How Rebate Software Improves Financial Reporting Accuracy

How manual rebates corrupt financial reporting — under/over-accrued liabilities, period-close surprises, misstated margins — and how rebate software fixes each.

Rebate software improves financial reporting accuracy by replacing estimated, quarter-end rebate numbers with a live accrual computed from actual sales, applying the correct credit-note classification, and reconciling to settlement on one auditable record. The result: liabilities, margins and provisions that reflect reality instead of a spreadsheet guess.

GST note: This article is general information, not tax, accounting or legal advice, and touches GST and financial-statement matters that carry real consequences. GST positions — including CBIC Circular No. 251/08/2025-GST and the Finance Act 2026 amendments to Section 34 of the CGST Act (assented 30 March 2026, not yet notified into force as of publication) — and any accounting treatment must be re-verified at publish time with a qualified professional (CA/CMA). Professional review pending.

Why this is a reporting problem, not an admin one

Rebates are one of the largest variable costs in a channel business, accrued over time and settled later. If that accrual is wrong, the financial statements are wrong — the liability, the margin, and the provision. This is the accuracy argument that complements the mechanics in rebate accounting: that page is how to account; this one is how good the numbers are.

How manual rebates corrupt reporting

| Symptom | What causes it |

|---|---|

| Under/over-accrued liability | Estimated, not computed from real volume |

| Period-close surprises | The true number lands late, after books look done |

| Misstated margins | Scheme cost unallocated to the products it funded |

| Audit findings | Accrual and settlement never reconcile |

| GST mismatch | Wrong credit-note classification on settlement |

Each is a reporting-quality failure with the same root cause: the number was guessed, not calculated.

