How to Structure a Commission Agent Agreement in India

What a commission agent agreement should cover — scope, rate, qualifying conditions, evidence, payment terms and tax responsibilities — for Indian businesses.

A commission agent agreement should cover eight things: the scope of work, the commission rate or slab, the qualifying conditions, how a claim is evidenced, the payment terms, the tax and GST responsibilities, the term and termination, and disputes and clawback. Get those right and most commission arguments never happen. This is general information, not legal advice — have any agreement reviewed for your business.

The clauses that matter

Source: ClaimDS — free to reuse with a link back to this article.

Scope, rate and qualifying conditions

The first three clauses do most of the work. Scope says what the partner is engaged to do — and, just as importantly, what they are not. The rate or slab sets how commission is calculated, including any tiers, accelerators and caps. The qualifying conditions define the single thing most agreements get vague about: when commission is actually earned.

"When a sale happens" is not precise enough. Is commission earned on an order booked, on payment received, or on a referral converted? Does it require the customer to stay for a period? Naming the earning event exactly is what prevents the classic dispute where a partner claims commission the business does not think was earned.

Evidence, payment terms and clawback

The next clauses make the arrangement operable. Evidence of a claim says what proves a sale or referral — the document or system record that triggers commission — so a claim can be validated rather than argued. Payment terms set the cycle, the invoice trigger and the timeline. And a clawback clause lets the business recover commission if the underlying sale is later cancelled, returned or unpaid — the same reversal discipline any payout needs, so the partner is paid for genuine business only.

Tax and GST responsibilities

The agreement should record who is responsible for what on tax — ordinarily the business deducts TDS on the commission and the partner charges GST on their invoice — but the agreement records the responsibility; it does not decide the tax. The exact sections, rates and thresholds are set by law and are covered in the dedicated tax articles, which should be reviewed by a chartered accountant. Confirm the treatment for your arrangement with a professional.

<!-- TODO: link the tax pillar (#151) and "TDS on the GST component of commission" (#153) once they are out of draft. -->Term, termination and post-term commission

Finally, the term and termination clause sets the duration, the notice period, and — a point often missed — what happens to commission on business booked before termination but settled after. Handling post-term commission explicitly avoids a messy exit.

Read next

- Channel partner and sales-agent commission — the pillar this sits under.

- Commission invoice format — what the partner's invoice must show.

- Referral and channel-partner commission programs and C&F and DSA partner commissions.

- Incentive management software — running the payout side.

