference between paying an employee and paying a sales agent?

An employee incentive is part of salary, paid through payroll under an employment relationship. A sales-agent commission is a fee to an external party for a service, paid against an invoice under a commission agreement. The two carry different documentation and different tax treatment, so the first question with any payout is which relationship it belongs to.

Do channel partners need a commission agreement?

Yes. A written commission agreement sets the scope of work, the rate or slab, the qualifying conditions, the payment terms and how a claim is evidenced, so both sides agree how commission is earned and settled. Without one, commission disputes are common and the tax characterisation of the payment is harder to support.

Is GST charged on channel-partner commission?

Generally, an external partner rendering a service raises an invoice charging GST on the commission, and TDS is deducted on the base commission rather than the GST. The exact rate, threshold and treatment are set out in the dedicated tax articles and should be confirmed with a professional, because the position is specific to the arrangement.

What types of external sales partners are there?

Common types include a sales or commission agent who procures orders, a referral partner who introduces leads, a channel partner who sells alongside you, a carrying-and-forwarding (C&F) agent who stocks and forwards goods, and a direct-selling agent (DSA). Each is outside your payroll and paid for a service, but the exact role shapes the agreement and the payout.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

ASM and Field-Force Incentive Structures for Indian Distribution

How to structure incentives across a field sales hierarchy — sales officer, ASM and RSM — in Indian distribution, so each tier is paid on the right base.

How to Calculate Sales Incentives in Excel (and Where It Breaks)

A step-by-step way to calculate sales incentives in Excel — mapping, slabs, gates and payout — and the point at which a spreadsheet stops being safe to run on.

Paying C&F and DSA Partners: Commission for Carrying-and-Forwarding and Direct-Selling Agents

How carrying-and-forwarding (C&F) agents and direct-selling agents (DSA) are paid commission in India — two external partner types, clearly explained.