Chargeback Fraud: Detection & Prevention in Channel Claims

Chargeback fraud and leakage in channel claims — duplicate, inflated and unsupported deductions — and the controls that detect and prevent them. Trade, not card.

In channel claims, chargeback fraud and leakage occur when deductions or claims are duplicated, inflated, or raised without support — sometimes deliberately, often through error. The defence is the same either way: validation against the agreement and data, anomaly and duplicate detection, mandatory evidence, segregation of duties, and an audit trail.

Trade/channel claim fraud, not card fraud. This covers leakage in deductions and claims between a manufacturer and channel partners — not card or payment chargeback fraud handled by banks and networks.

How leakage and fraud occur

| Pattern | What it looks like |

|---|---|

| Duplicate claims | Same deduction raised more than once |

| Inflated claims | Quantity or rate above what is supported |

| Unsupported deductions | No agreement or evidence behind the claim |

| Out-of-window | Claims raised after the eligible period |

Whether deliberate or accidental, each drains money the same way. The hub view is chargeback management software and the claim engine is chargeback claim software.

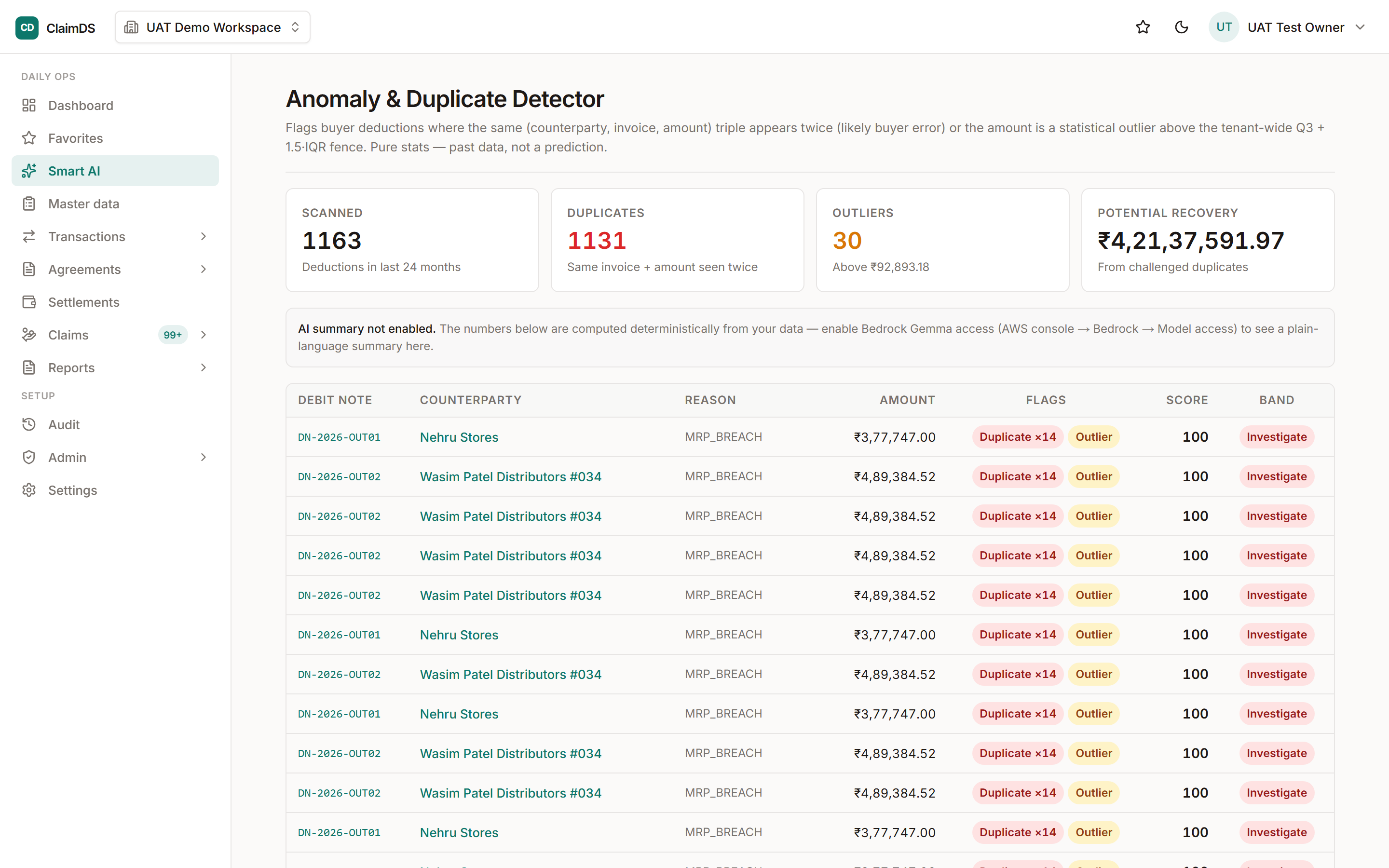

Detection signals

Detection is pattern-spotting at scale. Repeated round-number claims, the same invoice claimed twice, quantities exceeding supply, and clusters of out-of-window deductions are all flags a system can surface automatically. Manual review cannot keep up with the volume — especially in FMCG — which is why anomaly detection and duplicate matching matter.

Preventive controls

- Agreement-based validation — every claim checked against its terms.

- Duplicate detection — block the same deduction twice.

- Mandatory evidence — no support, no settlement.

- Segregation of duties — who raises ≠ who approves.

- Immutable audit trail — every action recorded.

These are the same controls a finance leader should demand in the CFO revenue-leakage playbook.

Fraud vs honest error

Most channel leakage is honest error, not fraud — but the controls that stop one stop the other. Treating the problem as a control problem rather than an accusation keeps channel relationships intact while protecting the money. The dispute side is in the chargeback dispute process.

GST note: This article is general information, not tax or legal advice. Where settlement involves GST credit notes, positions — including CBIC Circular No. 251/08/2025-GST and the Finance Act 2026 amendments to Section 34 of the CGST Act, assented 30 March 2026 but not yet notified into force as of publication — must be re-verified at publish time with a qualified professional.

Frequently asked questions

What is chargeback fraud in channel claims?

In channel claims, chargeback fraud and leakage occur when deductions or claims are duplicated, inflated, or raised without support — intentionally or through error. It is distinct from card chargeback fraud and is controlled through validation, anomaly detection, audit trails and segregation of duties.

How do you detect channel chargeback fraud?

By validating each claim against the agreement and source data, detecting duplicates and statistical anomalies, requiring evidence, and maintaining an audit trail. Patterns such as repeated round-number claims or out-of-window deductions are flags.

How do you prevent chargeback leakage?

With preventive controls — agreement-based validation rules, duplicate detection, mandatory evidence, segregation of duties between who raises and who approves, and an immutable audit trail — so invalid claims are stopped before settlement.

See ClaimDS on your own claims data

A 30-minute walkthrough tailored to how your channel actually settles claims.

Related posts

Why ClaimDS Is the Best Rebate Management Software in India

Why Indian distributors and dealers need finance-grade rebate and claims settlement: multi-tier fidelity, GST credit-note compliance, faster payouts.

Customer Rebates: Programs & Software

Customer rebate programs explained — structures, claim validation, accrual and the GST treatment of customer rebates. Distinct from supplier and distributor rebates.

SMB Rebate Software for India

Indian SMB rebate software — affordable, fast-deploy rebate management for mid-market manufacturers and distributors. Why enterprise suites are overkill for SMBs.