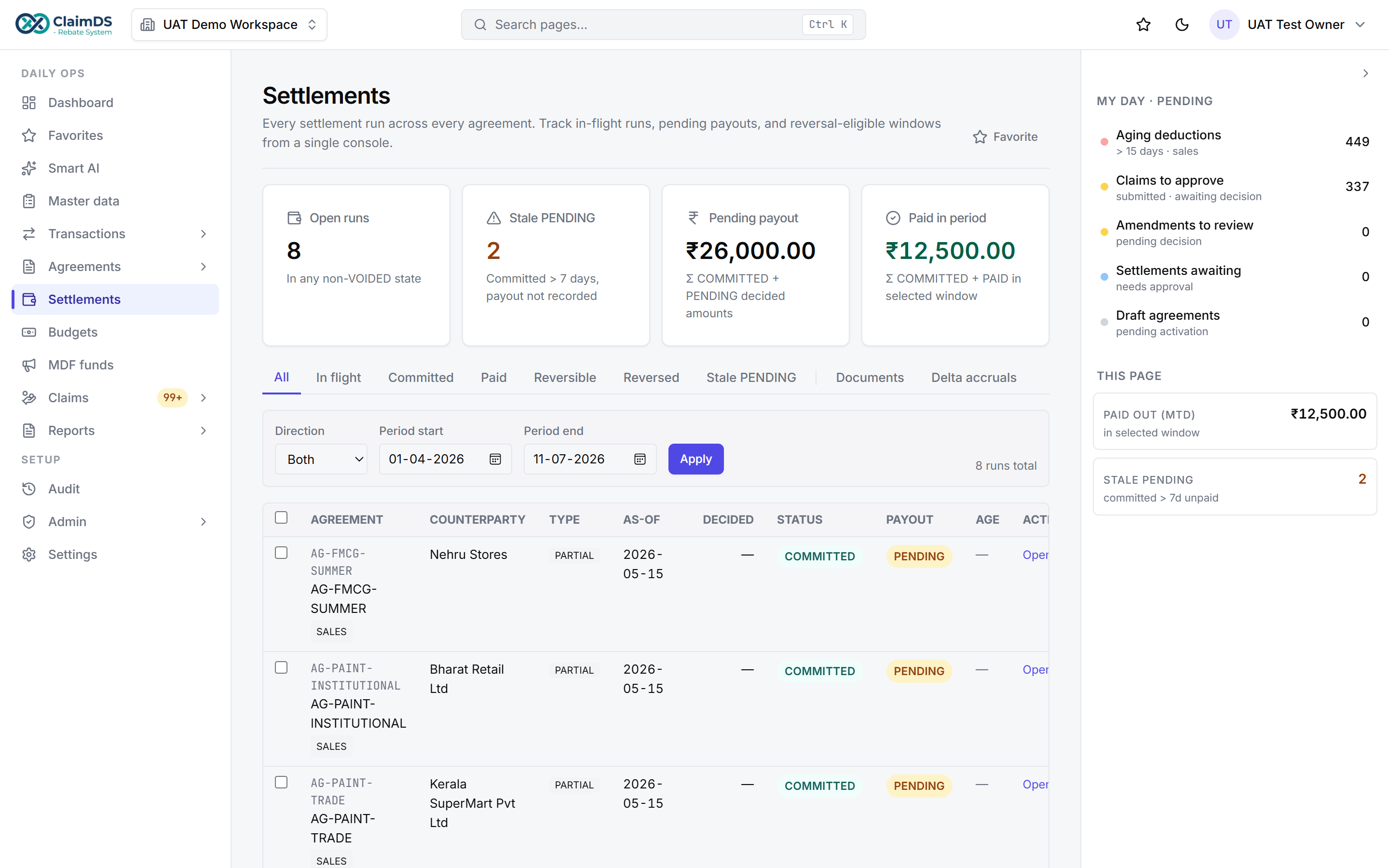

ClaimDS turns the agreement's terms — rate, qualifying conditions, evidence, clawback — into a running calculation, so what the contract says and what the partner is paid stay the same.

<!-- TODO: confirm capability wording with founder -->

The ClaimDS settlement view — payouts calculated, approved and settled in one place.

Book a demo to see a commission agreement run as a live, auditable calculation.

Frequently asked questions

What should a commission agent agreement include?

A commission agent agreement should set out the scope of work, the commission rate or slab, the conditions under which commission is earned, how a claim is evidenced, the payment terms, the tax and GST responsibilities, the term and termination, and how disputes and clawbacks are handled. Together these define exactly how commission is earned and settled.

How is commission earned defined in an agreement?

Commission is earned when the qualifying conditions in the agreement are met — typically an order booked, a payment received, or a referral converted, depending on the model. Defining the earning event precisely, rather than leaving it to 'when a sale happens', is what prevents most commission disputes between a business and its partner.

Who is responsible for TDS and GST in a commission agreement?

Ordinarily the paying business deducts TDS on the commission, and the partner charges GST on their invoice for the service. The agreement should state who bears what, but the exact rate, threshold and treatment are set by tax law and should be confirmed with a professional — the agreement records the responsibility, it does not decide the tax.

Should a commission agreement include a clawback clause?

Yes, where commission is paid before a sale is final. A clawback clause lets the business recover commission if the underlying sale is later cancelled, returned or unpaid, so the partner is paid for genuine business only. Without it, a reversed sale stays paid, which turns the commission arrangement into a leak.

Is a written commission agreement legally required?

A written agreement is strongly advisable even where an oral arrangement might be recognised, because it evidences the terms, supports the tax characterisation of the payment, and settles how commission is earned and disputed. This is general information and not legal advice, so have any agreement reviewed by a professional for your business.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

ASM and Field-Force Incentive Structures for Indian Distribution

How to structure incentives across a field sales hierarchy — sales officer, ASM and RSM — in Indian distribution, so each tier is paid on the right base.

How to Calculate Sales Incentives in Excel (and Where It Breaks)

A step-by-step way to calculate sales incentives in Excel — mapping, slabs, gates and payout — and the point at which a spreadsheet stops being safe to run on.

Paying C&F and DSA Partners: Commission for Carrying-and-Forwarding and Direct-Selling Agents

How carrying-and-forwarding (C&F) agents and direct-selling agents (DSA) are paid commission in India — two external partner types, clearly explained.