Trade schemes & settlement

Scheme settlement software for Indian trade schemes

Settle QPS, volume and secondary schemes the way Indian channels actually run them — from the scheme circular, through the distributor claim and validation, to a GST-compliant credit note, in one workflow.

14-day free trial · no credit card

What is scheme settlement software?

Scheme settlement software settles the trade schemes you run for your channel — QPS, volume and secondary schemes — from end to end. It takes a scheme from its circular, through the distributor’s claim and validation against the agreement, to a GST-compliant credit-note settlement, all in one workflow. It is built for Indian distributors and manufacturers who today settle scheme claims by circular and spreadsheet, and want the scheme, the claim and the credit note tied together and provable.

The problem

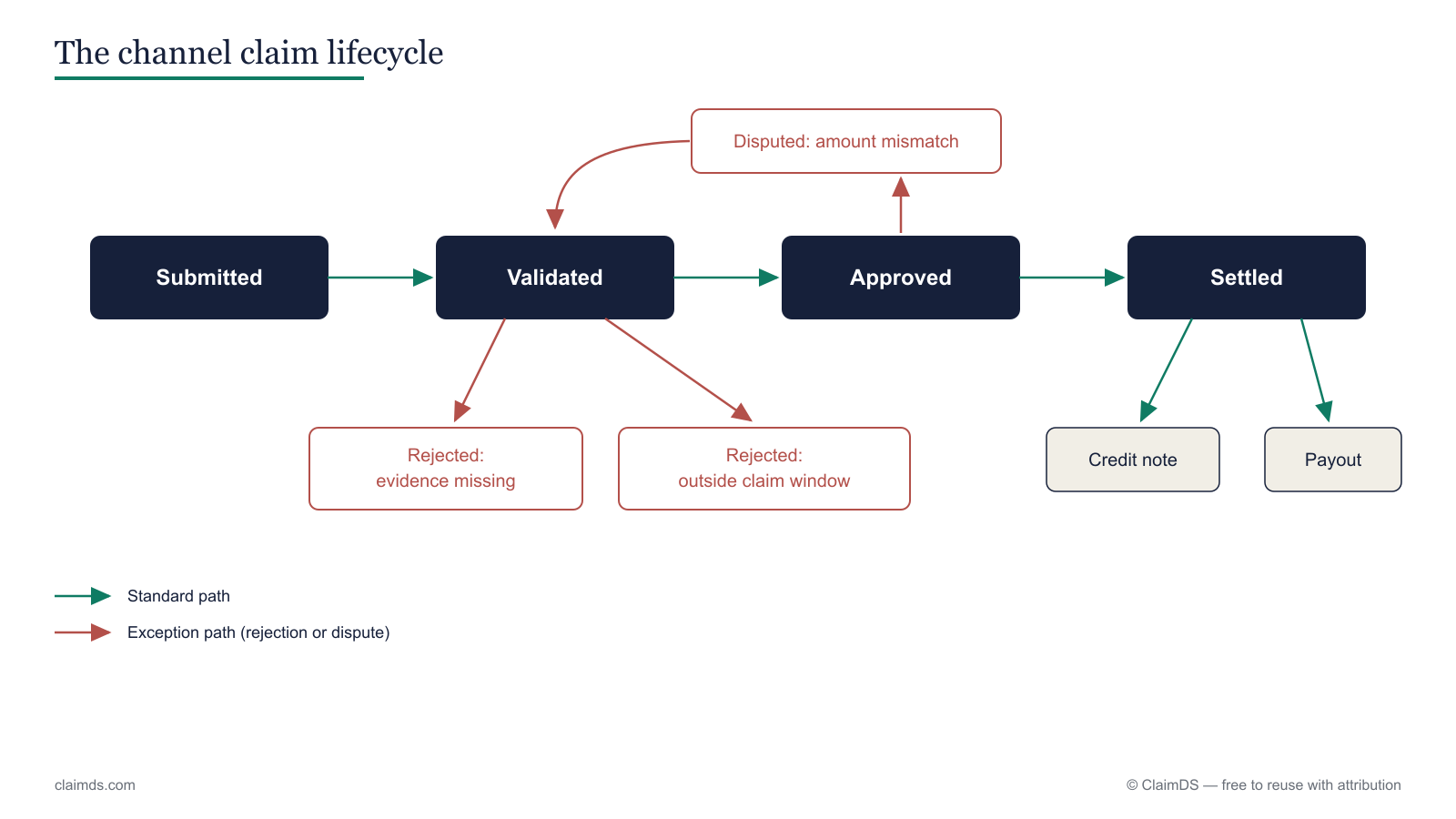

A trade scheme starts life as a circular — a QPS slab, a volume target, a secondary-scheme offer down to the retailer — and ends as money the channel expects back. In between, the settlement work is manual. A distributor raises a scheme claim, and someone in finance has to pull the circular, re-key the claim into a spreadsheet, and check it line by line against the scheme terms and the agreement to see what the party is actually entitled to.