How software fixes each

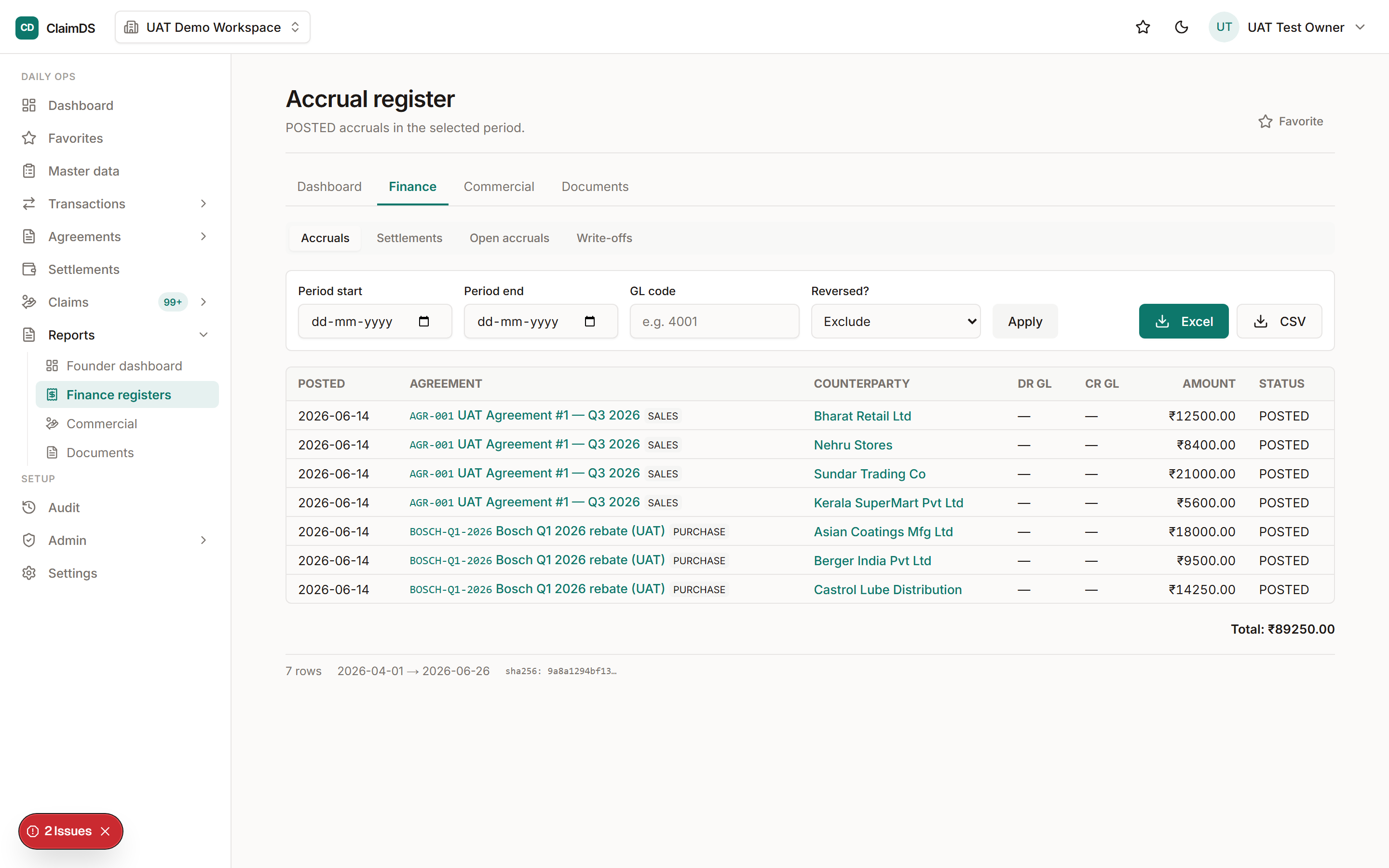

- Real-time accruals from actual sales replace the quarter-end estimate, so the liability is right all period — the rebate tracking view.

- Single source of truth ends the "sales sheet vs finance sheet" divergence, so margins are stated on one reconciled number.

- Correct credit-note classification by rule keeps the GST and financial treatment aligned — see financial vs. tax credit notes.

- Audit trail + reconciliation close the accrual-to-settlement gap before period-end, removing audit findings.

The leadership framing — what to measure and demand — is in the CFO revenue-leakage playbook, and the specific loss quantified in revenue leakage in rebate programs. The reporting layer that surfaces it is rebate analytics.

Where ClaimDS fits

ClaimDS keeps rebate accrual live, classifies the credit note by rule, and reconciles settlement to accrual with a full audit trail — India-first, at a mid-market price (a ClaimDS-supplied ~₹3–5 lakh/yr figure, positioning not a benchmark). It sits under the rebate management software pillar; the deeper positioning is in why ClaimDS.

Frequently asked questions

How does rebate software improve financial reporting accuracy?

It replaces estimated, quarter-end rebate numbers with a live accrual computed from actual sales, applies the correct credit-note classification, keeps a single source of truth reconciled to settlement, and holds an audit trail — so reported liabilities, margins and provisions reflect reality rather than a spreadsheet guess.

How do manual rebates distort financial reporting?

Manual rebates under- or over-accrue the liability, produce period-close surprises when the real number lands, misstate product margins because scheme cost is unallocated, and create audit findings when accrual and settlement don't reconcile — all symptoms of estimating rather than computing the number.

Does rebate accrual affect GST reporting?

It can. The credit-note type used to settle a rebate determines whether output tax changes and whether the recipient reverses ITC. Misclassifying it distorts both the financial statements and the GST return, which is why classification should be by rule and documented.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Rebate Analytics: Reporting, Dashboards & Opportunity Analysis

What rebate analytics should deliver — real-time accrual dashboards, liability forecasting, scheme profitability, partner performance and slab-proximity opportunity analysis.

Revenue Leakage in Rebate Programs: Where the Money Goes & How to Stop It

Where rebate and trade-spend programs leak revenue in Indian multi-tier channels — overpayments, duplicates, unclaimed accruals, mis-slabbed math — and how to stop it.

Claims & Deductions Management for CFOs: A Revenue-Leakage Playbook

A CFO's playbook for channel claims and deductions — quantifying revenue leakage, accrual visibility, GST exposure, the control framework and the KPIs to track.