Then the credit note has to be raised correctly for GST, the accrual reconciled, and the whole thing filed so it survives an audit or a distributor dispute months later. When every scheme lives in its own sheet, the live picture — what is claimed, what is validated, what is settled — is never in one place. Claims sit in dispute, credit notes get raised wrong, and a secondary-scheme claim can rarely be traced back to the circular it came from.

How ClaimDS settles schemes

- 1. One queue for every scheme claim. QPS, volume and secondary-scheme claims land in a single workflow instead of scattered inboxes and sheets — so the live position across every scheme is always in one place.

- 2. Auto-match the claim to the scheme. Upload the distributor’s claim file and ClaimDS auto-matches it against the relevant scheme agreements, so you review the variances instead of re-keying and tying out every line by hand.

- 3. Accruals that compute automatically. Each scheme accrues as transactions land, so the liability behind a claim is already known when the claim arrives — see rebate scheme accrual tracking for the accrual step.

- 4. Validate against the agreement. Every claim is checked against the scheme circular, the agreement and the underlying data, so you settle on entitlement, not on the number the distributor sent.

- 5. Settle by GST credit note. Approved claims settle through the correct GST credit note under Rule 53(1A), with the tax treatment and input-tax-credit position handled rather than reconstructed later.

- 6. Hash-chained audit log. Every state change — who raised, validated, approved or settled a claim — is written to a tamper-evident, hash-chained audit log, so a settled figure is always defensible.

- 7. Tenant-isolated data. PostgreSQL row-level security applies on every row, so no other company — and not even ClaimDS’s own engineers — can read across company boundaries.

- 8. Hand off to payout. Once a scheme claim is settled, the payable moves to settlement payout management for the payout step, with the claim, the accrual and the credit note all tracing back to one agreement.

Built for the Indian channel

Scheme settlement in India is not the same problem a Western rebate tool solves. Goods move through a multi-tier route-to-market — C&F, super stockist, distributor, wholesaler, dealer and retailer — and a scheme can be settled at any of those tiers. ClaimDS models that hierarchy, so a claim settles against the right party at the right level.

It settles by GST credit note under Rule 53(1A) rather than a plain payment, because in India a post-sale scheme benefit is passed back through a credit note. It handles secondary schemes — the offers that run below the primary sale, down to the retailer — in the same workflow as primary QPS and volume schemes. And it keeps fidelity to the scheme circular: the terms you published are the terms a claim is validated against, so what was announced and what gets settled never drift apart.

Related reading

- Secondary scheme settlement — how below-the-primary schemes are claimed and settled down to the retailer.

- Types of trade schemes in India — QPS, volume, slab and target schemes explained.

- FMCG trade schemes explained — how consumer-goods brands structure and run channel schemes.

- Reconciling scheme credit notes with GSTR-2B and 3B — tying settled credit notes back to your GST returns.

- Claim and rebate approval workflows — the validation and approval path a scheme claim moves through.

- Financial vs tax credit notes under GST — which credit note a scheme settlement should use, and when.

- Channel rebates in India — how scheme settlement fits the wider channel-rebate picture.

Frequently asked questions

What is scheme settlement software?

It is software that settles the trade schemes you run for your channel — QPS, volume and secondary schemes — end to end. It takes a scheme from its circular, through the distributor claim and validation against the agreement, to a GST-compliant credit-note settlement, in one workflow instead of scattered spreadsheets.

Who is it for?

Indian manufacturers and distributors running trade schemes across a multi-tier channel — C&F, super stockist, distributor, wholesaler, dealer and retailer. If your team settles scheme claims by circular and spreadsheet today, this replaces that with one auditable queue.

How is this different from settlement payout management?

This page covers settling the scheme and the claim end to end — scheme circular, claim intake, validation and the credit note. Paying the settled amount out is the downstream step, handled by our settlement payout management solution. Scheme accrual — building the live liability before a claim — is handled by rebate scheme accrual tracking.

Does it handle secondary schemes?

Yes. Secondary schemes — run below the primary sale, down to the retailer — are settled in the same workflow as primary QPS and volume schemes, so a secondary-scheme claim ties back to its circular and agreement just like any other claim.

How does GST-compliant settlement work?

Approved scheme claims settle through the correct GST credit note under Rule 53(1A), so the tax treatment and input-tax-credit position are right rather than reconstructed later. The accrual, the claim and the credit note all trace back to one agreement and a tamper-evident audit log.

How much does it cost?

Pricing depends on your channel size and scheme volume. The honest answer is to see it on your own schemes first — start a trial or sandbox and import your agreements. See the current plans on our pricing page and we will scope it with you.

Settle your trade schemes end to end

Book a ClaimDS demo, or start a trial and import your scheme circulars and agreements. See pricing on our /pricing page.